sefa ozel

Executive summary

Trip.com (NASDAQ:TCOM) owns the leading travel sales platform in China, with an estimated 50% market share and a growing presence in South East Asia.

The group owns the leading online travel brands in the market and can drive traffic to its platform efficiently, providing merchants with the largest pool of potential customers.

As of late, the company’s profits have been growing rapidly as travel restrictions out of China are being eased and travellers flock to Thailand, Japan and the West.

Over the longer term, the travel market is expected to grow faster than the overall Chinese economy, as a growing share of income is being allocated to discretionary consumption.

Trip trades at 14X forward earnings, considerably lower than international peers such as Booking, and arguably offers better long-term growth prospects.

Chinese companies with strong growth momentum can reward shareholders handsomely; however, we do have to note that the risk profile of these stocks is elevated due to potential macro and company-level governance issues.

Earnings are roaring higher as China relaxes travel restrictions

During the second quarter of FY2024, the company’s revenues increased by ~14% compared to the same period last year, while adjusted non-GAAP earnings grew by ~47% as profit margins have expanded. Both domestic and outbound bookings as well as global distribution were driving the sales uplift.

Accommodation reservations were driving the sales uplift, but flight prices have started to moderate as capacity is built back up. Lower flight pricing is not an issue for Trip as accommodation is the primary driver of profits and increased flight capacity enables higher accommodation sales.

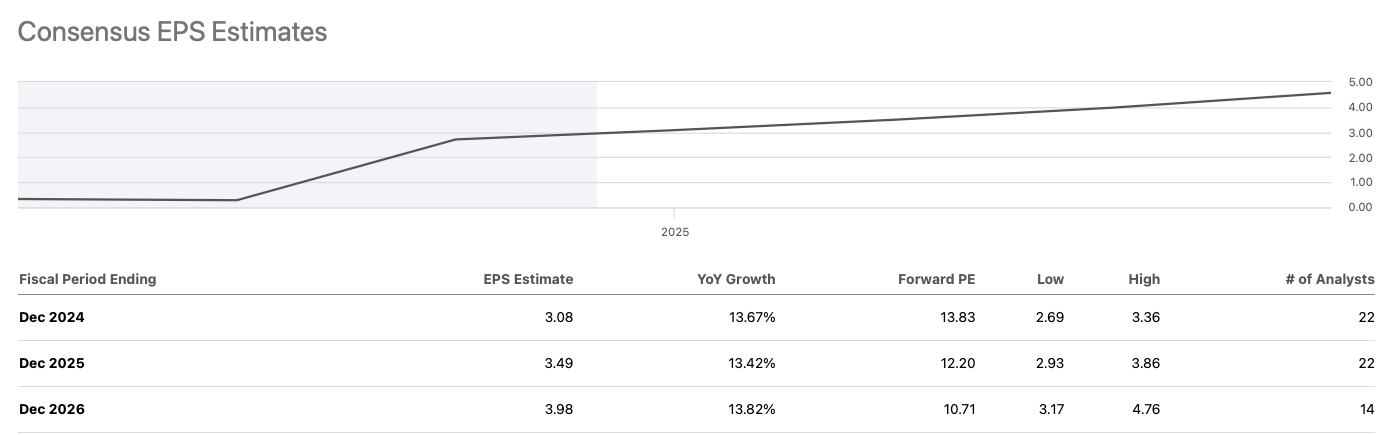

Travel restrictions were lifted in the first quarter of last year; therefore the company has faced tougher comparables in the second quarter; however, Trip is expected to maintain strong earnings growth momentum for the remainder of the year and increase earnings per ADS from ~$2 last year to about $3 this year.

Seeking Alpha

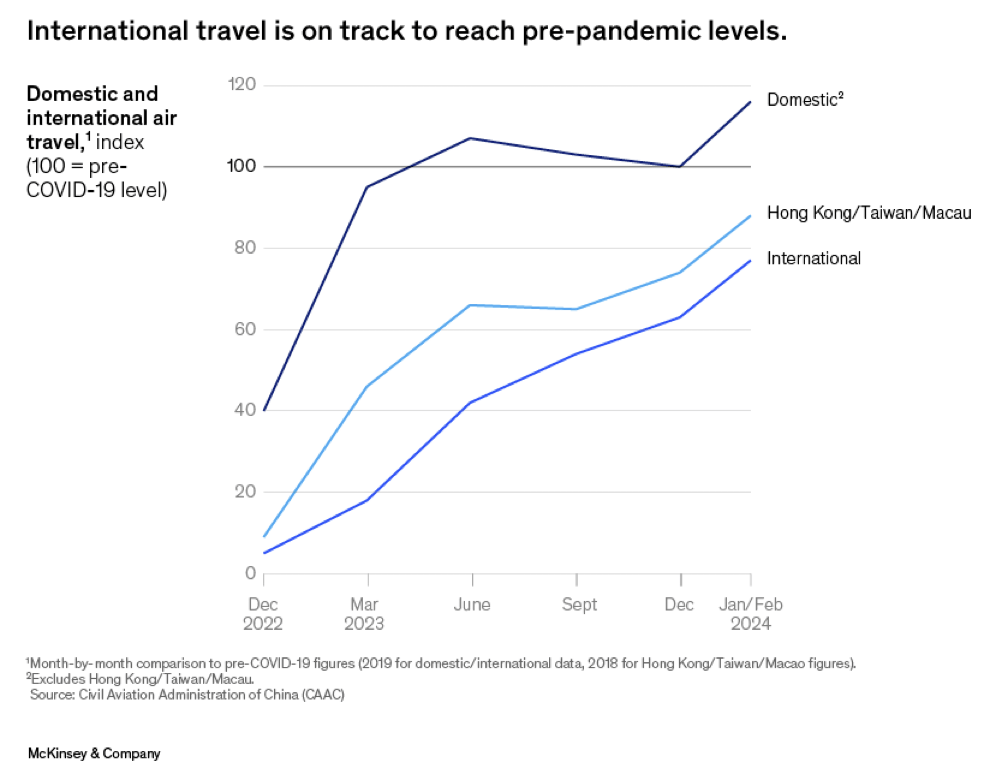

Even though domestic tourism has now largely recovered, international travel is still considerably below pre-Covid levels in terms of volume. International flight capacity has only recovered to 70% of pre-Covid levels.

Air travel recovery (McKinsey)

We expect outbound travel to continue trending up as international flight capacity is built back up and Chinese travel restrictions continue being lifted. Most likely, the elevated demand will extend beyond this year, as consumer behaviour will take time to adjust.

Trip is the leading online travel agent in China

China is the core market for Trip, they also have a strong foothold in the international markets which can serve as a platform for growth. Trip Group owns Ctrip, the largest online travel agent in China, as well as Qunar, the leading travel aggregator platform in the country. Ctrip controls about 36% of the Chinese market and is twice as big as the second-largest competitor, Meituan (OTCPK:MPNGF).

The company also owns the internationally focussed Trip.com and Skyscanner brands and has strategic investments in India’s MakeMyTrip (MMYT) as well as Tongcheng (OTCPK:TNGCF).

The business model of Trip is akin to Booking (BKNG) and Airbnb (ABNB), where the company acts primarily as an agent rather than a merchant of accommodation and flights. The company’s competitive position primarily relies on its ability to drive traffic to its platform cost-effectively.

Leading retail platforms can leverage marketing spending across the largest customer base and therefore usually have the lowest customer acquisition costs. The largest online agents tend to dominate the markets in the U.S. and also in China.

Aggregators such as Google (GOOG), Kayak or Qunar could in theory weaken the pricing power of online travel agents, however, most of them are now owned by OTA’s themselves. Qunar was initially part of Baidu (BIDU), the Chinese Google, but was later acquired by Trip.

Douyin is unlikely to undermine Trip.com

Probably the most significant threat to the position of Trip could come from Douyin (aka Chinese TikTok). As we mentioned, efficient traffic acquisition is the key to the competitive position of Trip. Douyin can also leverage the organic traffic that the platform generates to sell many types of products, including travel.

Under this scenario, online traffic could move from Douyin to an influencer-provided link straight to the hotel operator, circumventing Trip altogether. Douyin is likely to carve itself out a niche in the travel booking market; however, we doubt that it could achieve a dominant position.

OTA’s such as Ctrip have the largest selection of accommodation options and therefore can cater to the largest share of the market. The hotel market is very fragmented and the majority of the inventory is provided by independent operators, that cannot afford to hire influencers. For the majority of hotels, Ctrip will still be the preferred marketplace to sell.

YouTube travel vloggers, for example, have been posting booking links at the bottom of their videos for years, but that has not undermined the position of Booking in the U.S.

We, therefore, expect Trip to maintain a strong share in China and benefit from the gradual market growth as discretionary consumer spending is expected to exceed GDP growth.

Chinese travel industry offers strong growth potential

Despite the strong earnings reported over the past quarter, Trip’s share price has declined 25% since the last earnings announcement. Chinese Technology and Consumer Discretionary companies are particularly exposed to declining consumer confidence as well as rising geopolitical tensions. Most recently, consumption could have started bouncing back as inflation picked up to 0.5% in July.

Despite the current issues faced by the Chinese economy, we believe that long-term growth prospects continue to be solid. The Chinese economy is projected to grow by ~5% in 2024, driven by the strong services sector, which includes tourism.

The pent-up demand as well as accumulated savings are likely to drive the tourism industry over the next couple of years as travel restrictions have now been lifted. Both domestic and international travel sectors are seeing strong growth, and this trend is likely to continue as more travel options become available and confidence in travel fully returns. As McKinsey puts it:

As travel rebounds, the pent-up demand and accumulated wealth during the pandemic seem to be channelled into more luxurious and high-value purchases, indicating the Chinese consumer’s desire to invest in unique and high-end experiences. This early wave of post-pandemic travellers from China may skew toward wealthier consumers, as they have more disposable income and can afford the higher flight and hotel costs that are prevalent today.

Over the long term, the travel industry should also grow at rates exceeding GDP appreciation. As the incomes of the Chinese continue to increase and consumer confidence recovers, two important changes should happen.

Number one, – the share of income allocated to discretionary items, such as cars and travel, should increase. It is only natural that as consumers become wealthier, necessities such as food and shelter take up less and less of their earnings. Number two, – the Chinese still save 30% of their earnings, which is very high. Increasing the share of earnings allocated to consumption would propel consumer discretionaries, such as travel, considerably higher.

Overall, it is highly likely that the Chinese travel industry will continue growing strongly over the short and longer term.

Trip.com is attractively priced, but the lack of shareholder returns is concerning

Trip .com is expected to generate about $3 of earnings per ADR during this financial year, the company’s stock trades at c14X these earnings. Given the growth prospects and how profitable the business is, this valuation multiple does seem attractive.

There are issues, however. First of all, what we buy is not a stock but a share of a Variable Interest Entity that has contractual arrangements with the business itself. While we do believe that geopolitical risks are blown out of proportion as China is quite different from Russia, we have to note that shareholder rights are quite limited in Cayman-domiciled VIEs.

As it is quite difficult to enforce your rights with the Chinese ADRs, the shareholders have to rely on the goodwill of the management. In this case, the track record is of utmost importance.

Trip.com despite being quite profitable and very cash generative is not paying dividends and has only engaged in limited share buybacks. They have also attracted criticism for dilutive remuneration policies.

During FY2023, Trip .com generated ~$1.6 billion of free cash flow, excluding working capital movements and stock-based compensation expense, as compared to $1.4 billion in earnings. During the year, businesses paid no dividends and only bought back $0.2 billion worth of stock. The company, on the other hand, has spent ~$1.3 billion on long-term investments.

Trip owns ~$7 billion worth of long-term investments overall. The most significant ones are Tongcheng Travel and MakeMyTrip, though these account for a small share of the overall portfolio. There is considerable uncertainty on how the cash is being allocated.

Long-Term Investments (Trip.com)

It is not uncommon for Chinese companies to make overpriced acquisitions from related parties, and in doing so, channel funds to the controlling parties. We see no signs that this could be the case with Trip; however, we need to dig deeper, but the disclosure is not excellent.

During the last financial year, Trip recorded a share-based compensation expense of RMB1.8 billion ($258 million) and has granted 12.3 million new share options, equivalent to 2% of the share count. At the end of the year, 71.4 million share options were outstanding, equivalent to 11% of the share count.

During the last 5 years, the company’s share count has increased 18% though this was skewed up by the secondary listing in Hong Kong. We do expect the share count of Trip to continue increasing but at a slower pace than before.

Overall, Trip does not seem to be particularly transparent about its capital allocation and shareholder return plans. Unlike many other Chinese tech peers, it has not initiated a considerable share buyback scheme and still pays no dividend. We see this as a significant red flag.

The bottom line

Trip is a leading online travel agent in China with a growing overseas presence. The company controls 50% of the Chinese travel booking market and has a considerable scale advantage over other market players. Trip is able to drive user traffic cost-effectively to its platforms because of this scale, and therefore is attractive to independent hotel operators in particular.

The travel market in China has been growing rapidly as of late due to the removal of COVID-related travel restrictions and increasing international flight capacity. There seems to be a level of pent-up demand and the industry growth will likely continue over the next couple of years. Over the long term, the Chinese travel industry is also expected to grow at rates exceeding GDP appreciation.

Trip.com currently trades at only 14X forward earnings despite these solid growth prospects. Corporate governance seems to be the main sticking point when it comes to investing in Trip.

The company has so far failed to reward shareholders despite strong cash generation. We will therefore Hold out from buying the stock, but we intend to continue following this excellent business. A more shareholder-friendly capital allocation policy could turn us into willing buyers.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}