Jetta Productions Inc/DigitalVision via Getty Images

Introduction

Samsara (NYSE:IOT) recently reported their results for Q2 FY2025. These results beat on both the top and the bottom line and have sent shares skyrocketing in the trading sessions since the release. I recently initiated coverage on this stock when it was trading at $38.37 and rated it a STRONG BUY, which has proven to be an excellent call. Shares rocketed up 13.6% this past Friday, its largest single-day increase YTD.

I believe investor enthusiasm is warranted, given the future growth prospects and lack of strong competition within their industry. However, this recent surge in price has elevated shares to extremely high valuation multiples, which I believe may be unsustainable. IOT has a 5-year beta of 1.50, meaning shares tend to be 1.5x as volatile as the broader market. Given this high volatility, combined with an expensive price, I am downgrading IOT to a hold with the caveat that I will likely encourage buying if there is a pullback in the future.

Q2 Earnings:

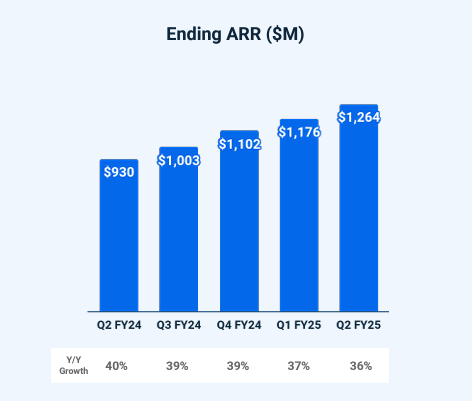

Samsara reported $1.264bn in Q2 FY25, annual recurring revenue (ARR). This figure is up 36% YoY and ~7.5% sequentially. This implies that they are consistently able to bring on new customers or renew existing customers at higher contract values. The average ARR per $100k+ ARR customer has also risen 3.9% YoY from $306k in Q2 FY24 to $318k in the most recent quarter. This growth is not all that significant, as it barely outpaces the inflation we have experienced over the past year. This proves that the emphasis for Samsara is still on acquiring new customers rather than raising contract values. This was evidenced as their CEO, Sanjit Biswas, essentially glossed over a question on their earnings call about better pricing power stemming from new product releases. I will be closely monitoring this figure, as it is essential that this number grow significantly in the future if IOT is going to grow into its valuation (more on this later).

Investor Relations

Samsara’s ARR mix is improving every year, from my perspective. Their largest segment ($100k+ customers) has grown 8% YoY and 17.3% since Q2 FY23. These high-value customers can significantly reduce IOTs G&A expenses due to the fact that managing fewer contracts is easier. Signing fewer contracts to reach a target level of ARR means fewer resources are expended on legal and administrative processes as well. Additionally, having a smaller number of customers can lead to economies of scale since IOT can specialize their operations to focus on providing excellent service to a smaller subset of companies.

This past quarter, IOT recorded a record 2,133 customers who generated more than $100k in ARR. This figure is up an incredibly impressive 41% YoY and 8.6% QoQ. They also added a “quarterly record of 14 customers with more than $1 million in ARR.” This is by far the most important segment to grow as the operating efficiencies associated with large contract customers is what will, in my opinion, allow this firm to begin posting large quarterly profits sooner rather than later.

They also reported a dollar-based net retention rate of 120% for large customers, which demonstrates that they are able to entice existing customers into purchasing new products or signing contracts at higher values.

Operating expenses continue to be a massive drag on Samsara’s operations; however, we are seeing massive improvements. Their non-GAAP gross margin remained steady QoQ at 77% however their non-GAAP operating margin was 6%. This is a 900bps improvement YoY and a 400bps improvement sequentially, which was a reassuring sign for investors.

They also raised their midpoint of FY25 revenue guidance from $1.209bn in Q1 to $1.226bn (1.4% increase). The more significant increase, from a profitability standpoint and as a percentage increase, was their midpoint EPS guidance. This jumped from a midpoint of $0.14/share to $0.17/share (21.4% increase QoQ).

Catalysts

Adoption of new products is integral for a company like Samsara that operates in an extremely competitive landscape and is dependent upon customers renewing contracts. A lack of innovation can lead to customers jumping ship when it comes time to renew their contracts in favor of a competitor that offers more advanced features or a better value proposition.

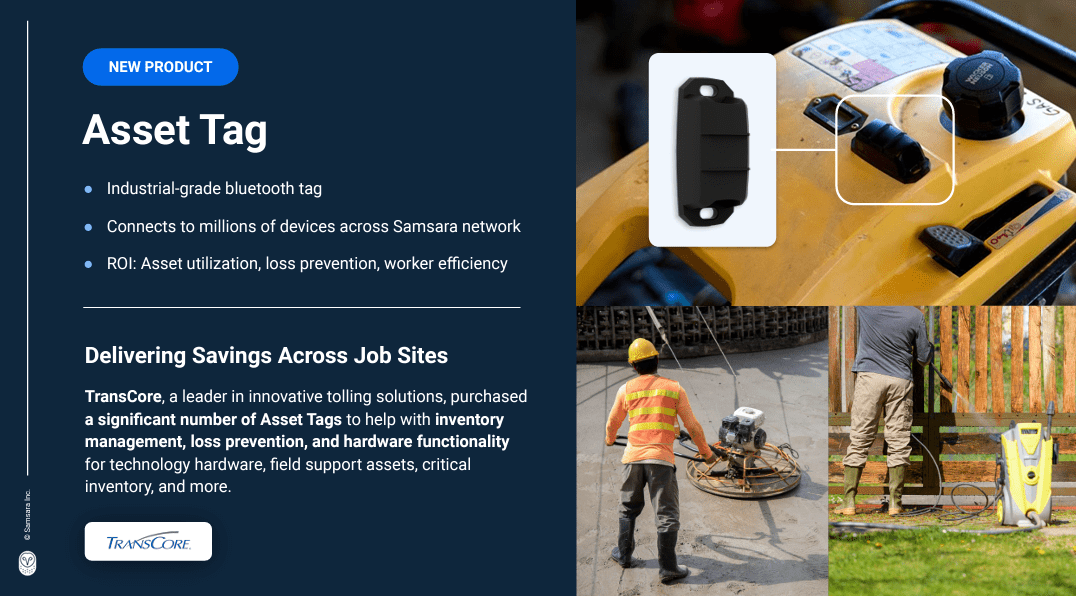

One of the new products highlighted in their investor presentation was the industrial-grade Bluetooth Asset Tag, which I also discussed in my previous article on IOT. I won’t go into too much detail about the use-cases of this product here. However, one notable section in their investor presentation discussed how one of their largest enterprise customers, TransCore, has “purchased a significant number of asset tags” to help them keep track of “technology hardware, field support assets, critical inventory, and more.” Additionally, IOT reports that this product contributed ~$1mn of net new annual contract value (ACV) during Q2. While this only makes up ~.33% of quarterly revenue, it is a sign that enterprise customers are beginning to implement this product.

Investor Relations

New launches are something that I am constantly monitoring when it comes to this firm in particular as deployment of useful, cost-saving products is essential for the growth story of IOT. Another useful statistic from their earnings calls was that 94% of $100k+ ARR customers use 2 or more of their product offerings. The more integrated a customer becomes with various Samsara software and hardware offerings the higher the switching cost becomes, and in turn the less likely they are to switch to a competitor.

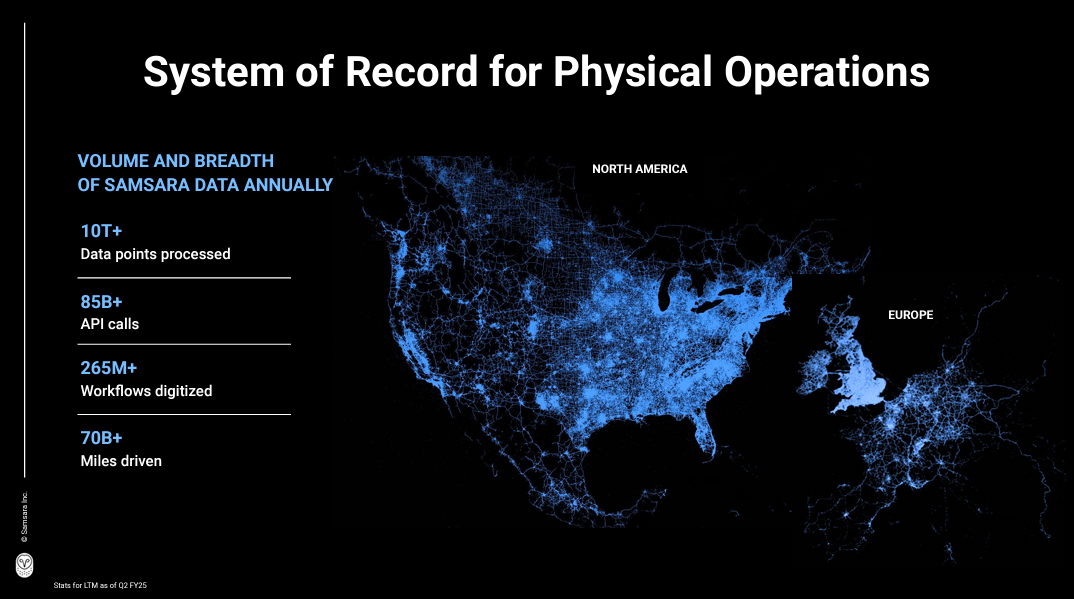

Another potential lever for future growth is the vast quantity of data that IOT collects on an annual basis. They reported that, for the LTM of operations, they collected over 10 trillion data points and that there were over 85bn application programming interface (API) calls. This refers to the number of requests made to Samsara’s internal API, which is a proxy for customer usage of their software solutions. This figure also demonstrates their ability to scale their operations if they are able to handle this level of customer usage.

Investor Relations

This data can be used either to offer more efficient solutions for customers (for example, their ability to optimize route’s for truck drivers is largely dependent on the quantity and quality of their data). Additionally, data is one of the world’s most valuable resources.

This is evidenced by many recent transactions, including Reddit’s (RDDT) contract with Alphabet Inc. (GOOG, GOOGL) for over $60mn per year. This contract gives Alphabet exclusive access to Reddit’s data in order to train advanced generative AI models. I could envision a similar scenario where a large tech-focused AI firm with lots of equity capital could sign a deal with IOT to purchase the data they collect on enterprise customers.

As more firms begin to enter the race to provide autonomous vehicle solutions, the treasure trove of data Samsara possesses could become recognized as an incredibly valuable asset. This is also an asset that is constantly growing its value as IOT brings on more customers and collects more information from said customers. Even if they do not choose to sell their data, the information they have on their customer base is valuable internally and compounds over time allowing them to offer a more comprehensive suite of products.

One of my favorite statistics in their investor presentation was the fact that 87% of Q2 net new ACV came from enterprises that do not operate within the transportation vertical. Diversification of revenue streams is important not only from a risk standpoint, but also to ensure that IOT can continue to grow its operations. There is only a finite amount of transportation companies in the world, therefore growth into other areas is imperative to their future success.

Valuation

According to IOTs earnings call, roughly 50% of commercial fleets in North America are not using vehicle telematics solutions and only 10% of fleets are using video based safety products. These are IOTs two largest offerings, representing $500mn in ARR each, therefore having a large number of enterprises that have not adopted a solution yet is extremely bullish for IOTs future prospects.

Another bullish statistic is that physical operations (construction, transportation, retail, etc.) represent 40% of global GDP. Nearly every firm that operates within physical operations could potentially stand to benefit from at least one of Samsara’s product offerings.

Investor Relations

The estimated market size of the connected operations industry by 2026 is $200bn compared to $122bn in 2023 (18% CAGR). Connected fleet operations specifically are expected to grow at a 25% CAGR from 2023-2026, which is fantastic for IOT as they generate over $1bn in ARR from this segment of their business.

Samsara estimates that they have, so far, only penetrated roughly 5% of their total addressable market (TAM) as of late June this year. Obviously, it is an unrealistic assumption that they will be able to capture the entire market, but it does prove that there is room for massive growth moving forward.

IOT estimates that, due to 98% of their revenue coming from customer subscriptions, their lifetime value of a customer is 8x greater than the cost to acquire a customer. Their non-GAAP sales & marketing expense (which excludes SBC) was $128.7mn in Q2 FY25. In their investor presentation they did not directly report how many customers they added. However, I backed into this number by taking the sequential increase in $100k+ ARR customers and comparing this to the ARR mix (54% are $100k+ customers). Considering the ARR mix did not change materially from Q1 FY25 I estimated that they added ~313 customers in Q2. This equates to a customer acquisition cost of roughly $411k. This equates to an average estimated lifetime customer value of $3.29mn.

All of this data is useful in estimating future revenue growth rates. For instance, using management’s current guidance for FY25 revenue of $1.226bn (midpoint figure) in tandem with the 18% CAGR of the connected operations industry over the next 2 years, we arrive at an ARR figure of $1.71bn at the end of FY27. The other figures are more ambiguous, and it is hard to project with confidence how long it will take for IOT to capture more of their TAM.

In my previous article I calculated an implied share price of $43.01 which uses ~30% revenue growth over the next 5 years and has the operating margin reaching 21% in the terminal year of the DCF. I stick by the assumptions used in this model as I do not believe anything in the recent report has materially changed the value of this company, however the recent rise in share price means that shares trade ~7.2% above my estimate of fair value.

DCF Model (Author)

Using a DCF model is only one piece of the equation when it comes to estimating the value of a firm like Samsara, especially given we are discussing a young, high-growth company.

I do not mind holding investments in a firm like this when shares seem to have reached roughly their implied share price, as there is a good chance that they could outperform my own expectations given the extremely solid fundamentals of this business in particular. But, given how much shares have jumped recently, I do not believe that now is the best time to invest, which is why I rate IOT shares a HOLD.

Takeaways

Samsara is an incredible business that, I believe, will continue to grow rapidly over the coming years. While the growth story is most definitely still in-tact following their recent earnings report, I believe that shares have reached roughly full value after the recent surge in price.

I will continue to monitor this company moving forward and will also likely look to buy shares in the event of a pullback as I believe this company will reach profitability over the coming quarters and become an incredibly valuable business over the coming years.

{kind=link}