Klaus Vedfelt

The Q2 earnings season has been a big boon for many out-of-favor rebound companies. Especially as the stock market is falling sharply from all-time highs on growing recession fears, value-oriented stocks are looking more and more appealing. But caution and careful stock-picking is of the utmost importance: needless to say, not all fallen companies have the ability to overcome their struggles.

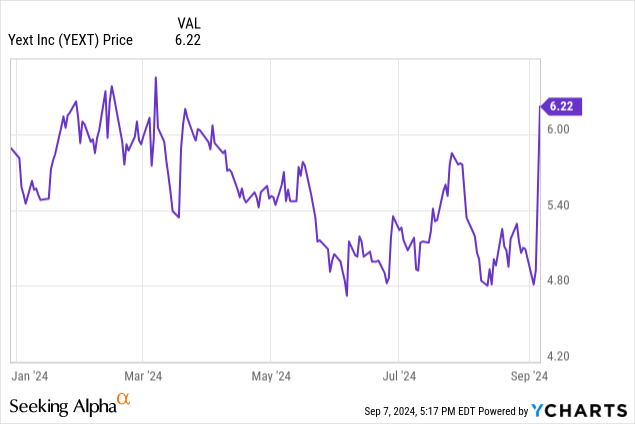

Yext (NYSE:YEXT) is a stock that has, in particular, seen an unexpected surge. The software company, which describes itself as a “knowledge graph” for enterprises, has rallied more than 25% after reporting stronger-than-expected Q2 results (though even this rally has only been able to reverse YTD losses, and the stock is roughly flat since January). The question for investors now is: is the Yext rally sustainable, or is this company still on a collision course?

I last wrote a bearish note downgrading Yext in June, when the stock was trading in the mid-$5s. I wasn’t expecting the post-Q2 rally, but nor does Yext’s incremental news make me any more bullish on this stock.

Broadly: investors are cheering the fact that Yext’s direct ARR (that is, sales to customers by Yext’s own sales force, and not reseller partners) has returned to growth after a hiatus of more than a year. At the same time, however, overall ARR is still declining.

We should also consider the fact that Yext’s original product, Listings (a tool to help business manage their location data on platforms like Yelp and Google Maps), has tremendous exposure to businesses like retail shops and restaurants. We’ve already heard dire news from Yelp and other companies that have concentration to this vertical that these companies are fearing a pullback in consumer spending, and thus curtailing their spend: ultimately another factor that is dragging on Yext’s retention rates and ability to land new deals.

Here are all the core red flags that I see in Yext:

- Yext has seen persistent declines in ARR and customer retention. Yext continues to see customer defection and declining ARR, a situation which may worsen with declining macroeconomic conditions.

- Alternatives including DIY abound. A quick scan of online reviews of Yext’s product suggests that its functions can be built in-house at a much lower cost.

- Yext’s guidance, particularly on the bottom line, seems like stretch goals that will be difficult to hit. The company is expecting 15%+ adjusted EBITDA margins, even when its current margin profile is in decline. Layoffs can only help so much if the top line continues to decay.

The only appeal to Yext (as well as the only real factor that I see as an upside risk in this stock) is the fact that it remains cheap, even after its post-earnings rally.

At current share prices near $6, Yext has a market cap of $795.7 million. After we net off the $234.8 million of cash on Yext’s latest balance sheet, its resulting enterprise value is $560.9 million. Meanwhile, the company is still guiding to full-year FY24 adjusted EBITDA of $66-67 million, which is a 16% margin against the company’s revenue range of $420-$421 million.

This puts Yext’s valuation at 8.4x EV/FY24 revenue. Though seemingly cheap when the S&P 500 continues to trade at a near-20x forward P/E multiple, I still consider Yext a value trap. A software company that is struggling to grow, in my view, is a company that is accelerating toward obsolescence. Retention rates are still poor, signaling a weak product that doesn’t have mission-critical usage for clients. As such, I’d recommend staying on the sidelines here.

Q2 download

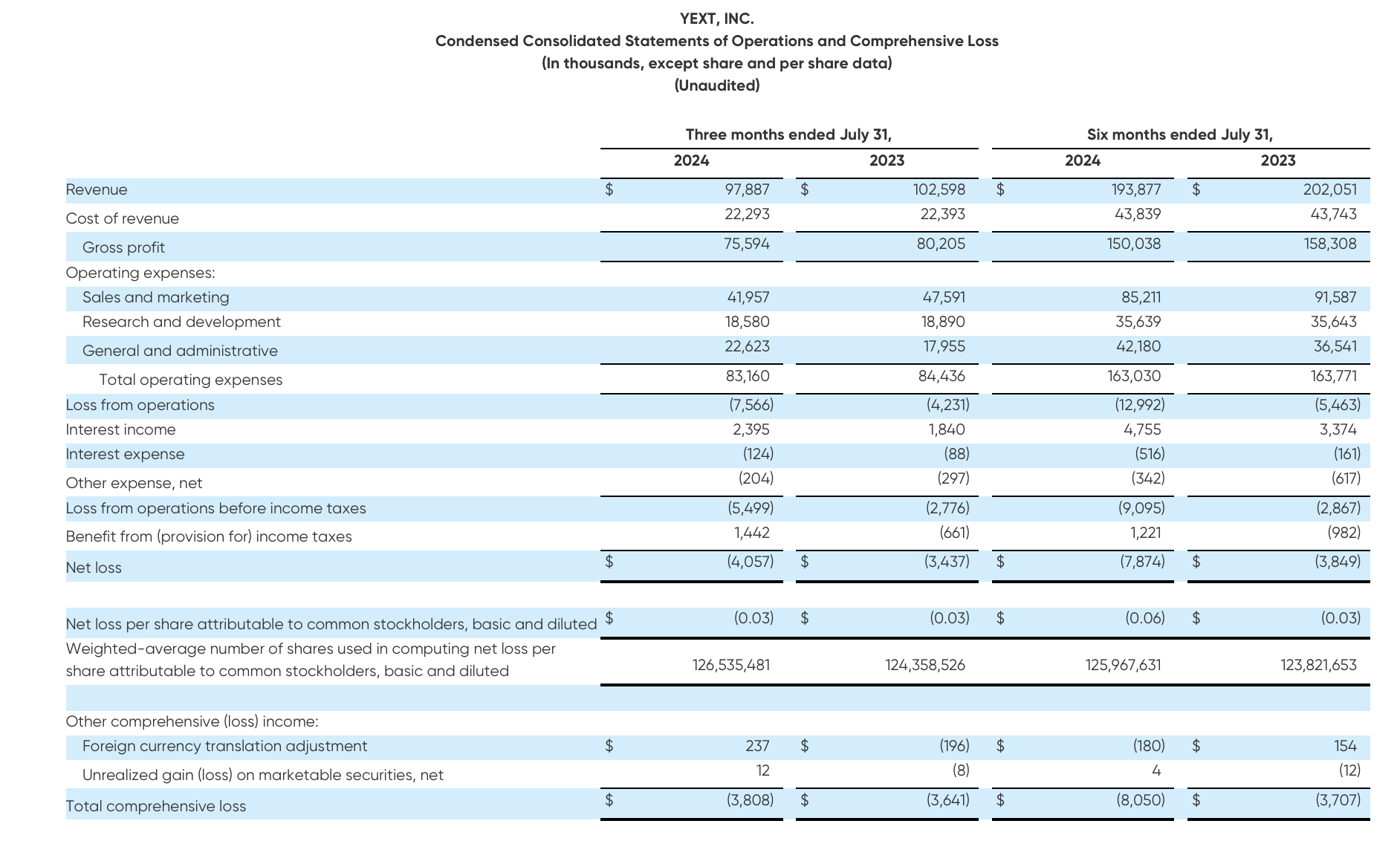

Let’s now go through Yext’s latest quarterly results in greater detail. The Q2 earnings summary is shown below:

Yext Q2 results (Yext Q2 earnings release)

Yext’s revenue declined -4.6% y/y to $97.9 million. Despite the positive post-earnings reaction, the company actually slightly missed against Street expectations of $98.2 million (-4.3% y/y).

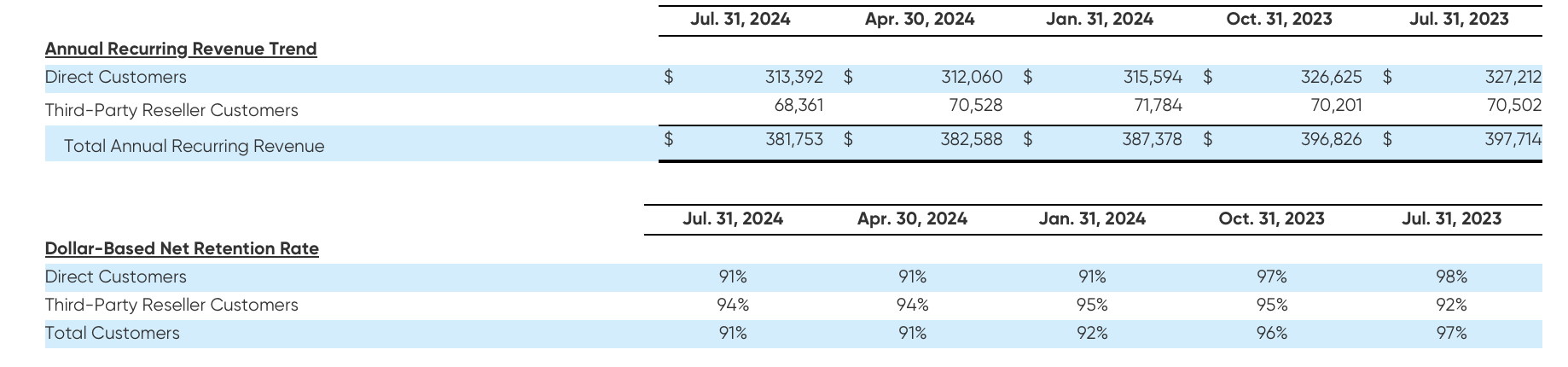

The big issue for Yext, however, is continued slippage in ARR. Despite the company touting its recovery in direct channel ARR, total ARR declined -4% y/y and lost ~$1 million sequentially to end the quarter at $381.7 million.

Yext ARR and retention (Yext Q2 earnings release)

Now, Yext management believes that the decline in reseller ARR isn’t completely representative of the company’s health, as customers who sign up through resellers don’t often commit full amounts in advance (which would be reported in ARR). Still, the company is citing challenging sales cycles. Per CEO Michael Walrath’s commentary on the Q2 shareholder letter:

While committed Reseller ARR declined roughly $2.1 million in Q2, we note that there is a shift happening in this business. Pricing in our Reseller channel differs from pricing in direct deals. Because our partners have less visibility into their required volumes over time, most of our Reseller deals involved some level of committed consumption (which we report as Reseller ARR) and a structure for usage-based growth beyond that commitment. We see a lot of opportunity to strengthen and expand our Reseller business by focusing on more usage-driven elements. This shift pressures committed Reseller ARR, as a higher percentage of a deal’s expected value is uncommitted and therefore not included in ARR. While this impacted total ARR, the revenue contribution from Reseller was stable relative to Q1.

I’d like to take a moment and specifically address questions on the macro environment. There is a lot to consider, and predicting how enterprises will manage their IT spending has proven to be a challenge across the software sector. We see many drivers of uncertainty today. The interest rate environment, a looming election, geopolitical risks, questions of a consumer recession. Our customers continue to be cost conscious and conversations with C- level customers and prospects indicate that the cautiousness we have seen will likely continue until there is more clarity on the risks outlined above. Our current outlook anticipates stable to modestly growing ARR this year in spite of the headwinds discussed above. The market remains unpredictable and will update our outlook as things evolve.”

It’s worth noting as well that Yext is only reporting a 91% net revenue retention rate (compared to ~110s for many software companies), while gross retention was in the 80s. To me, this continues to indicate that Yext isn’t exactly a “sticky” product that customers will strive to keep paying the bills for when times are tough.

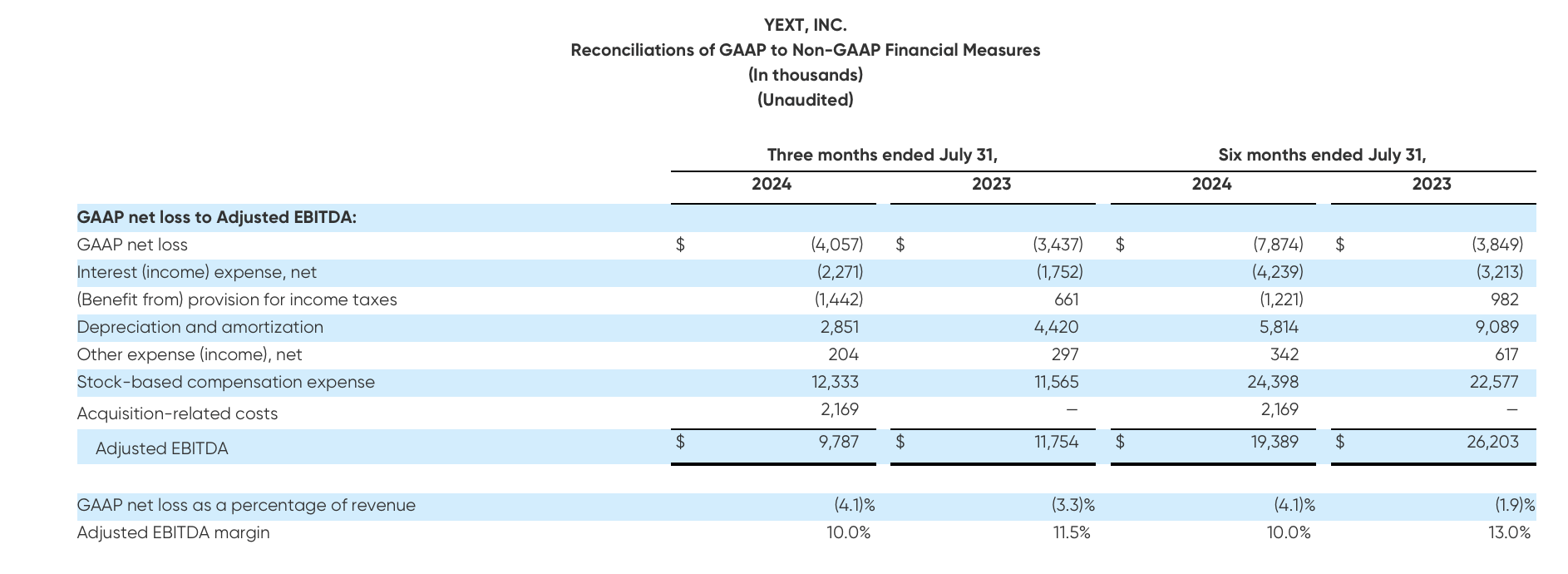

From a profitability perspective, Yext’s Adjusted EBITDA declined -17% y/y to $9.8 million, representing a meager 10% margin – 150bps worse than the year-ago quarter. We note as well that YTD margins are also 10%, and that the company on a nominal basis has generated less than $20 million in adjusted EBITDA this year. Guidance is calling for a midpoint of $66.5 million in adjusted EBITDA and a 16% margin. The company is expecting EBITDA to improve from a combination of ARR improvements and sales productivity boosts, as well as further resource allocation and cost management – but as we haven’t seen any evidence of this yet as ARR is sliding, I wouldn’t truly bank on Yext faithfully executing to these targets.

Yext adjusted EBITDA margins (Yext Q2 earnings release)

Key takeaways

Especially as we head into a potential recession that saps away at Yext’s core clientele for its Listings product, I’d be wary of the recent rebound rally in Yext, as recent history has shown us that the company is more than capable of disappointing us sharply. With declining ARR, deteriorating EBITDA margins, and a looming recession that will pressure IT budgets, I’d continue to sell Yext from here.

{kind=link}