HappyBall3692

Real estate investment trusts, or REITs, have experienced a strong rally recently.

During the last 30 days, the sector is up by 4.17% (third, behind Utilities and Consumer Staples).

During the past 3 months, REITs are up by 7.93% (second, behind only Information Technology).

I’ve been calling for this rally for a while now. For over a year now, I’ve highlighted beaten down REITs as coiled springs because of the interest rate overhang that would eventually be removed. When that happened, I thought the sector would soar.

Well, it turns out I was right.

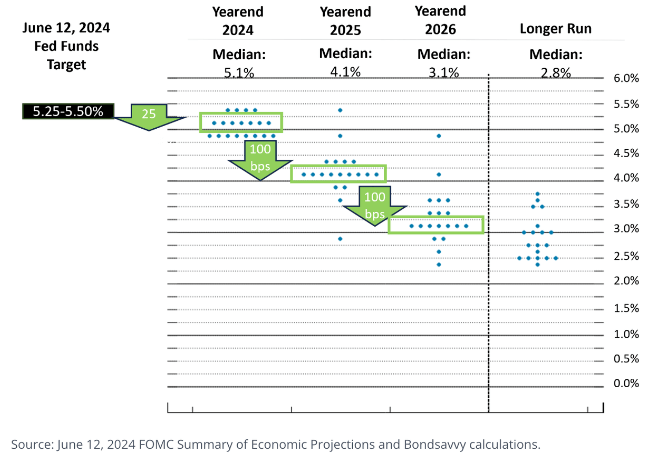

Recent economic data showing a slowing economy and cracks in the job market have led to a lot of talk about rate cuts. The estimates, in that regard, will vary from analyst to analyst and economist to economist; however, the overall consensus clearly points to numerous cuts over the coming years.

Bondsavvy

Now that rate cuts have taken over the macro narrative, the sentiment surrounding the real estate sector has changed… rapidly.

To me, it was only a matter of time before rates fell. I didn’t believe in the “higher for longer” thesis that many bears on the sector held. Do I expect to see the US enter back into ZIRP policy in the near-term? No, I do not. But, I didn’t expect to see rates hover in the 5% range forever, either.

REITs got two black eyes when rates rose, being high-yielding stocks with interest rate sensitive operations. But, once rates fell, I knew those two headwinds would turn into strong tailwinds, driving fundamentals higher (as lower rates led to more growth opportunities for real estate developments/acquisitions) and demand for shares higher (as income-oriented investors fled the bond market and back into risk assets).

Many savvy investors saw this writing on the wall as well. They piled into REITs while their valuations were depressed and now, they’re glad that they did.

But now, questions arise… what to do after the recent rally?

Are there still bargains to be found?

Or, has the market gotten ahead of itself (as it tends to do) when it comes to the bullish sentiment surrounding REITs?

To answer those questions, I put together a few tables breaking down the fundamentals of some of my favorite REITs, comparing their current valuations to historical data.

You might be surprised by what you see below.

There are certain blue chip REITs that definitely look overvalued after their recent run-ups.

However, there are others that trade with attractive margins of safety and therefore, still offer strong upside potential.

That’s good news for people who’re underweight REITs and still looking to buy into the sector.

That’s good news for people still rotating out of fixed income and back into high-yield stocks.

And, that’s good news for people who’ve been invested in REITs for years (like me) and want to see their long-held positions continue to compound higher.

Breaking Down Blue Chip REITs

When thinking about this article, I decided to focus on only the highest quality REITs for a couple of reasons:

-

Because when markets get volatile like they have recently, I know that many investors flock to safety in blue chip names.

-

Because oftentimes, the highest quality REITs trade with the highest valuations attached to them and therefore, I wanted to see what sort of margins of safety could still be found in the high-quality space.

To separate a list of blue chips from the rest, I decided to look at the new “Risk Ratings” on the iREIT® + Hoya Ratings spreadsheet. These are 1-5 ratings (1 being the lowest risk, 5 being the highest) and we provide them for hundreds of REIT and home builder stocks.

There were only 10 stocks with risk ratings below 2.0, so to me, that was a good place to start.

As you can see below, nearly all of these companies have performed well recently, with average 30-day price gains of 4.2% and average YTD price gains of 7.1%.

|

Company |

Ticker |

Property Type |

1-Month Price Returns |

YTD Price Returns |

iREIT® + Hoya Risk Rating |

|

AVB |

AvalonBay Communities |

Multifamily |

5.3% |

14.9% |

1.5 |

|

EQR |

Equity Residential |

Multifamily |

4.5% |

16.7% |

1.5 |

|

MAA |

Mid-America Apartment |

Multifamily |

8.8% |

13.7% |

1 |

|

UDR |

UDR, Inc. |

Multifamily |

2.6% |

9.2% |

1.5 |

|

CPT |

Camden Property |

Multifamily |

9.0% |

20.5% |

1.5 |

|

PSA |

Public Storage |

Self Storage |

4.6% |

4.7% |

1.5 |

|

PLD |

Prologis |

Industrial |

0.9% |

-7.8% |

1 |

|

REXR |

Rexford |

Industrial |

-0.7% |

-10.3% |

1.5 |

|

INVH |

Invitation Homes |

Single Family |

-0.6% |

3.4% |

1.5 |

|

AMH |

American Homes |

Single Family |

5.8% |

6.4% |

1.5 |

|

Average |

4.2% |

7.1% |

You’ll notice that these companies are highly concentrated in just a few subsectors of the REIT space.

That’s a function of the algorithm that drives our results; however, I plan to write a follow-up to this piece, focusing on the highest rated REITs from the other areas of REITdom that didn’t make that sub-2.0 Risk Rating cut in the coming weeks.

For now, though, we’re going to focus on the 10 REITs with the best Risk Ratings.

Bear with me because each of these tables has plenty of numbers on them.

Below is the valuation chart. I’ve included each stock’s blended P/AFFO ratio alongside its historical averages for the year-to-date and trailing 3, 5, and 10-year periods.

To me, this is a quick and easy way to see what the recent rallies have done to each stock’s valuation multiple. In most cases, you’ll see that recent rallies have driven blended multiples up above their year-to-date averages, towards their long-term (10-year) averages, but in most cases, they’re still below the 3 and 5-year numbers. All of that makes sense; however, there are a few stocks that stand out from a valuation standpoint as still having room for multiple expansion ahead.

|

Company |

Ticker |

Blended P/AFFO Ratio |

YTD- Average P/AFFO |

3-Year Average P/AFFO |

5-Year Average P/AFFO |

10-Year Average P/AFFO |

|

AVB |

AvalonBay Communities |

22.0x |

19.7x |

23.9x |

21.1x |

22.6x |

|

EQR |

Equity Residential |

22.6x |

19.4x |

24.6x |

22.3x |

23.2x |

|

MAA |

Mid-America Apartment |

19.0x |

16.3x |

24.4x |

20.6x |

19.2x |

|

UDR |

UDR, Inc. |

19.3x |

17.3x |

22.9x |

21.3x |

21.9x |

|

CPT |

Camden Property |

20.4x |

16.7x |

24.8x |

22.5x |

21.4x |

|

PSA |

Public Storage |

21.9x |

21.1x |

24.8x |

21.9x |

23.0x |

|

PLD |

Prologis |

27.8x |

29.5x |

34.8x |

28.0x |

27.9x |

|

REXR |

Rexford |

27.4x |

32.6x |

43.9x |

39.0x |

35.2x |

|

INVH |

Invitation Homes |

22.8x |

22.7x |

26.4x |

25.1x |

n/a |

|

AMH |

American Homes |

25.1x |

24.5x |

27.4x |

25.6x |

39.5x |

Looking at this list, UDR (UDR), Rexford (REXR), and Invitation Homes (INVH) stand out as the potential best values (looking at their current blended P/AFFO multiples compared to their longer-term averages).

Many stocks on this list are still trading well below their 3 and 5-year averages; however, UDR is still trading at a fairly wide discount to its 10-year average and INVH is trading well below its 5-year average (which is interesting because AMH shares have run back up to that 5-year average mark).

The next chart will show each stock’s forward-looking bottom-line growth consensus versus its trailing 10-year average.

|

Company |

Ticker |

2024 AFFO Growth Est. |

2025 AFFO Growth Est. |

2026 AFFO Growth Est. |

10-year Average AFFO Growth Rate |

|

AVB |

AvalonBay Communities |

5% |

5.0% |

6.0% |

7.20% |

|

EQR |

Equity Residential |

0% |

7.0% |

0.0% |

3.20% |

|

MAA |

Mid-America Apartment |

-4% |

1.0% |

5.0% |

6.80% |

|

UDR |

UDR, Inc. |

-1% |

4% |

5.0% |

6.40% |

|

CPT |

Camden Property |

-2% |

2.0% |

7.0% |

6.00% |

|

PSA |

Public Storage |

2% |

8.0% |

6.0% |

7.50% |

|

PLD |

Prologis |

-4% |

17.0% |

11.0% |

15.60% |

|

REXR |

Rexford |

10% |

15.0% |

16.0% |

14.10% |

|

INVH |

Invitation Homes |

5% |

4% |

8% |

4.8% (5-year average) |

|

AMH |

American Homes |

6% |

6.0% |

7.0% |

10% (5-year average) |

As you can see above, there are mixed results here (as far as the expectations that these companies meet their historical growth averages moving forward go).

For instance, AvalonBay’s (AVB) forward-looking estimates in the mid-single digits aren’t that far from its 10-year average in the 7.2% range. Yes, they’re slightly lower, but it’s reasonable to assume that they could beat Wall Street’s expectations and produce 6-7% AFFO growth moving forward.

However, a company like American Homes 4 Rent (AMH) is expected to post much slower (albeit, still positive) growth moving forward than it has produced during the last decade.

The 5-7% growth that AMH is expected to produce moving forward is great; however, it’s much lower than the 10% growth that investors are used to and therefore, it seems reasonable that shares should trade discounted to its long-term averages (being that they were propped up by higher fundamental growth).

Companies like Mid-America Apartment Communities (MAA), UDR, Camden Property (CPT), and Prologis (PLD) all also fall into this category of blue-chip REITs with 3-year forward-looking growth average estimates that fall below their trailing 10-year averages.

On the other hand, REXR and INVH are still expected to post forward growth that is essentially in-line with trailing growth averages.

Rexford’s 3-year forward average AFFO growth rate is expected to be 13.7%. That’s pretty close to its 14.10% 10-year trailing average.

INVH’s 3-year forward average AFFO growth rate is expected to be 5.7%. That’s above its 5-year trailing average of 4.8%.

So, with that being said, these are the two stocks that best pass the screens laid out in this data set.

FAST Graphs FAST Graphs

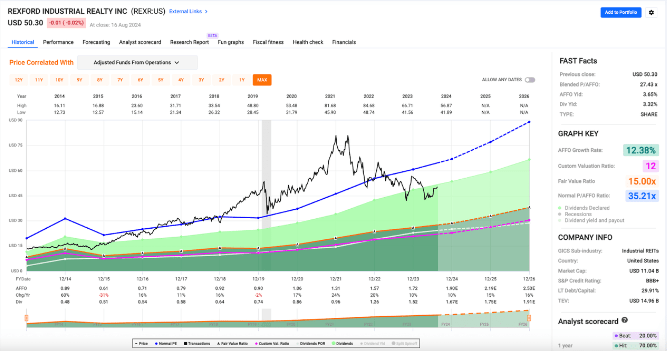

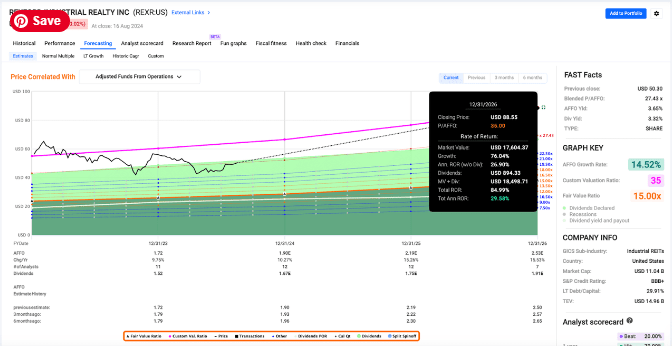

Looking at the FAST Graphs above, you’ll see that REXR’s sell-off since the highs in 2021 has driven its share price (black line) well below its long-term average P/AFFO (blue like). In the event of multiple expansion back up to that ~35x area (which appears to be justified, looking at forward AFFO growth prospects) we’re looking at a stock that could generate annualized returns of nearly 30% over the next 2.5 years. That’s a total return of ~85% between now and the end of 2026.

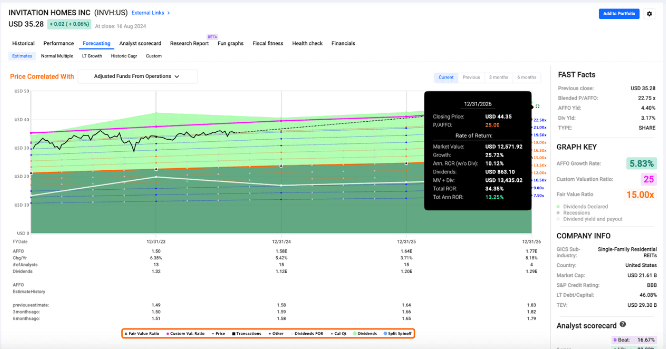

FAST Graphs FAST Graphs

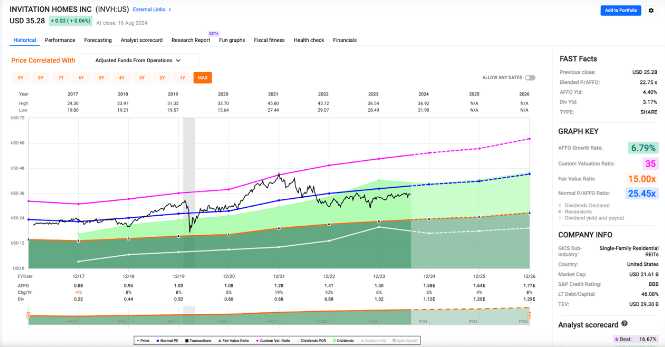

You’ll see the same story playing out here with INVH as well (though, to a lesser extent).

INVH’s share price (black line) remains below its historical average multiple (blue line) and in the event of multiple expansion via mean reversion, we’re looking at a stock that could generate annualized total returns north of 13% over the coming years. That would represent total returns of nearly 35% between now and the end of 2026.

Conclusion

The fact is, a lot of great value has dried up in the real estate sector recently due to sentiment shifting from bearing to bullish on REITs.

I wouldn’t be surprised to see this trend continue as talks of rate cuts continue; however, if the rally picks up pace it’s going to be paramount that investors pay close attention to valuations, making sure that they aren’t overpaying for REITs (no matter their quality).

This article shows that there are still bargains to be had in the real estate sector, just not as many as there were at the beginning of the year.

A year ago, you could have thrown darts at a list of REITs to hit highly undervalued stocks likely to generate double-digit upside. That’s not the case any longer.

Patience and discipline will be key moving forward. But, I still like the REIT sector a lot through the impending rate cut cycle. Investors just need to be selective moving forward.

{kind=link}