BrianAJackson

Investment Thesis

MongoDB (NASDAQ:MDB) delivers what some may say a middle-of-the-road earnings results that result in its share price soaring more than 10% after hours. What a shocking reaction by the market.

What’s more, despite management raising its guidance for fiscal 2025, the stock is still priced at 100x forward non-GAAP operating profits.

I’m a tech investor, so I know it’s blasphemous to even mention GAAP earnings, but this company is still incurring more and more GAAP losses.

When the thesis doesn’t make sense, I’ve learned that it makes no sense trying to make sense of the market and it’s best to stick to the sidelines.

Rapid Recap

Back in May, I said:

The problem for investors is that high-growth companies rarely go on sale. They only go on sale when the outlook is horrid. And up until that moment, growth stocks carry a growth premium.

As such, even after the premarket drop [on the back of its fiscal Q1 2025 earnings], MongoDB is still priced at 85x forward non-GAAP EPS. An exorbitant figure. Consequently, I argue, that investors would do well to call it a day here before things get even cheaper. As MongoDB’s high valuation isn’t reflective of its underlying prospects.

Author’s work on MDB

This is a stock that I have asserted for some time doesn’t make sense to be priced as expensively as it is. Accordingly, notwithstanding the market’s cheer for MDB, I remain firmly neutral on this name.

Why MongoDB? Why Now?

MongoDB is a type of database that stores data in a flexible, document-oriented way. Unlike traditional databases that use tables, MongoDB uses collections of documents that can vary in structure. This flexibility allows developers to manage applications more efficiently, especially when dealing with complex data, called unstructured data.

MongoDB is popular among developers, as it’s easy to scale and has the ability to handle a wide variety of data types, making it a go-to choice for data-intensive applications.

MongoDB’s near-term prospects are closely tied to the growth of its cloud-based service, MongoDB Atlas. As Atlas continues to grow-representing 71% of the company’s revenue-it’s becoming clear that this growth is cannibalizing its traditional on-premise database business.

Although on-premise remains important for certain customers, especially those with regulatory needs, the shift to cloud-based solutions is strong. That’s perhaps as far as the bull case goes in my opinion.

Other considerations include the tough quarterly comparisons for the remainder of fiscal 2025, plus macroeconomic pressures affecting customer spending on existing workloads.

Although Atlas has shown resilience, the company’s slower-than-expected recovery in consumption growth and the seasonal slowdown anticipated in Q4 could impact revenue.

In support of the above paragraph, take note of this comment from MongoDB’s CFO, Michael Gordon, from the Q&A section of the earnings call:

The only other things I think I would call out is we saw a slower seasonal rebound in Q1, and so we’re expecting that slower seasonal rebound to occur in Q3 as well. And then as you mentioned, Q4 is a seasonally weaker quarter. And so all those are some of the considerations to think about when you’re thinking about the rest of the year.

With this background in mind, let’s now discuss its fundamentals.

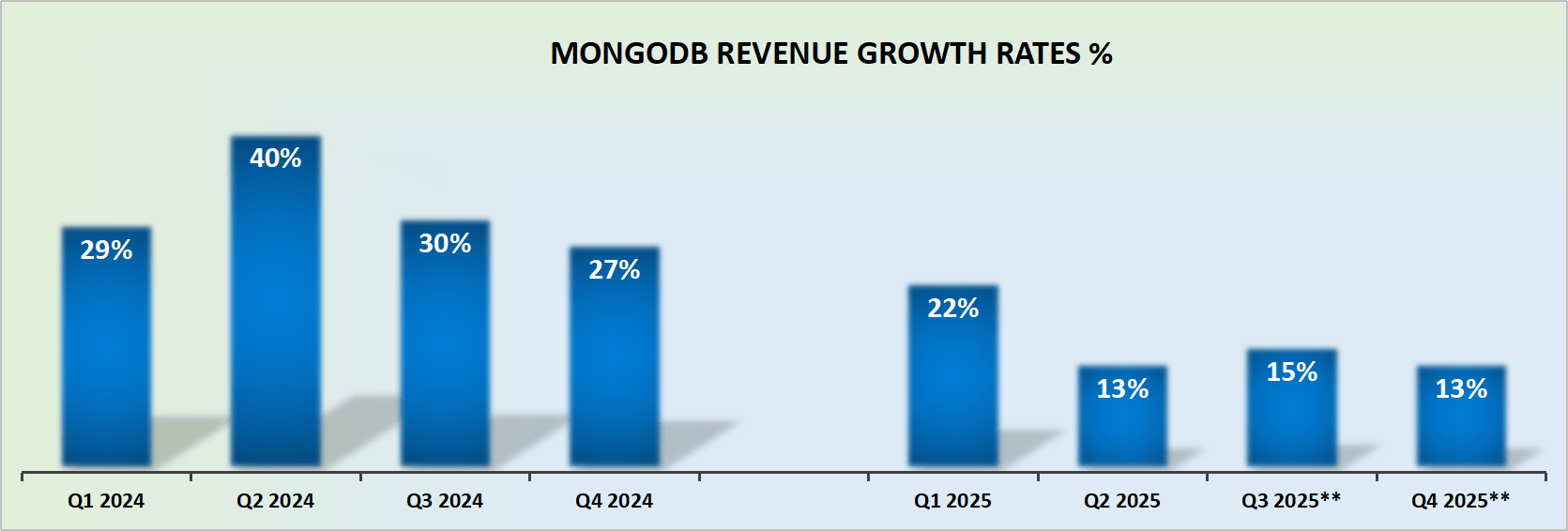

Revenue Growth Rates Upwards Revised a Hair

MDB revenue growth rates

MongoDB is now demonstrably growing at less than 15% CAGR. Note, for the revenue growth rates for fiscal Q3 2025 and fiscal Q4 2025, I used the company’s guidance:

MDB revenue growth rates

I presumed that management would probably beat the high end of their guidance by approximately 2% or thereabouts.

Even if we bake in some level of conservatism into management’s guidance, this is a company that does not deliver premium growth. Premium growth means revenue growth that is consistent, predictable, and at 20% CAGR or higher.

On the contrary, MongoDB’s growth rates have become erratic, choppy, and as you can see in the graph above, unquestionably below 20% CAGR.

In what way is MongoDB a growth company? In my mind, beyond a relief rally, there is nothing in this outlook that supports its premium valuation on its stock.

Perhaps, one could make the case that investors cheered the fact that MongoDB’s results didn’t fare as badly as Elastic (ESTC). But beyond that, I can’t make sense of the market’s after-hours reaction.

MDB Stock Valuation – 100x Forward Non-GAAP Operating Income

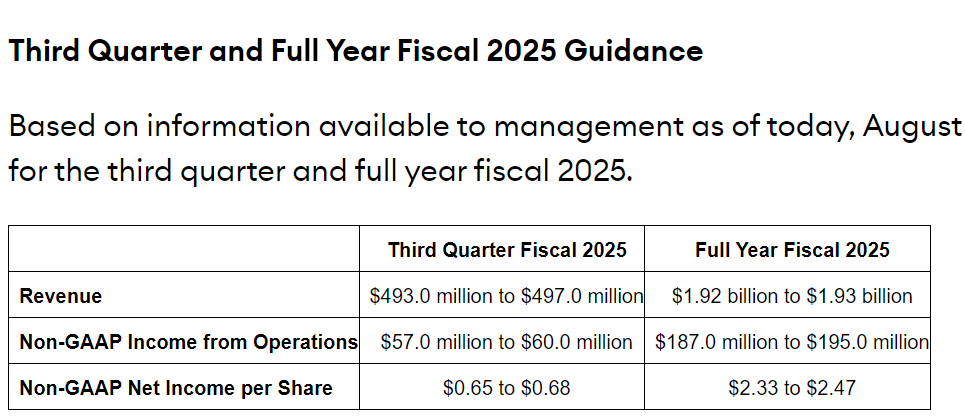

Mongo’s updated guidance reassures investors that it has what it takes to get to $200 million of non-GAAP operating income in the coming year. This leaves the stock priced at 100x forward non-GAAP EPS.

Yes, MongoDB holds approximately $1.1 billion of net cash, adjusted for its convertible notes, but is this enough to support its valuation? This implies that 5% of its market cap (including the after-hours jump) is made up of net cash. That’s clearly supportive of the overall bull thesis, but is it enough cash to support its valuation?

I can’t see how paying 100x forward non-GAAP profits leaves investors with any space to maneuver. I follow a lot of tech companies, with all sorts of growth profits and valuations, but at 100x forward profits for a business that is decidedly growing at less than 25% CAGR? No, thank you, not for me.

The Bottom Line

Paying 100x forward non-GAAP EPS for MongoDB is simply too high a premium, especially given the company’s slower growth trajectory and the uncertain path to profitability.

While I recognize the market’s enthusiasm for MDB, the fundamentals do not justify such an elevated valuation.

When a company like MongoDB is priced at this level without delivering consistent, premium growth, it leaves investors with no margin of error.

I believe it’s prudent to remain on the sidelines rather than dive into such an overvalued stock. In this case, it’s better to let this one stay in the database.

{kind=link}