Michael M. Santiago/Getty Images News

It’s a dire situation

The S&P 500 (SP500) is facing the recessionary bear market with the tech bubble burst, and on top of that, there is a potential housing bubble burst. It’s really a combination of the 2001 and the 2008 bear markets, and in both cases the S&P 500 fell by over 50%. Thus, in the current situation, the S&P 500 is likely to fall by at least 50% as well.

However, based on the current data, the economy is not in a recession yet, and the recession could be delayed by another quarter or two. However, the market is expecting that the Fed will start with an aggressive monetary policy easing cycle.

In my opinion, the institutional investors inflated the GenAI bubble, and now need to sell – because the GenAI hype is fading, and the bubble burst is unfolding.

Thus, they need the Fed to start cutting interest rates to delay the GenAI bubble burst, so they have more time to sell. They need the Fed to cut by 50bpt in September.

After the weak July labor market report, which pushed the unemployment rate to 4.3%, the Wall Street used the opportunity to start lobbing for not only a 50bpt cut in September, but also for the emergency cut. Even the respected university professor Jeremy Siegel urged the emergency cut.

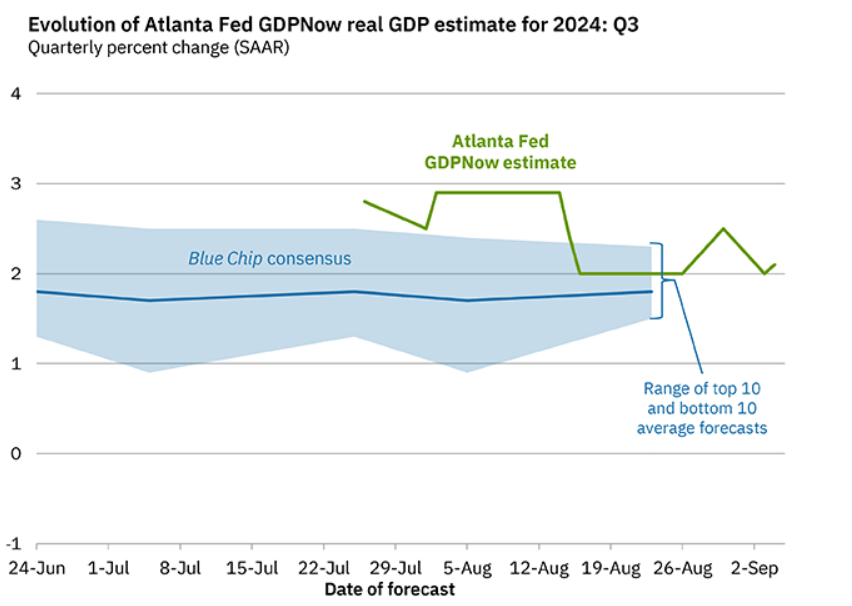

Q3 GDP at around 2%

First, we are currently not in a recession, as the GDPNow predicts that Q2 GDP will be around 2.1%, led by very strong consumption at 2.1%. Thus, the Fed cannot come to the September meeting and say that the US economy is weak and in need of stimulus. The US economy is currently still solid.

Atlanta Fed

The labor market, still near full employment.

Next, let’s look at the August labor market report. All indicators that I pointed out to focus on came out strong:

- The labor force increased by 120K, and given that the labor participation rate stayed unchanged, virtually all growth in the labor force is due to immigration. The labor force growth due to immigration is positive for growth, and ultimately inflationary.

- The number of employed people increased by 168K, and the number of unemployed people decreased by 48K, which means that each entrant in the labor force found a job, plus, some unemployed persons found a job as well.

- Thus, the unemployment rate decreased to 4.2% which is still historically low, and near full employment.

- Further, the establishment survey shows that construction added 34K jobs, and the leisure and entertainment sector added 46K jobs – that’s where the immigrant labor force is getting hired, and together with healthcare jobs, this represents over 90% of total new jobs created in August.

- The wage growth accelerated to 0.4% MoM, suggesting that the demand for labor is still very strong.

So, take it altogether, the August labor report does not show an imminent recession, and does not warrant the Fed’s intervention. This is supported by the leading job market indicators, such as the weekly claims, which suggest that the September labor report will be sufficiently strong as well.

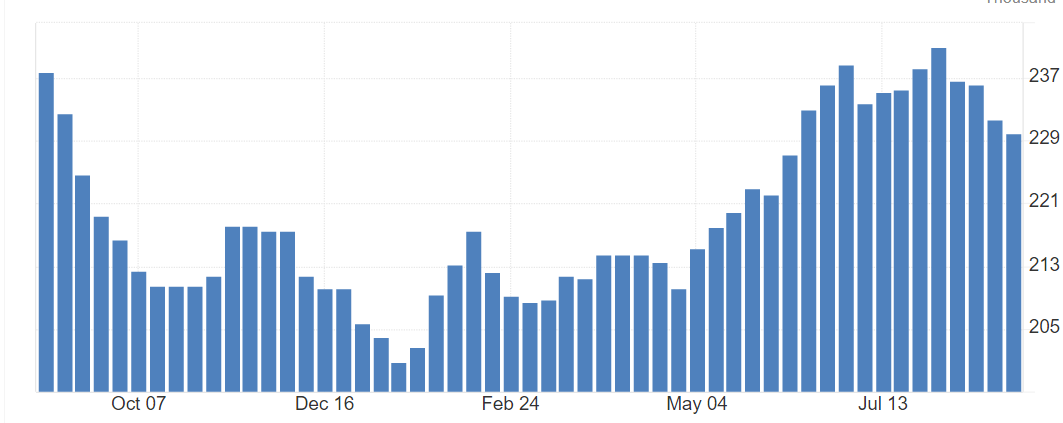

Here is the chart of the 4-week average for weekly claims, which is a leading indicator for labor market health. It has been falling for 4 weeks already, and it’s at a 12-low point. This does not indicate an imminent recession. The labor market is strengthening – it is what it is, and that the data shows.

4-week average in initial claims (Trading Economics)

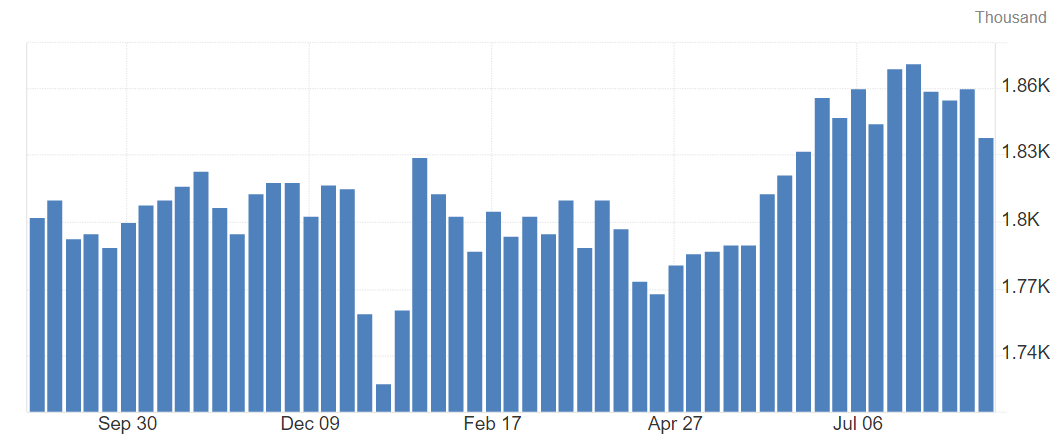

Even the continuing claims are falling, now at a 10-week low point. This means that it takes a shorter time to find a new job for people who initially filed for unemployment benefits.

Trading Economics

To have an imminent recession, which requires the Fed to cut aggressively, we need to see a spike in the initial claims and the continuing claims, and that’s not happening. Let’s wait for next Thursday for the update.

On the negative side, there are revisions to the previous months, and the pace of job creation is slowing down. Undoubtedly, we are heading towards a recession, but it might not happen until Q1, 2025.

The bursting bubble

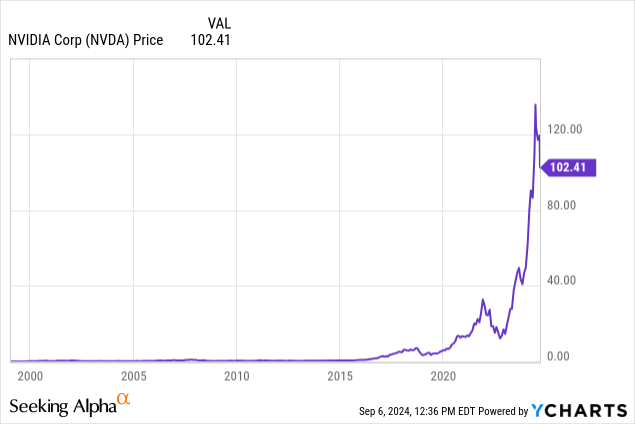

Here is the bursting bubble in early stages – this is Nvidia (NVDA) – the poster child of the GenAI bubble. Institutional investors, like BlackRock, are still overweight GenAI theme, and need to get out. Retail investors are also all-in on Nvidia, and now are possibly buying the dips.

If the recession comes and the GenAI capex disappears, Nvidia could fall by 80-90% – and Nvidia is the third-largest stock in the S&P 500 index.

Thus, the Wall Street desperately needs the Fed to cut, to possibly delay the recession or preferably to cancel the recession altogether.

The problem is that the unemployment rate is still near the full-employment level, so if the Fed cuts aggressively to prevent the recession, the unemployment rate could drop below the 4% level by year-end, and continue falling. Thus, the wage growth could accelerate and restart the second wave of inflation – the Fed would be forced to start hiking again next year.

This is an especially serious situation given the geopolitical escalation, and the possibility that oil spikes. In fact, given the unfolding deglobalization, we are in stagflationary environment.

The point is that the Fed needs the recession and the unemployment rate to increase at least over 5%, so when the growth cycle restarts, there is at least some slack in the labor force.

Implications

The market is forcing the Fed to cut prematurely to delay the GenAI bubble burst. Irrespective of what the Fed does, the GenAI hype is fading, and the GenAI bubble burst is unfolding. This is the primary negative variable for the S&P 500 (SPY) at the moment.

However, if the Fed does cut and cut by 50bpt in September, without the evidence of a recession, we could have another short-term spike in the stock market.

At the same time, the stock market is forward-looking, and if the recession is expected to start in Q1 2025, the market will fall in advance, before the labor market confirms a recession. However, the Fed needs to reference at least some indicators of an imminent recession to cut aggressively. Thus, the Fed is likely to disappoint the market, which will likely accelerate the GenAI bubble burst, and cause further selloff in the S&P 500.

{kind=link}