DNY59/E+ via Getty Images

Investment Thesis

Byrna Technologies (NASDAQ:BYRN) is an interesting opportunity. I will not invest in this business or any similar business, but I do believe that less-lethal weapons could be one part of the solution against gun violence.

Moving on, the setup is very interesting. Byrna yesterday provided investors with strong preliminary fiscal Q3 2024 earnings results. This is a debt-free business that is highly profitable. It had come up against what seemed for a while an unpassable challenge when it had been banned from social media platforms.

But it has now found a way through its celebrity endorsement campaigns.

I estimate that BYRN is priced at 34x forward free cash flow. That may seem rich, but then you see that the business is growing at triple digits, and suddenly, this looks rather interesting.

Byrna Technologies’ Near-Term Prospects

Byrna is a company that has experienced substantial growth in recent years, particularly evident in its fiscal third quarter of 2024, where it reported a 194% increase in revenue compared to the same period in 2023. This growth was driven by a combination of direct-to-consumer sales and robust performance in dealer and distributor channels. The company’s marketing strategy, notably its celebrity endorsement campaign, has been a key factor in this success. Byrna’s production capacity has also expanded significantly, with the company manufacturing 55,000 Byrna SD and Byrna LE launchers during this quarter, aligning with its plans to increase monthly production.

In terms of its near-term prospects, Byrna appears well-positioned to continue its upward trajectory. The company has demonstrated a deep understanding of its marketing dynamics, fine-tuning its celebrity endorsement strategy to maximize returns. With plans to increase its advertising spend by 50% in 2025, alongside an expansion into new channels such as billboards and television, Byrna is poised for continued brand growth. Additionally, as the market for less-lethal weapons becomes more normalized and Byrna’s public recognition grows, its potential for scalability and sustained revenue increases looks promising.

Given this context, let’s now discuss its fundamentals.

Revenue Growth Rates Set A Light

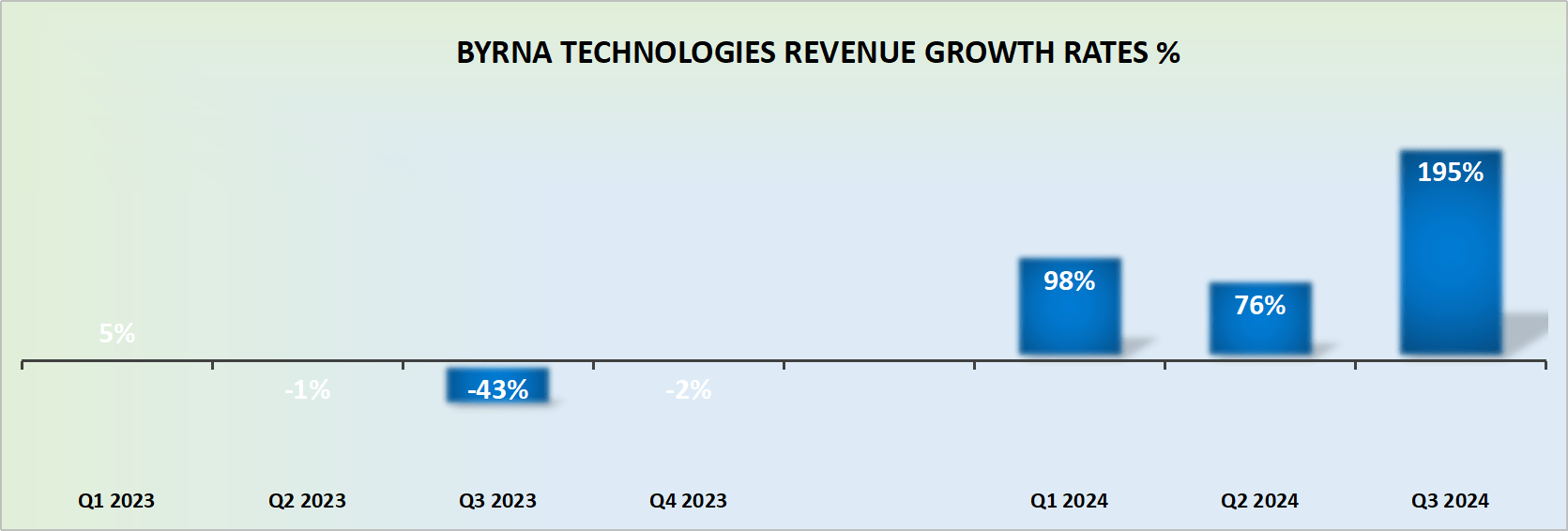

BYRN revenue growth rates

Allow me to be blunt. Byrna’s growth rates for fiscal Q3 2024 years were always going to be strong. After all, given that last year’s revenues were down 43% y/y, the comparables here couldn’t possibly be easier.

That being said, I don’t believe that many investors truly expected to see close to $21 million in fiscal Q3, 2024. That’s just off the charts. What a turnaround for a company that this time last year was delivering negative revenue growth rates.

The secret sauce for this turn around? A celebrity endorsement campaign that improved, it’s dramatically improved its direct-to-consumer business.

Now, in a similar blunt vein, some common sense is needed here. Celebrity endorsements are not a scalable driver. Or better put, it will work up to a certain extent, but at some point, you end up with lower returns on your marketing spend.

But does this consideration matter right now? No, I don’t believe it does, since for now, the valuation is compelling enough.

BYRN Stock Valuation — 34x Forward Free Cash Flow

As an inflection investor, it’s mighty important to think about a company’s balance sheet. A company with a solid balance sheet is able to get a higher multiple on its stock. And a business with no debt gets an even higher multiple on its stock.

We don’t have BYRN’s fiscal Q3, 2024 results yet, so I have had to make some rough estimates. I believe that since BYRN ended fiscal Q2 2024 with $24.8 million of cash and cash equivalents, plus the fact that it probably made at least $1.2 million of free cash flow in fiscal Q3, the business now holds about $26.0 million of cash and no debt. This means that approximately 10% of its market cap is made up of cash. That’s a very attractive position for a business that is unquestionably growing at a rapid rate.

On top of that, I estimate that going forward over the next twelve months, BYRN could make around $10 million of clean free cash flow.

Here’s my maths. We know that in fiscal Q2 2024 from $7 million of revenues, BYRN made roughly $1.1 million. And we also know that its revenues have now jumped to nearly $21 million. This means that in all likelihood its gross profit margins have improved once again to around 63%, and that its operating profits increased to around $11 million. This means that its underlying profits would be around $2.2 million, with perhaps around $400K for capex.

In sum, I very roughly estimate that BYRN’s free cash flows will be around $1.8 million in fiscal Q3, 2024. And if we add some growth to this figure, I believe that around $10 million of free cash flow sounds reasonable.

This means that investor being asked to pay around 34x forward free cash flow for a business that is growing at triple digits. This strikes me as an attractive risk-reward opportunity.

Risk Factors To Consider

The first and most obvious risk aspect is that this is a small-cap business. Small caps are incredibly volatile. Particularly, those below $20 billion market caps, without broad institutional sponsorship.

Secondly, Byrna faces brand-related risks that could affect its ability to maintain its growth. The strength of its brand is crucial to its marketing strategy, which includes investments in celebrity endorsements and social media campaigns. How scalable is this overall strategy? At some point, the company will get lower returns on its celebrity endorsement campaigns, and that will lower its revenue growth rates.

Additionally, Byrna competes in a growing market for personal security devices and faces ample competition, too.

The Bottom Line

In conclusion, Byrna Technologies presents an intriguing investment opportunity, combining a debt-free balance sheet with triple-digit revenue growth fueled by its successful celebrity endorsement campaigns.

While there are risks related to the scalability of its marketing strategy and increasing competition in the personal security device market, the company’s strong financials and strategic initiatives position it favorably.

For investors seeking a compelling risk-reward profile in a rapidly expanding industry, Byrna might just be a shot worth taking.

{kind=link}