Digital Vision./DigitalVision via Getty Images

On Sept. 5, the 2024/2025 NFL Season will start with a match between the Baltimore Ravens and the defending champions, the Kansas City Chiefs.

If the 2023/2024 season was any indication, this is going to be a great game!

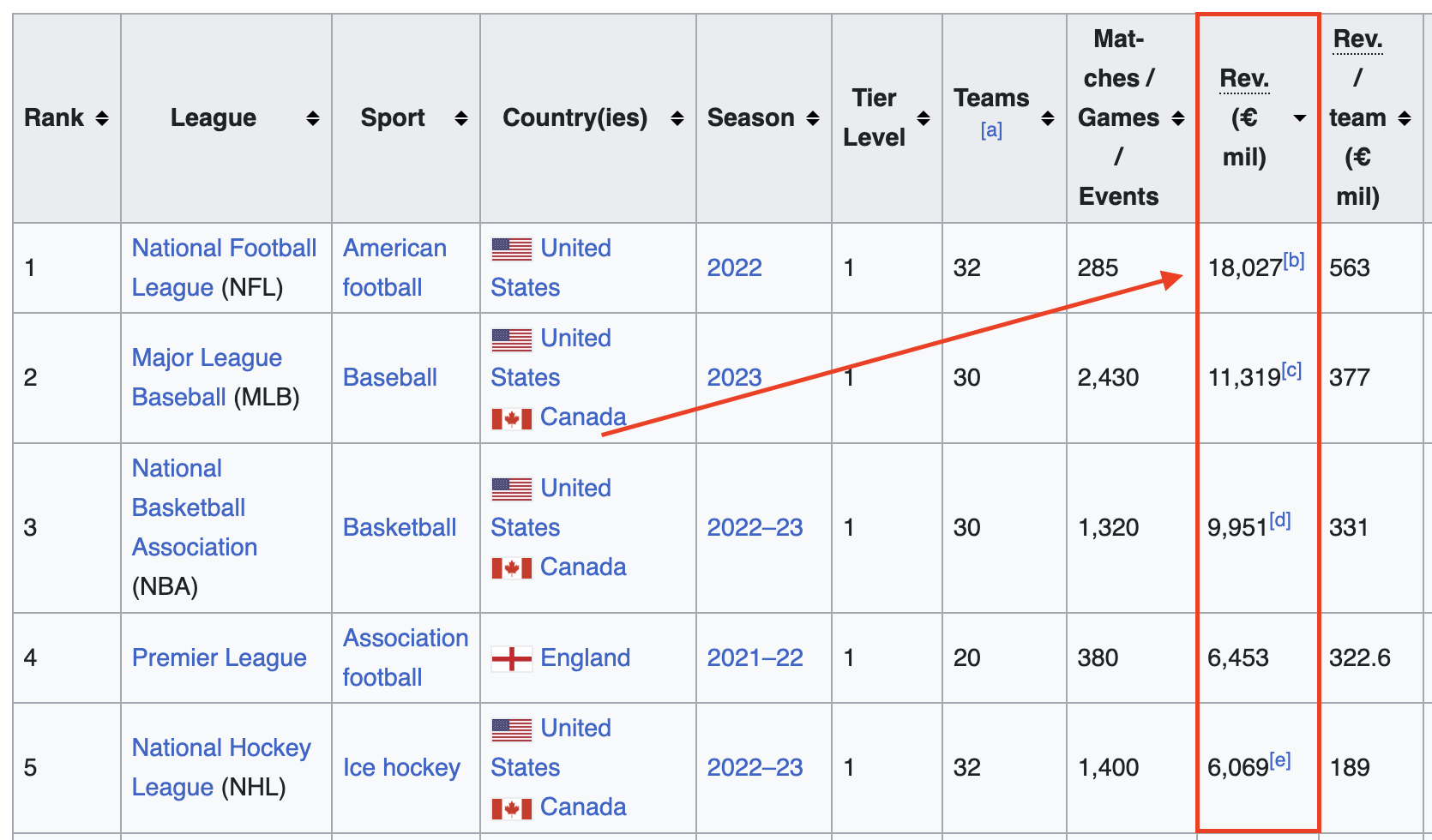

That said, did you know that in 2022, the National Football League generated $18 billion in revenue? That’s according to a list compiled by Wikipedia. This number makes it the biggest league in the world – by a huge margin.

Number two on the list is Major League Baseball, with $11.3 billion in 2023 revenues. The mighty English Premier League is number four on the list, with $6.5 billion in 2021/2022 revenues.

In fact, four out of five leagues are American!

Wikipedia

As one can imagine, if there’s money to be made, Wall Street is interested.

That’s currently the case, as The Wall Street Journal just wrote a big piece titled “Private Equity Ownership Is Coming to the NFL.”

While private equity has been busy buying professional sports teams for a while, the “holy grail” of sports has been out of reach – until now.

The NFL, which always wanted owners to be people instead of corporations, is making some changes. NFL owners are reportedly considering a policy change that will allow for the sale of up to 10% of a team to a select group of pre-approved firms.

In this case, only a few select companies can bid, as we’re dealing with high-ticket teams. Even the Washington Commanders sold for $6 billion “recently.” Imagine what good teams are worth (I’m joking).

With that said, according to Bloomberg, major PE firms like Ares, Blackstone, and Carlyle declined to comment when asked if they were involved. That makes sense, as nothing is yet known.

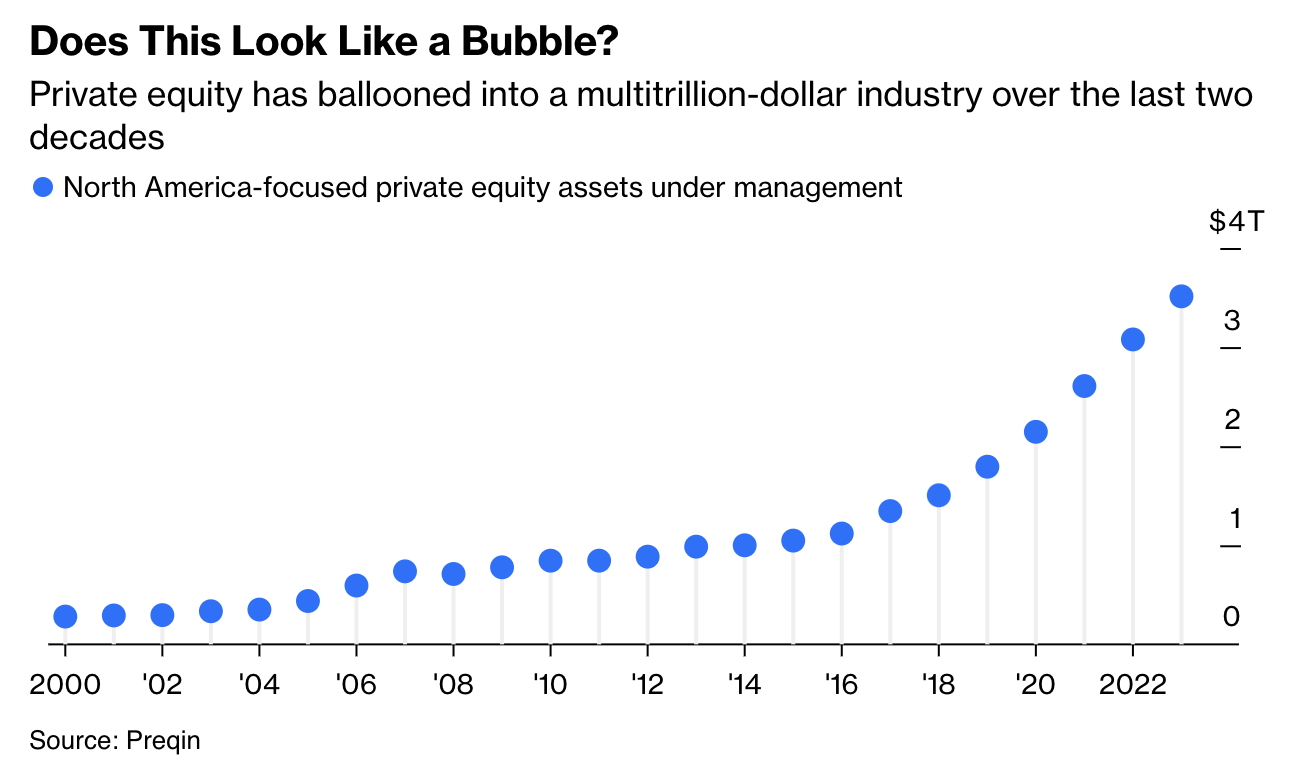

I’m bringing this up because private equity firms are becoming increasingly powerful. Over the past 20 years, the industry has turned into a multi-trillion-dollar industry, growing from $280 million in 2000 to $3.5 trillion in 2023.

Bloomberg

In this article, we’ll discuss two promising players with a lot of influence, starting with the biggest player in the industry.

Blackstone (BX) – The PE King

With a market cap of more than $170 billion, Blackstone is the largest PE firm on the face of the earth.

This did not happen overnight, as the company has spent decades perfecting its approach to asset management. For example, it’s now investing sums that were unheard of before the pandemic.

In the second quarter of this year, the firm deployed $34 billion in capital, the highest number in two years. It deployed close to $90 billion in the past three quarters. Three quarters ago, the 10-year yield peaked, which was highly favorable for PE firms.

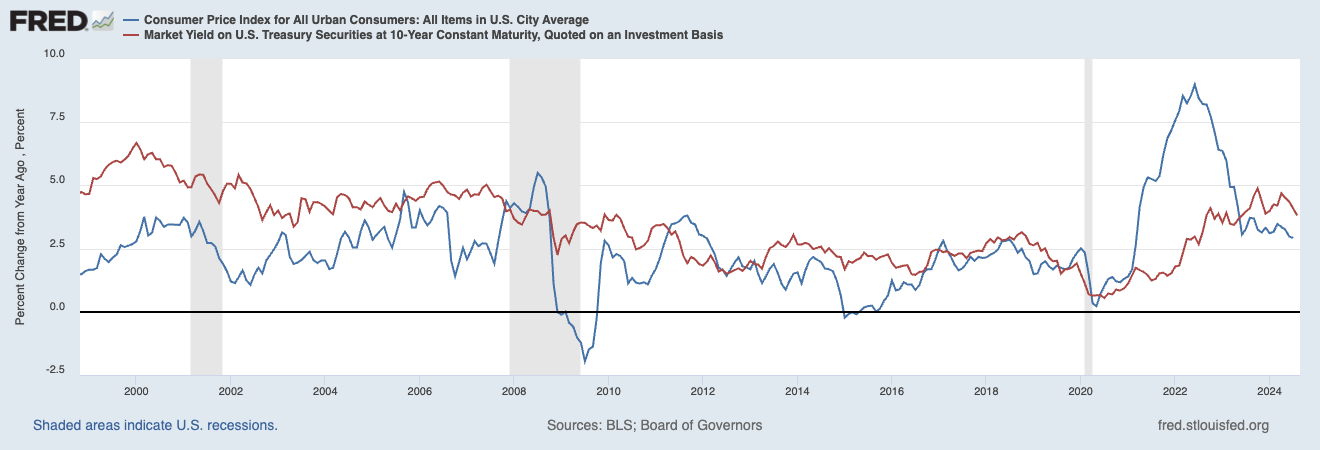

According to the company’s CEO, Steve Schwarzman, this aggressive investment approach was driven by the company’s correct assessment that inflation would come down. As some readers may remember, we have done a few articles in the past on Blackstone’s view on inflation and real estate.

Federal Reserve Bank of St. Louis (U.S. All-Items CPI, U.S. 10Y Yield)

Going forward, the company expects the Fed to cut rates, which was just confirmed by Jerome Powell when he held his Jackson Hole speech a few days ago.

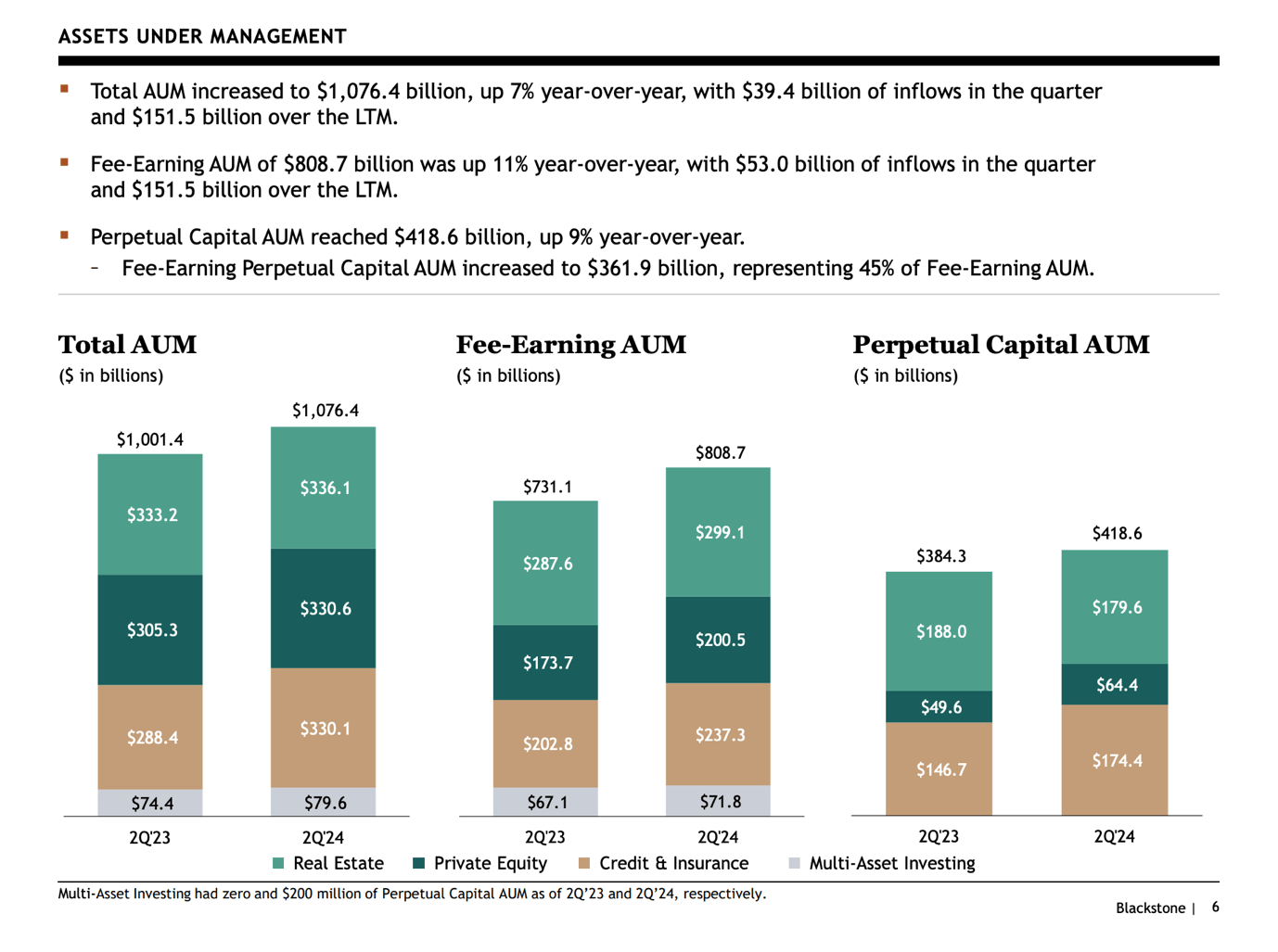

It also helps that Blackstone has a massive scale advantage. Managing $1.1 trillion in assets, the company has an unmatched size benefit, as its many investments provide unique insights that are shared and used to make informed investment decisions. Smaller players cannot compete with that.

Blackstone

This scale advantage started in the early 1990s when the company moved into private equity real estate. More recently, it has expanded its reach by venturing into private credit, global logistics, energy transition assets, and data assets.

In other words, instead of building the Tower of Babylon, the company has built an advanced portfolio of assets enjoying secular tailwinds.

In fact, the company has become the biggest financial investor in AI infrastructure in the world. Its portfolio includes $55 billion in data centers, with an additional $70 billion in developments(!). One of its portfolio companies, QTS, has seen a 7x growth in lease capacity since it was taken private in 2021.

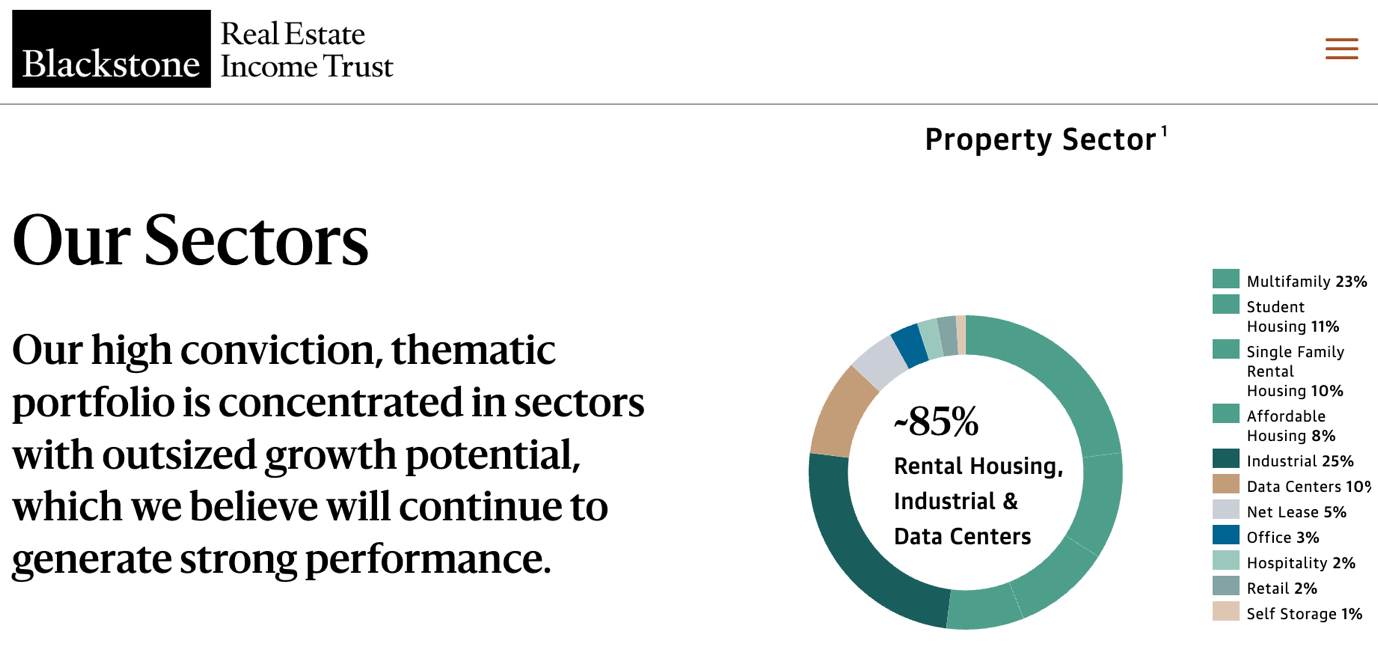

Essentially, one can make the case the company is a well-diversified real estate ETF with a focus on emerging trends. The Blackstone Real Estate Income Trust (“BREIT”) has returned more than 10% per year since its inception more than 7.5 years ago.

Blackstone

Roughly 90% of the BREIT portfolio is invested in warehouses, rental housing, and data centers. This private REIT has grown so fast that it’s 3x larger than the next five largest private REITs combined. Moreover, roughly 70% of its assets are located in attractive Sunbelt markets.

Currently, BX yields 2.4%. The company aims to maintain an 85% distributable earnings payout ratio, which explains why the company does not have consistent dividend growth.

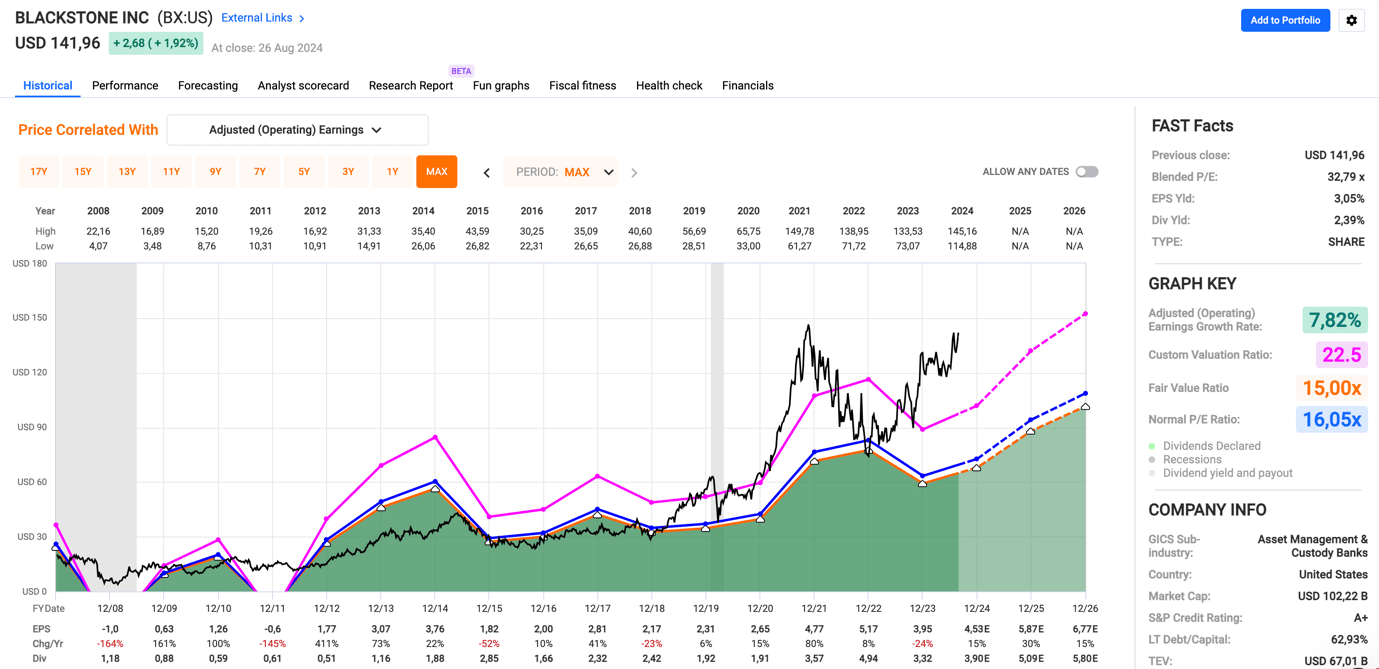

Going forward, analysts agree with the company, as they expect 15% EPS growth in 2024 to be followed by 30% and 15% growth in 2025 and 2026, respectively. Applying its five-year average P/E ratio of 22.5x, which fits its growth outlook, we get a fair stock price of $152, 7% above the current price.

FAST Graphs

Although we prefer a bigger margin of safety, we’re bullish on Blackstone and consider it to be a great investment during dips.

KKR & Co. (KKR) – Eye-watering PE Growth

With a market cap of slightly less than $110 billion, KKR is smaller than Blackstone, but no less impressive.

KKR was founded in 1976 by Henry Kravis, George Roberts, and their mentor Jerome Kohlberg with $120,000. This investment has turned into one of the most diversified PE giants on the planet.

Currently, it has 25 offices and nine global Atlantic offices, managing assets in three large categories: Private equity, real assets, and credit/liquid strategies. In 2010, the company had 13 offices.

KKR

These assets boosted the company’s assets under management to more than $550 million in 2023. Since 2010, that number has grown by 18% per year, on average.

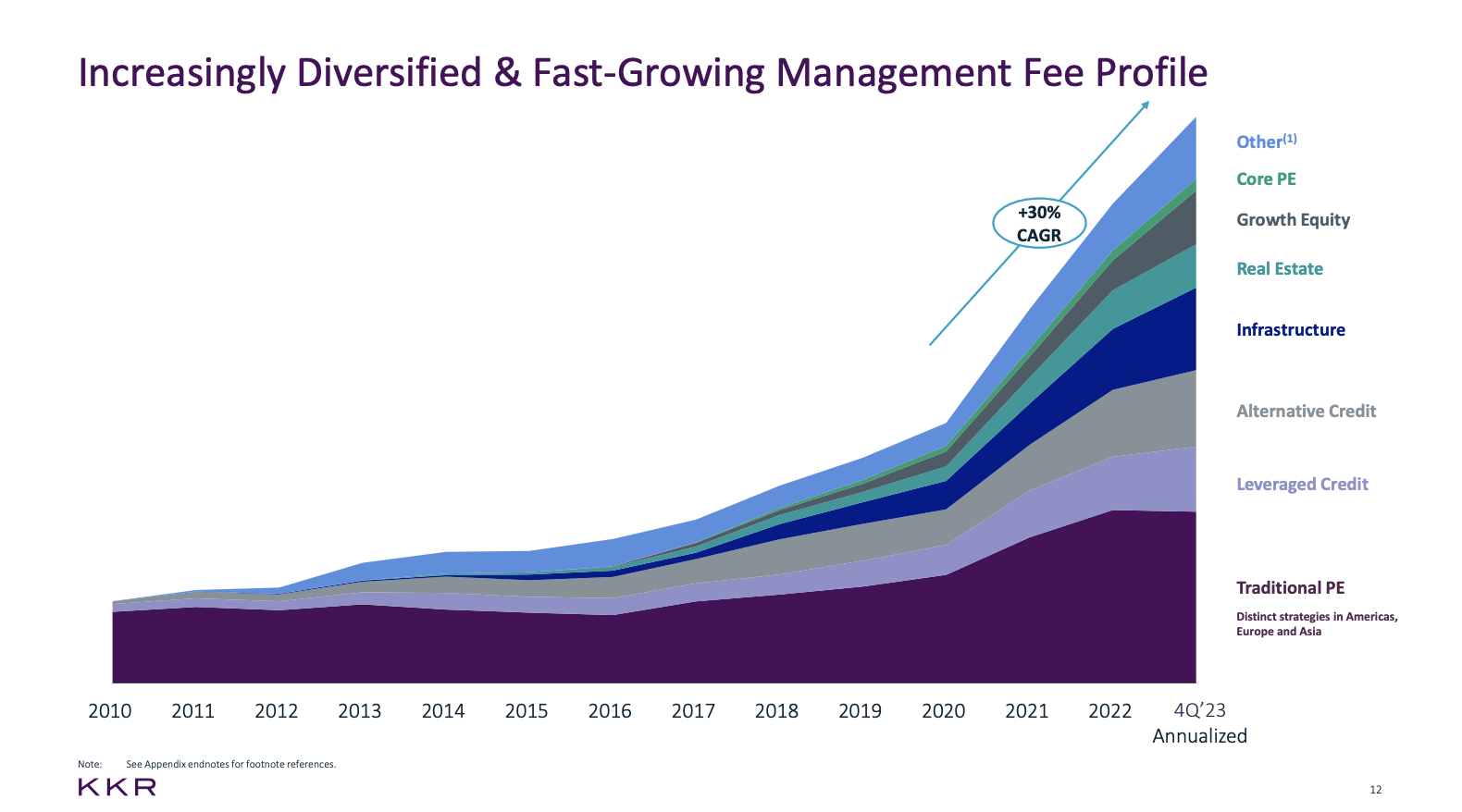

This rapid growth has paved the road for 30% annual growth in management fees. As we can see below, in 2010, the company mainly saw traditional PE fees. Nowadays, it generates more fees from credit, infrastructure, and real estate.

KKR

Last year, the company made $2.4 billion from fee-related earnings, 7x more than it generated in 2010.

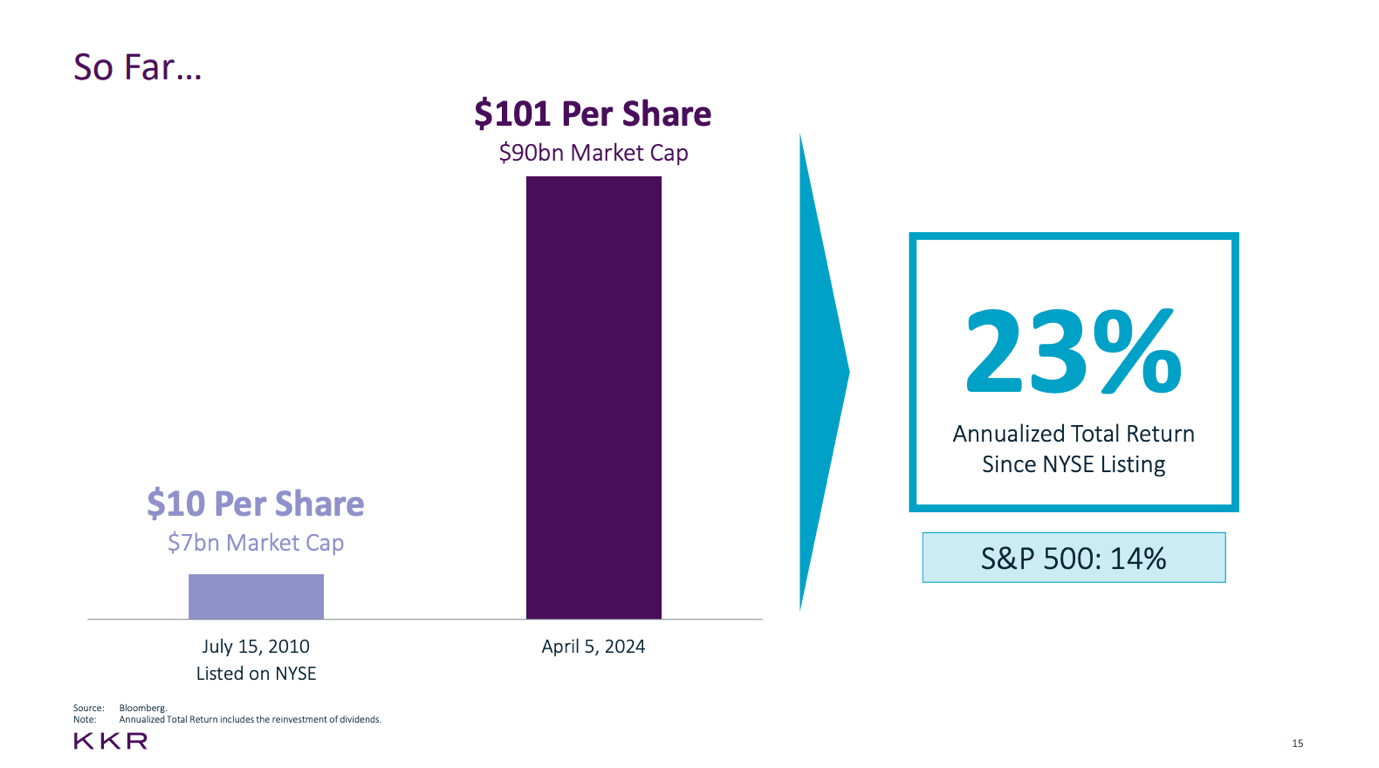

This has been great for shareholders, as the company has returned 23% per year between July 15, 2010, and April 5, 2024. That’s almost 10 points above the S&P 500’s average annual return. These are truly tech-like returns.

KKR

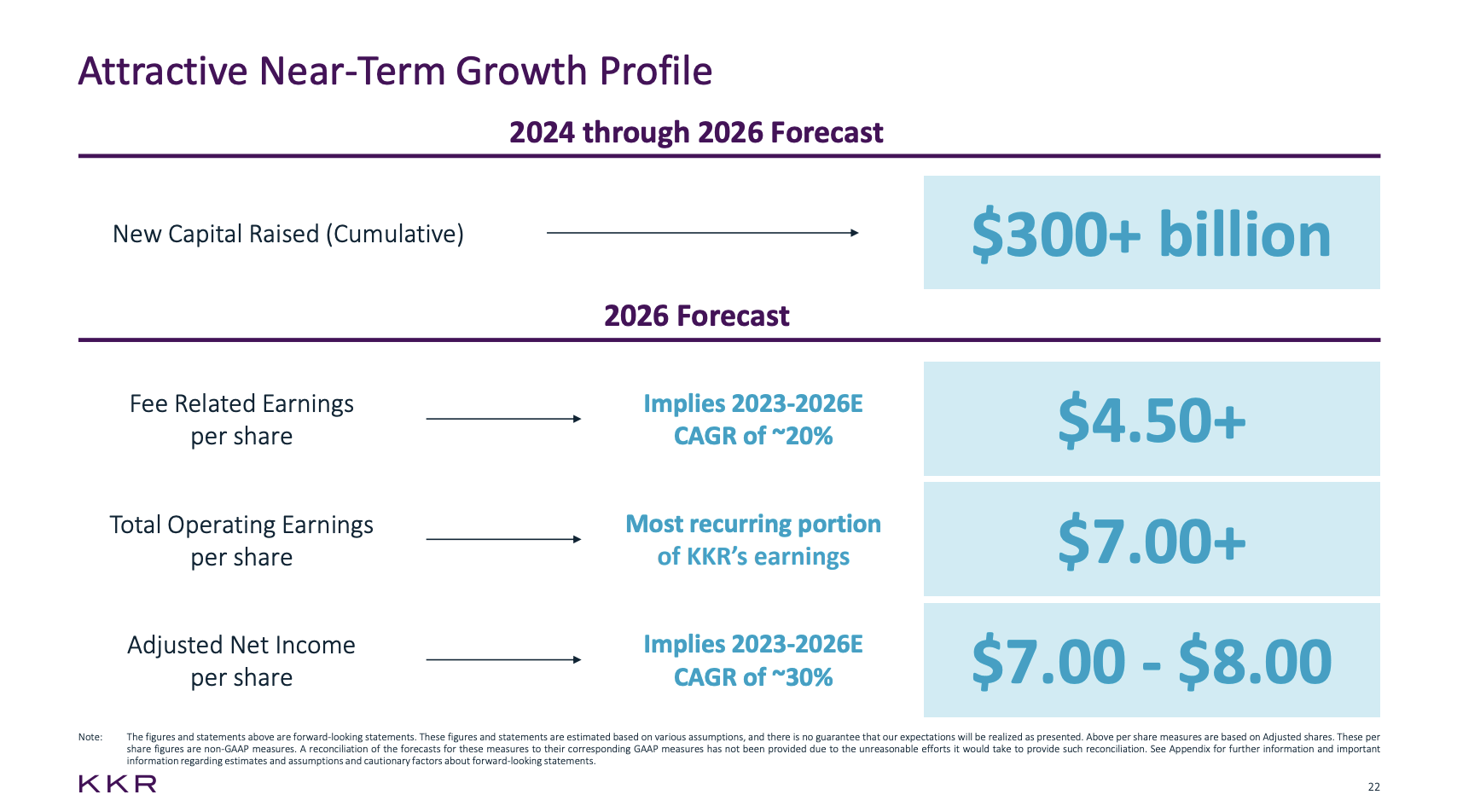

If you think this is impressive, the company used its 2024 Investor Day to make the case that it’s “just getting started.“

Through 2026, the company expects to raise more than 300 billion in new capital, potentially growing net income by 30% per year!

KKR

The company is confident because of three reasons:

- It operates in a high-growth industry with a leadership position in key markets (similar to Blackstone).

- It has a “purpose-built business model” with three growth engines to drive recurring earnings.

- It has a supportive business culture and exceptional capital allocation capabilities.

In its most recent quarter (2Q24), the company put $23 billion to work, bringing the first-half number to $37 billion. This is almost double the amount it deployed in the first half of 2023. In fact, the company’s fundraising is so impressive that it raised $32 billion in 2Q24 alone, the second-best quarter in its history.

It also benefited from strong growth in private equity, infrastructure, real estate, and credit. Meanwhile, its insurance segment after the acquisition of Global Atlantic saw record inflows of more than $8 billion.

Moreover, the company’s market position is supported by strategic initiatives like its partnership with Capital Group. The aim is to increase its reach and offer hybrid investment solutions to a wider investor base.

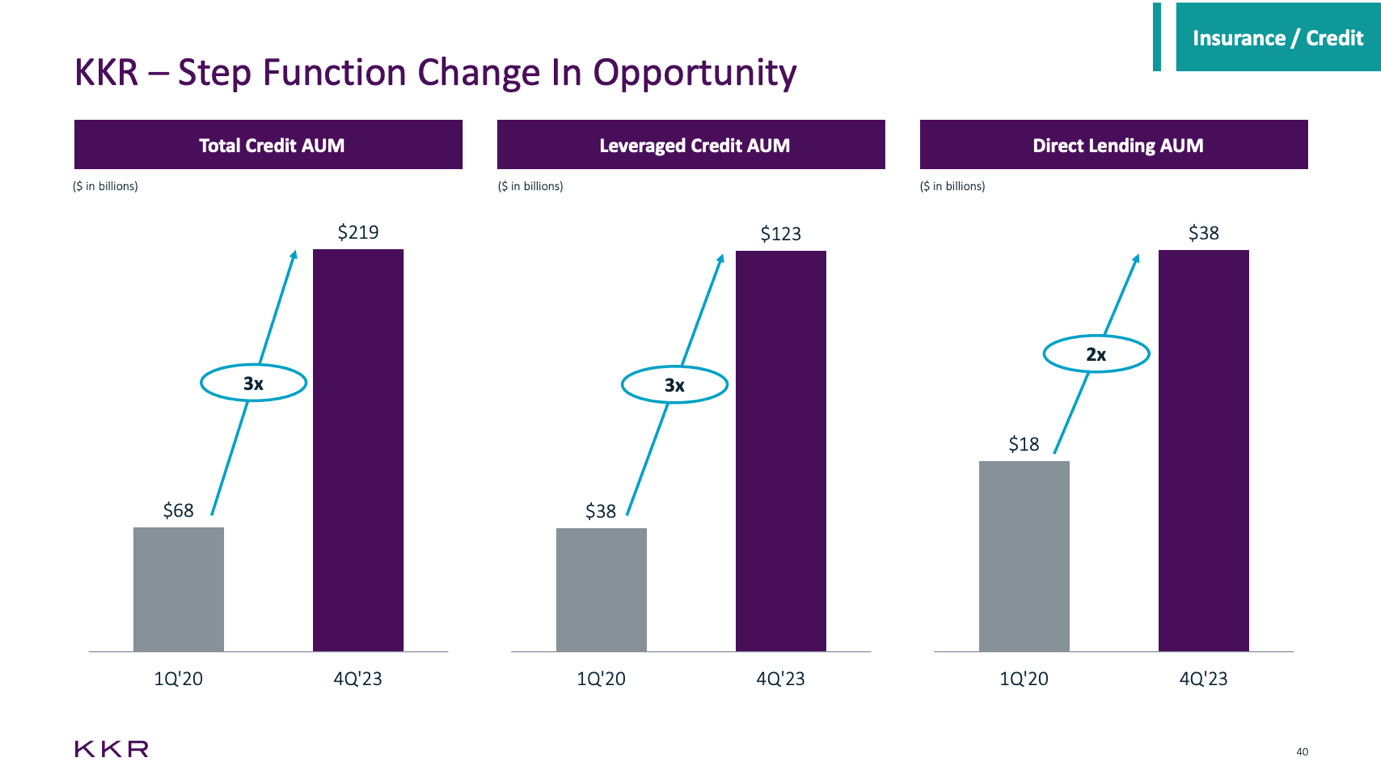

According to KKR, this partnership, its $230 billion credit platform, and its major real estate footprint put it in a great spot to benefit from current market conditions. The global credit market has a $40 trillion size, which offers tremendous opportunities.

KKR

With regard to its dividend, KKR currently pays $0.175 per share per quarter. This translates to a yield of 0.6%.

While it’s hard to get excited about a 0.6% yield, analysts agree with the company’s rosy outlook, expecting aggressive earnings growth.

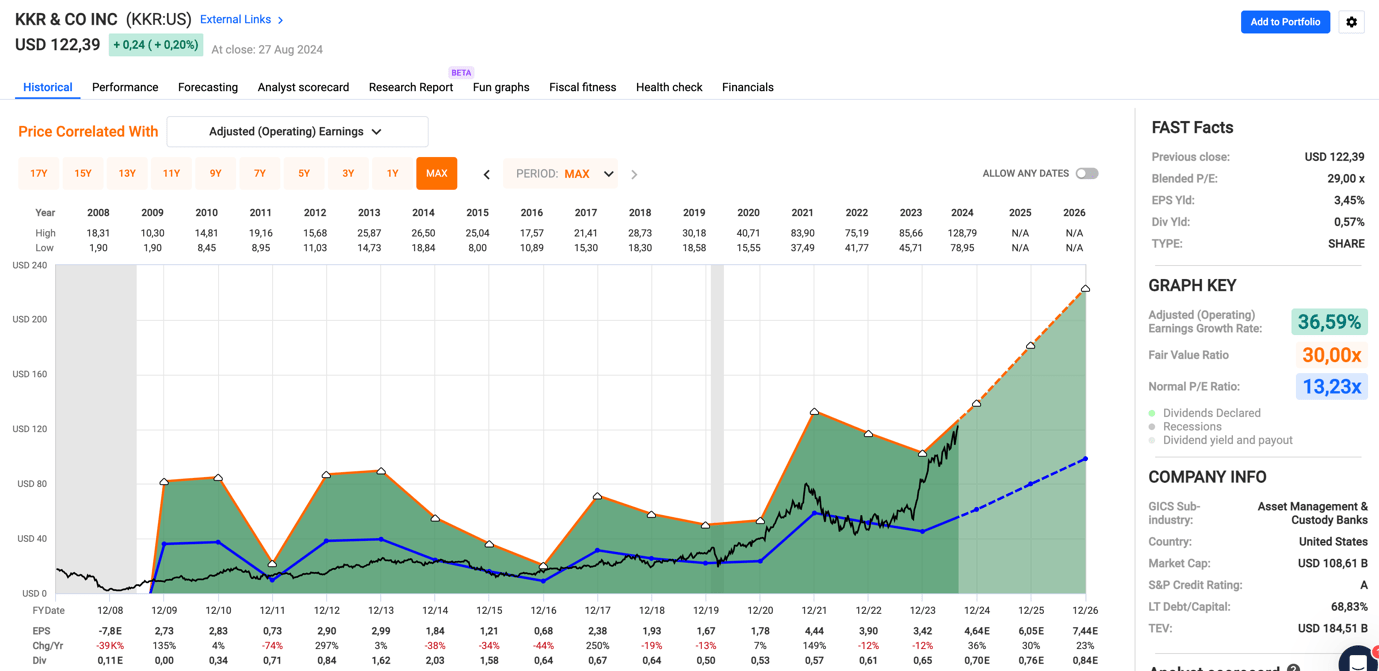

Using the FactSet data from the chart below, the company is expected to grow its EPS by 36% this year, potentially followed by 30% and 23% growth in 2025 and 2026, respectively.

FAST Graphs

As such, despite trading at 29x earnings, KKR has a $138 consensus price target, 13% above its current price.

It’s hard to disagree with that, as the company is working on one of the strongest and potentially most consistent growth streaks in recent history.

Just like Blackstone, we believe KKR is a great buy on dips.

In Closing

Private equity is breaking new ground, even in the NFL.

With the league opening its doors to select firms, the landscape of sports ownership is changing.

This shift is more evidence of the growing influence of private equity, which has ballooned into a multi-trillion-dollar industry.

Firms like Blackstone and KKR are leading the charge, deploying massive capital and leveraging their market dominance to fuel impressive growth.

As these giants continue to shape industries, including sports, their strategies and success make them compelling investment opportunities.

Author’s Note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed to assist in research while providing a forum for second-level thinking.

{kind=link}