AlpamayoPhoto

Hooker Furnishings Corporation (NASDAQ:HOFT) is a manufacturer and importer of residential household and contract furniture for sale that we have covered often over the years. The company has struggled over the last few quarters with the housing market slowdown and from softer demand, in large part due to higher rates for consumers to borrow money or utilize their credit. To combat demand issues and help preserve profitability, the company has made strategic moves to offload lower margin businesses, specifically by selling off the Accentrics Home product line a while back. This is a company with a rich history, and has been in operation for nearly a century. The stock has not done much for investors, though, and has swung back and forth, making it a target for traders.

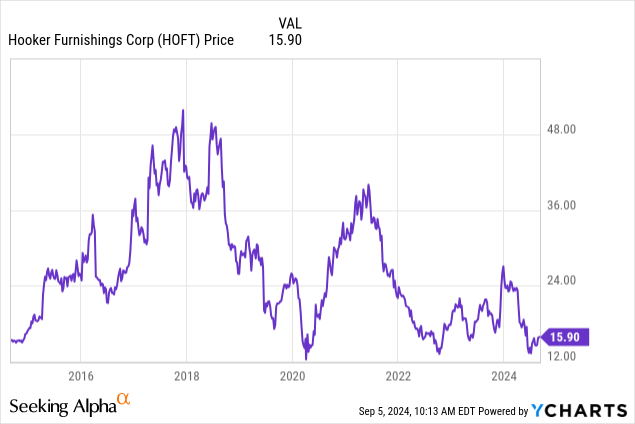

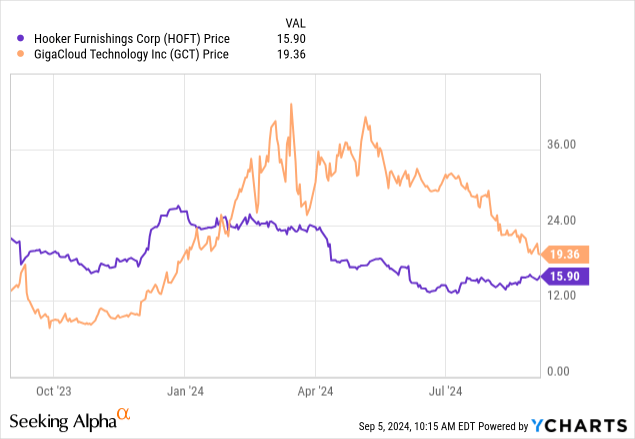

As you can see, the stock has basically gone nowhere for a decade, although the stock does offer a growing dividend, which has helped total returns. But in the last year, it is still a trader’s stock. A lot of furniture related names have been crushed during this time, including popular names like B2B focused GigaCloud Technology (GCT).

The question is, with today’s bounce due to the earnings release, can the stock regain momentum? This comes with what was a bad quarter in terms of the headline numbers. But stocks bottom on bad news, generally speaking, not good news. And this was a poor quarter overall. At $15, we think the stock is a buy here and lower. As rate cuts are about to begin, we think this will be a jolt for the housing market as well as consumer spending on furniture items. Let’s discuss the quarter.

Net sales for the just reported fiscal Q2, which is seasonally the slowest periods, dropped $2.7 million, or 2.8%, compared to a year ago. The total revenue was $95.1 million and missed estimates by $4.2 million. This was both from ongoing soft demand for home furnishings and persistent weak market conditions. But there were some positives when we look at the segments.

The Home Meridian segment’s sales increased by $1.6 million, or 5.6% versus the prior year period, primarily driven by strong performance in its hospitality division. This is actually the first year-over-year quarterly sales increase for the segment in two years. Additionally, sales through major furniture chains and mass merchants increased during the quarter. The quarter-end backlog was 2.1% higher than the same period last year and 22% higher than the fiscal 2024 year-end in January. This is positive. Further, Home Meridian reported an increase in gross profit, with a strong gross margin of 19.5%, one of the highest levels since the acquisition of the business in 2016. The quarterly operating loss was below $1 million, improving from a $3.4 million loss in the first quarter and $3.3 million loss a year ago.

The Hooker Branded segment revenues decreased by $1.6 million, or 4.5%, versus the prior year period. This was mostly due to lower average selling prices following price reductions implemented in the second half of the previous year, driven by reduced ocean freight costs. One positive was that unit volume was up 11.6% versus last year and also improved sequentially compared to the fiscal first quarter. It is also worth noting that the order backlog remained 20% higher than pre-pandemic levels at the end of the fiscal 2020-second quarter.

We saw some weakness in Domestic Upholstery. This segment saw sales decrease by $2.3 million, or 7.6% versus last year. This stemmed from lower unit volume at Bradington-Young and HF Custom brands. However, Sunset West and Shenandoah brands each reported single-digit sales increases. Sunset West’s sales increase during the quarter followed a 20% increase in revenues last quarter. Management sees Sunset West as a key driver for future sales.

With sales falling, and mixed margins, earnings were negative. However, despite the losses here, both operating and net losses improved compared to the first quarter’s losses of $5.2 million and $4.1 million, respectively. The total operating loss was $3.1 million, with an operating margin of -3.3%. The net loss for the quarter was $2.0 million, or a loss of $0.19 per share. This was a considerable miss by $0.20, however.

Now, despite the negative quarter on the surface, the market thinks brighter days lie ahead, and so do we. CEO Jeremy Hoff noted that:

“ Challenges in the macroeconomic and furniture retail environment have extended well beyond our expectations… he combination of high interest rates, a housing shortage and elevated home prices have created a sustained housing downturn for over two years…While retail sales are doing well overall, most furniture retail is not. In response, we continue to focus on the things we can control to ensure we’re in the best possible position to grow when the macroenvironment improves. In our cost reduction measures announced last quarter, we are focused on reducing non-strategic costs while continuing to invest in revenue and profit-generating initiatives”

There is a cold truth that furniture demand has just stalled out, but better days are ahead. The company expects to realize 10% savings in fixed costs beginning in the second half of this fiscal year, for a total of a $10 million reduction. Approximately $5 million in savings is expected to come by the end of the fiscal year, split between the third and fourth quarters. Reductions will come from the consolidation of certain operations and fixed cost reductions. There will be job severances as well. Inventory levels decreased by $4.7 million from year-end. This level of inventory is seemingly much more in line with consumer demand, which means the company can be less promotional and thus start to expand gross margins on sales once again.

As we look ahead, the company’s cash and equivalents were $42 million, an increase of $1.2 million from the sequential quarter. Inventory levels are down, of course. The company also has an aggregate of $28.3 million available under its existing revolver at quarter-end. Long-term debt has been knocked down., As we move forward, we think rate cuts will be the much-needed relief that this company needs, and we think it is a buy ahead of this. Risks center on competition, and persistently high rates keeping the housing market cool, and possible recession. However, we think that with cost savings put in place and effective inventory management, the company emerges stronger. This is why we think the market has bid the stock up slightly despite a bad headline print. We rate shares a buy at $15.

{kind=link}