Flashpop/DigitalVision via Getty Images

Tilly’s (NYSE:TLYS) 2Q24 results were in line with the company’s guidance but very negative, at 8% negative comparable sales. The quarter’s absolute results were a little better, and earnings broke even because of the inclusion of one back-to-school week that was not part of 2Q23.

Overall, the company’s consistent falling sales point to challenges that are not only macroeconomic but also of the model. Last quarter, management had commented on assortment problems, and this quarter, the topic reappeared. It is positive that management is working on solving these issues, but the model problems signal a return to pre-pandemic profitability is not a given.

Based on the above, and despite Tilly’s stock price continually falling (40% since my first article), I still do not believe the stock is an opportunity. If the company cannot prove that its model can be profitable, then there is no price low enough at which I would Buy. For that reason, I maintain my Hold rating.

2Q24 results

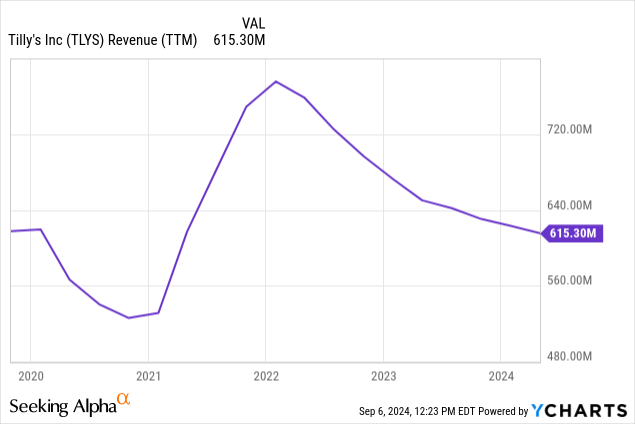

Positive absolutes, negative comps: Unadjusted results for Tilly’s 2Q24 were good. Revenues grew 2%, the company gained 300 bps in gross margins, and posted break-even net income (a small $70 thousand loss).

On the other hand, the comparable results were terrible, at negative 8% YoY. The company has not had a positive comparable quarter since the 2021 fiscal year, and 2Q24 was its best comparable since.

The company does not provide comparable margins, but the improvement in gross margins and operating margins of 2Q24 can’t be separated from the positive absolute sales (caused by the shift of a back-to-school week).

3Q24 pays back the improvement: The company correctly warned that 3Q24 results would be more challenging on an absolute basis, as the extra BTS week from 2Q24 is lost. The company is expecting operating income losses of close to $11 million, in what should be one of the best quarters for the company seasonally.

On the other hand, the comparables are expected to improve, falling only between 2% and 6%. In part this improvement is generated by comparables getting easier, as the company starts to anniversary the big fall in late 2022 and early 2023.

Recognition of interval problems and reform: In previous earning calls, the company blamed the challenging macro for the negative sales performance. Since my first article, I warned that despite the macro being challenging, Tilly’s may be suffering from other more permanent factors, like competition from cheap Chinese e-tailers (very popular among the company’s core demographic of Gen-Z), or problems in assortment. If the macro was really bad, it would be impossible for several apparel retailers targeting approximately the same demographic to be posting good comparables. Examples abound like Abercrombie & Fitch (ANF), Urban Outfitters (URBN) and American Eagle (AEO).

Last quarter, the company’s Chairman and interim CEO had already recognized bad merchandising practices, by saying that: ‘In the past, unfortunately, we gave the merchandise away, it’s way under cost. There was no reason for that, but it happened.’

This quarter, the CEO went one step further by saying that: ‘While the macroeconomic environment remains challenging for our core customer demographic of teens, young adults and young families, we also believe certain merchandising decisions on our part limited us from performing better in the second quarter.’

The company also launched its first brand campaign, called Discover Your Style, and is targeting micro-influencers to increase brand awareness. Although top-of-funnel efforts take a long time to pay off and are not the best strategy for a retailer, these efforts and the recognition of problems are healthy.

Valuation is challenging given model questions

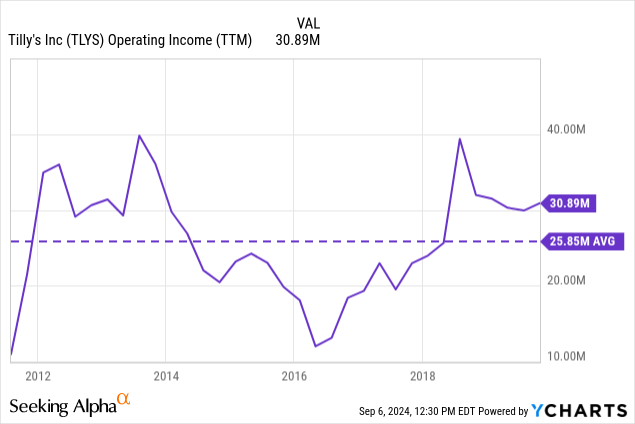

Today, Tilly’s trades at a market cap of $145 million and has about $75 million in cash and no debt. That yields an EV of about $70 million. If we compare this figure with average pre-pandemic operating income of $25 million, the stock is incredibly cheap.

However, the company is not in the same situation as before the pandemic. Tilly’s is not simply undergoing a challenging cycle in the economy. Rather, it is unable to offer the products that its customers want at the price they want them. This puts a question mark on the company’s viability, making the valuation very challenging.

However, we can still forecast what would be needed for the company to return to breakeven. The company’s fixed expenses are about $350 million (SG&A of $290 million TTM and lease expenses included in CoGS for $60 million). The company’s adjusted contribution margin (gross margin adding back leases) is 52% TTM. In order to breakeven with these figures, the company should post revenues of $675 million, or an 8.5% improvement from today’s $620 million (coincidentally the improvement in 2Q24 sales from the extra week that led to the quarter breaking even). In order to generate net profits of $7 million (a 10% earnings yield on the $70 million EV), Tilly’s should sell about $692 million, or 12% above current levels.

We can see that the difference between a nonviable business model and a healthy return is very little in terms of sales because of operating leverage. This could present an opportunity for speculative readers to bet on the company’s recovery. However, in my opinion, given the company’s lack of effective reform, and the challenging macroeconomic outlook, this speculation is not attractive. For that reason, I maintain my Hold rating on Tilly’s.

{kind=link}