Adam Gault

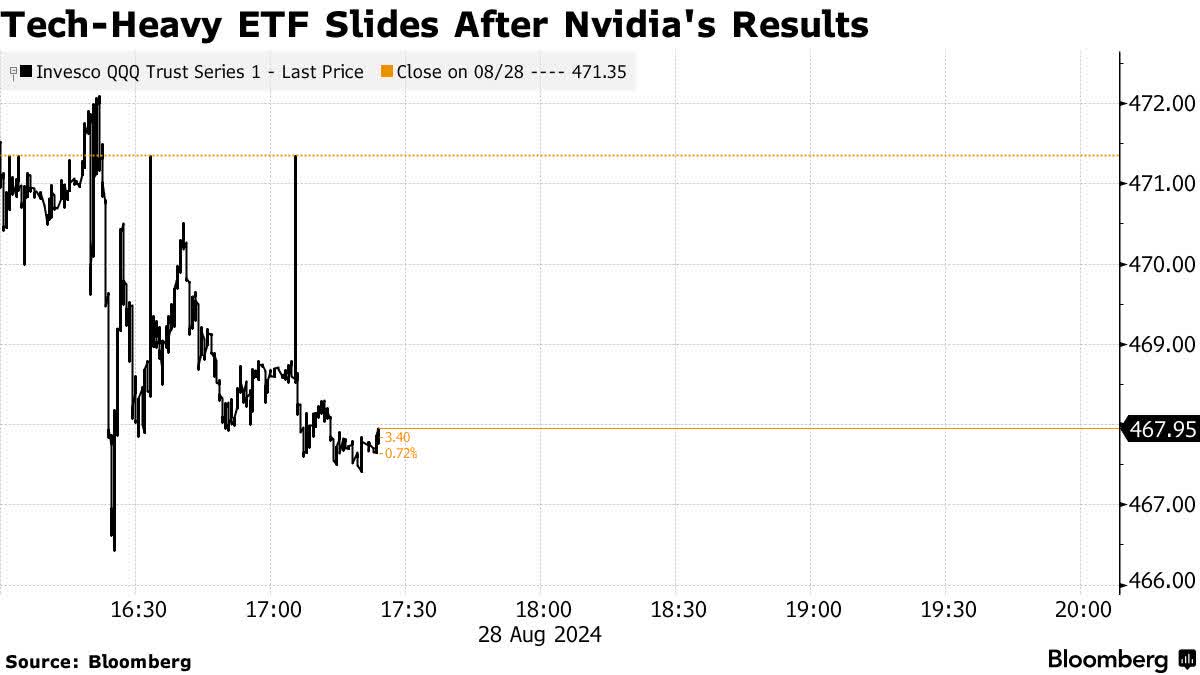

Investors were cautious in advance of earnings results from the largest company in the world, given its significant influence over the major market averages, as well as its status as the bell-weather for the artificial intelligence industry. That caution was warranted. Despite beating both top and bottom line expectations, as well as raising guidance, the beats for Nvidia were not as impressive as they had been since the launch of ChatGPT, and the increase in guidance not as significant. Furthermore, profit margins fell modestly for the first time in two years. Granted, they are still above 50%, which is extraordinary, but it is rates of change that rule the day when it comes to performance.

Finviz

Unsurprisingly, the bear camp was quick to call this the canary in the coal mine for the bull market, unrelenting in their search for reasons why this bull market is unjustified and will end soon. Yet Nvidia does not accurately portray what is happening in the economy or broad market today. It reflects what has helped fuel the bull market over the past two years. The company’s phenomenal growth was unsustainable and bound to slow, which is what we are starting to see today. Now the share price must pause, if not pull back, until the valuation falls in line with more modest rates of growth. This will weigh on the cap-weighted indexes, but investors should not allow it to distract them from the ongoing bull market.

Bloomberg

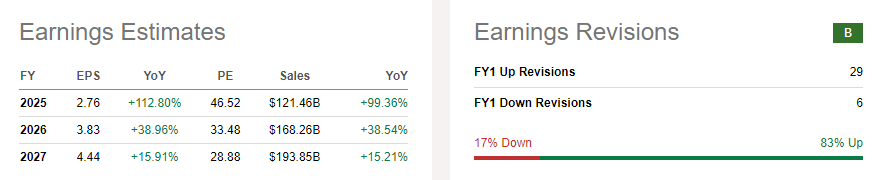

As can be seen plainly in the consensus earnings estimates below, the growth rate for Nvidia is expected to decline from approximately 100% to what will be closer to your typical growth stock of 15% in 2027. That is still phenomenal, but it doesn’t warrant an earnings multiple of nearly 50 times, and stock prices look forward. If the growth rate was 15% today and scheduled to explode to 100% two years from now, that would be a positive rate of change and warrant today’s multiple or higher.

Seeking Alpha

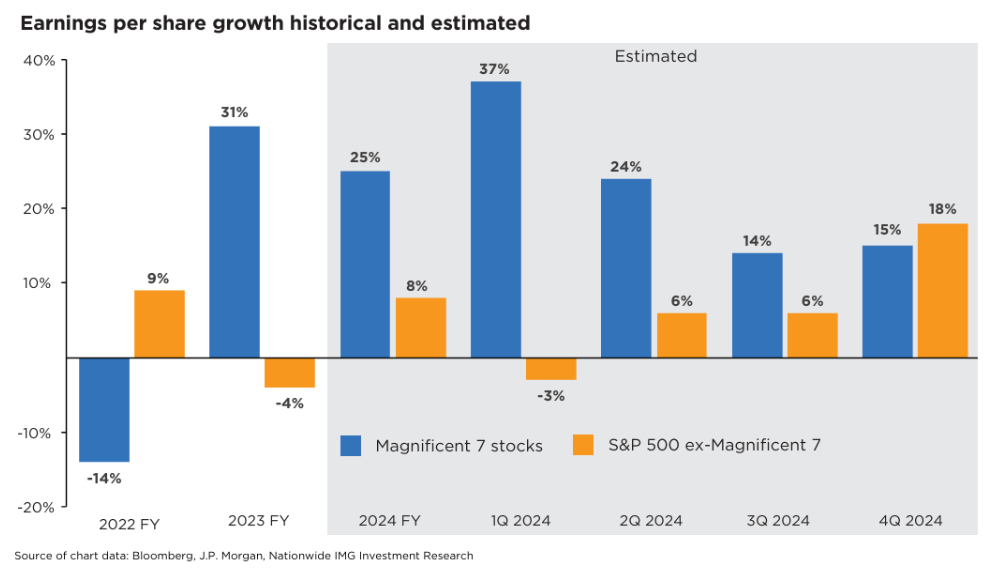

Nvidia is not alone, as the other six members of the club that has been coined the Magnificent 7 are expected to realize a similar deceleration in their collective growth rate as this year progresses. I shared the chart below with investors a few months ago to warn of this deceleration and likely end to outperformance for the technology sector. More importantly, as the rate of growth in earnings for the tech sector was expected to slow, the rate of growth for the remaining 493 companies was expected to increase.

Bloomberg

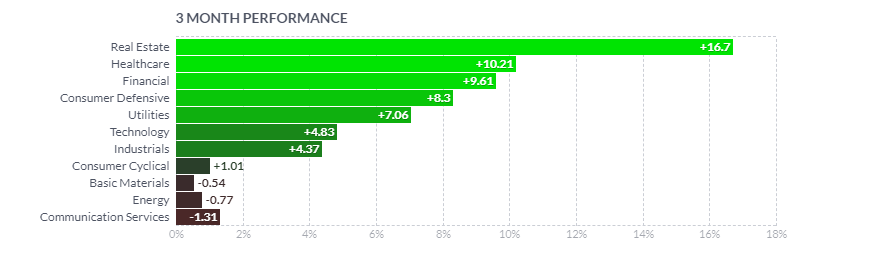

This is why we have seen a rotation from technology to other sectors of the market over the past three months, as market breadth has improved. The improvement in earnings growth for the S&P 500 ex-Magnificent 7 is a function of sustained economic growth.

Finviz

Last week, we received another very encouraging report on the economy from S&P Global. Its Flash US Composite PMI, which is a mid-month survey of corporate executives that measures business activity, reflected robust GDP growth of more than 2% for the current quarter combined with continued disinflation. A recession is not on the horizon. The only caveat is that our economy’s growth is increasingly dependent on the much larger service sector, as manufacturing activity continues to stall. This is why the upcoming monetary policy easing is so critical to the soft landing scenario, as it should help to revive the manufacturing sector. Despite this lopsided growth, the overall economy remains in good shape, which is why we have seen a broadening in sector performance beyond technology. Smaller companies that are more domestically focused are starting to bloom again.

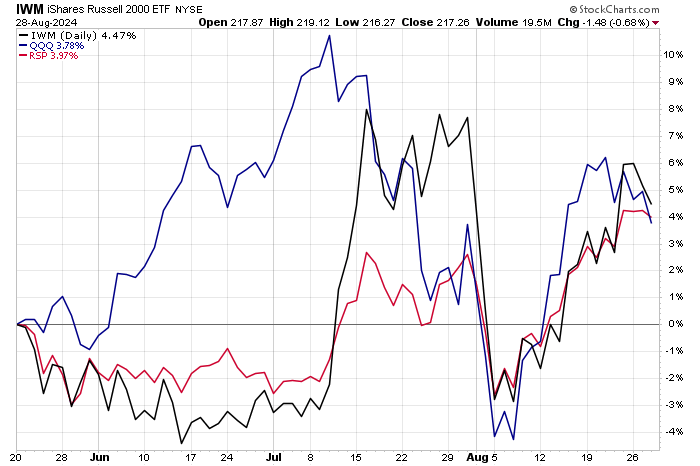

On May 21, I asserted that the tech sector’s outperformance was likely to wane as the economy experiences a mid-cycle slowdown. I think we are in the middle of that slowdown now. I also indicated that Nvidia had a valuation requiring perfection, and that as its rate of growth slowed, along with the other Magnificent 7 names, the Russell 2000 small-cap index was likely to outperform this market leading sector. In advance of Nvidia’s results last night, small cap stocks were finally inching ahead of both the Nasdaq 100 (QQQ) and the equal weight S&P 500 (RSP). I think this outperformance is likely to continue.

StockCharts

{kind=link}