LdF/E+ via Getty Images

If you own a home, you own a highly favorable asset. Not just because it provides shelter, but because it’s a red-hot “commodity” again.

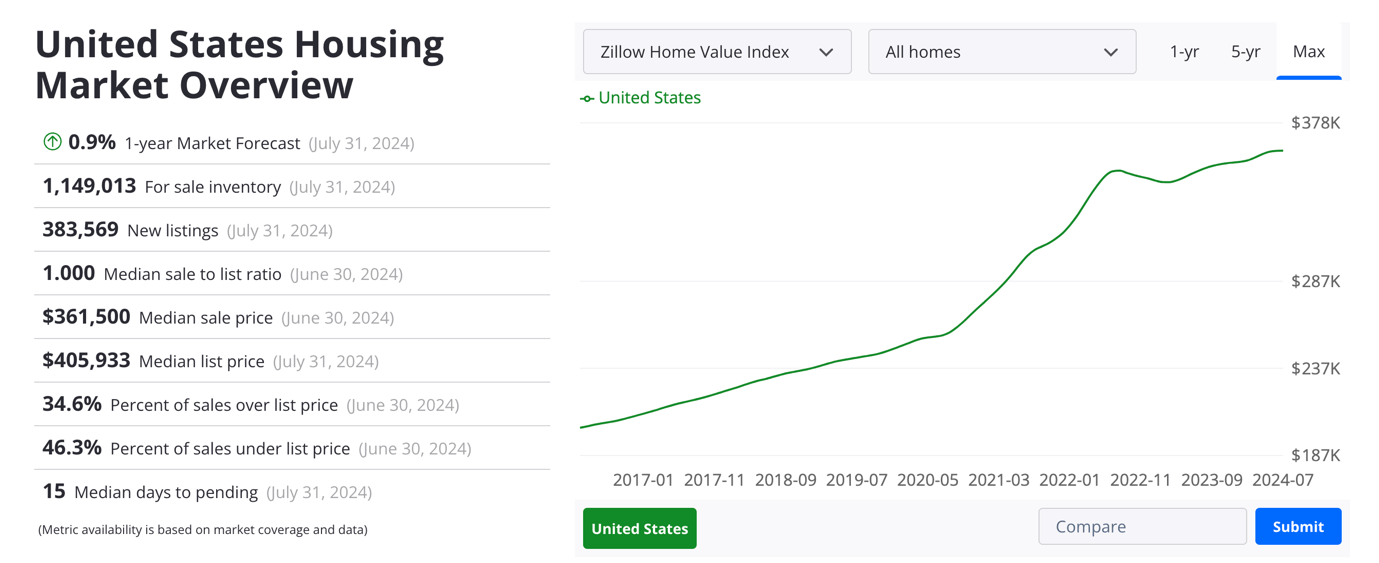

Using Zillow’s latest numbers, the average home in the United States now sells for more than $360 thousand, up from $203 thousand in April 2026. This translates to a 77% surge in roughly eight years.

Zillow

That’s not even the worst part – for people searching for a home.

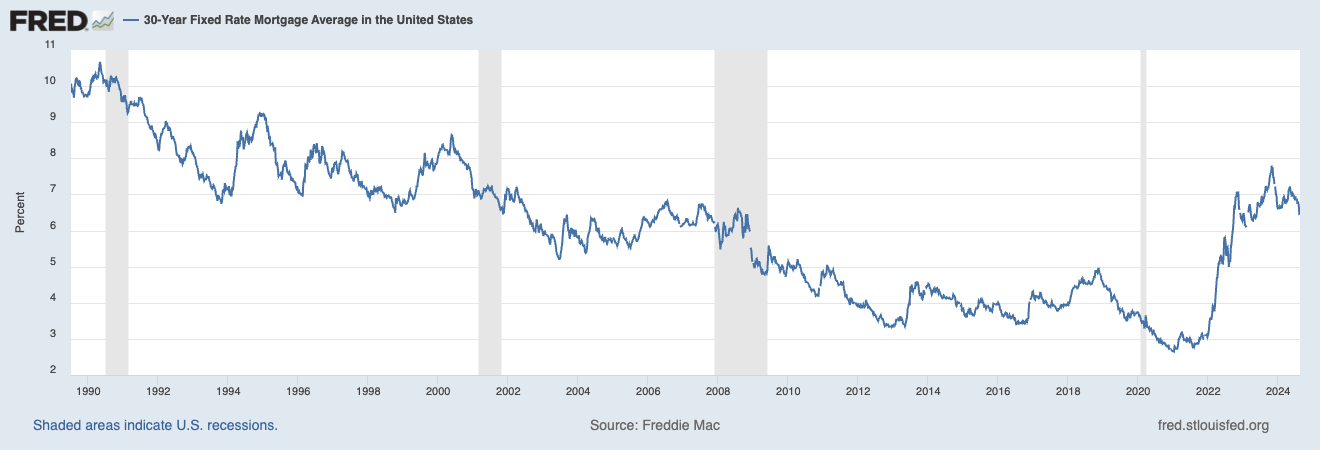

In 2016, the 30-year fixed mortgage rate was below 4.0%. Now, it’s roughly 6.5%.

Federal Reserve Bank of St. Louis

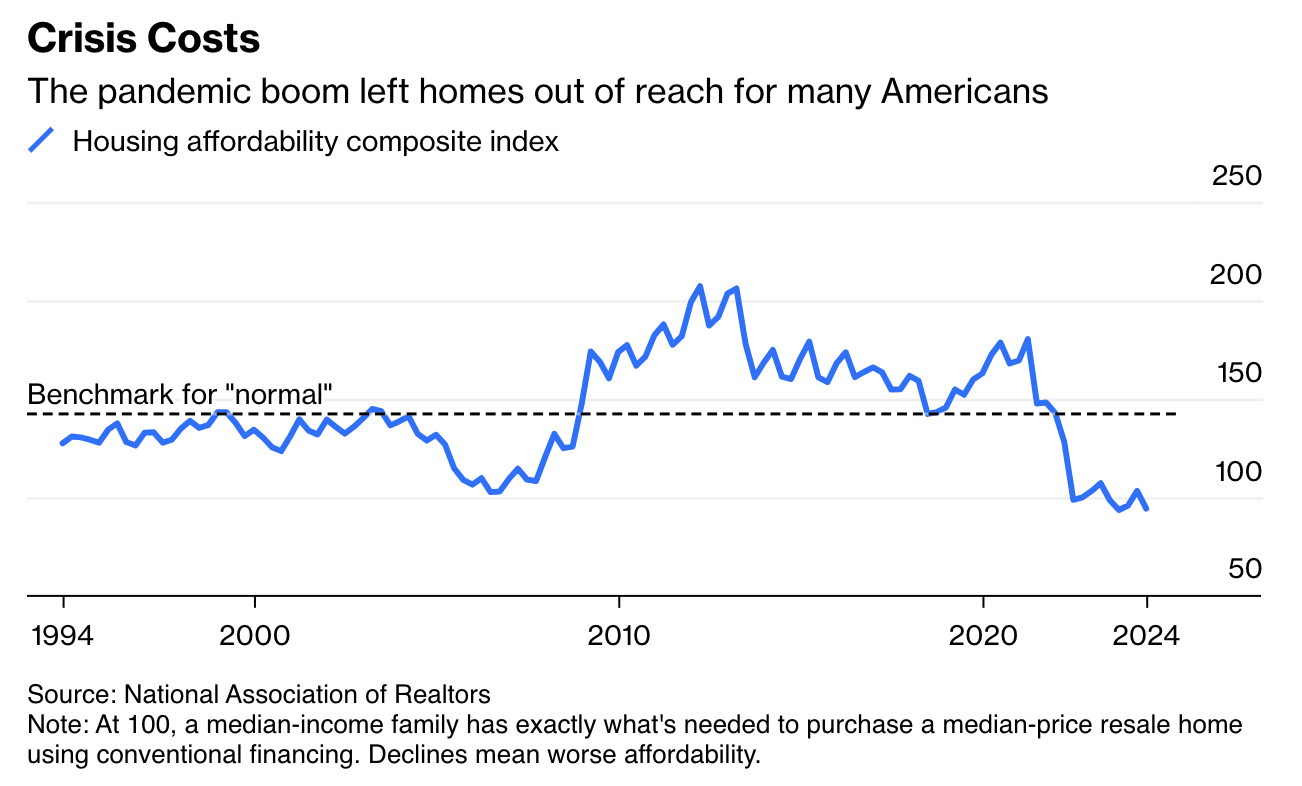

Based on this context, on August 21, Bloomberg published an article titled “Homes Will Be Affordable Again – Just Not Anytime Soon.”

The article included the chart below, which shows that affordability has never been worse since the start of the housing affordability composite index in the mid-1990s. It wasn’t even this bad before the Great Financial Crisis hit.

NAR

Although the worst seems to be behind us, as rates are not north of 7% anymore, the affordability index is still in panic mode. The average monthly payment to service a 6.5% mortgage rate is roughly 43% of the average salary of a full-time employee in the United States.

One of the solutions to this affordability problem was expected to be a housing crash, potentially triggered by the Fed hiking rates.

However, when the Fed hiked rates, homeowners who had locked in low rates did not sell their homes. This created an artificially low housing supply, achieving the opposite of what the Fed had hoped. Homes become pricier on top of higher financing rates.

Even the expected rate cuts wouldn’t change much. According to Bloomberg:

“The interest rate cuts priced into the futures markets — a fed funds rate approaching 3% by the end of 2025 — would probably only take mortgage rates down to somewhere in the 5% to 5.5% range. The 3% home-loan rates of the pandemic were a crisis response, and we should hope to never experience those conditions again.” – Bloomberg.

This is one of the reasons why Presidential candidate Kamala Harris presented a four-point plan. This includes:

- Building 3 million for sale and rental homes.

- Reducing barriers to building homes.

- Help middle-class Americans to afford homes, including providing $25 thousand in down payment assistance.

- Encourage the use of low-income housing tax credits to help low-income Americans.

Although Kamala hasn’t won yet, and it needs to be seen how inflationary these proposals are, as they mainly seem to stimulate demand, there’s a growing bipartisan support to address the housing shortage. As reported by Redfin:

“What’s promising for Harris: There’s growing bipartisan support for addressing the housing shortage, with Republicans in Florida and Utah zoning for more housing units at the same time as Democrats in California and Washington. There has also historically been strong bipartisan support for credits to first-time homebuyers (every state already provides first-time homebuyer credits). If Harris can lead Congress in pulling off her plan, she could make a meaningful dent in the affordability crisis by the end of this decade.”

Needless to say, even if Harris were to implement her plan, it would likely take too long to build these homes to make a meaningful impact. This is why Bloomberg makes the case that only strong annual wage growth in an environment of subdued home price increases would be likely to stimulate affordability over time.

“A plausible path to improved affordability over time is annual wage growth of 3.5%, home price growth of around 2% — lower than the historical average because of both increased construction and rising resale inventories — and mortgage rates at 5%. Over five years, this combination would bring housing affordability back to within 12% of those 2018 levels, with perhaps some down payment assistance from Washington closing the remaining gap.” – Bloomberg

This means the next government needs to increase supply without igniting a new wave of housing inflation.

That’s a tough task.

Hence, I’ll show you two picks that benefit from affordability issues and provide investors with both growth and income.

Invitation Homes Inc. (INVH) – 3% Yield, Safety, And Growth

Because of the mix of elevated interest rates and record home prices, renting has become attractive – at least relatively speaking.

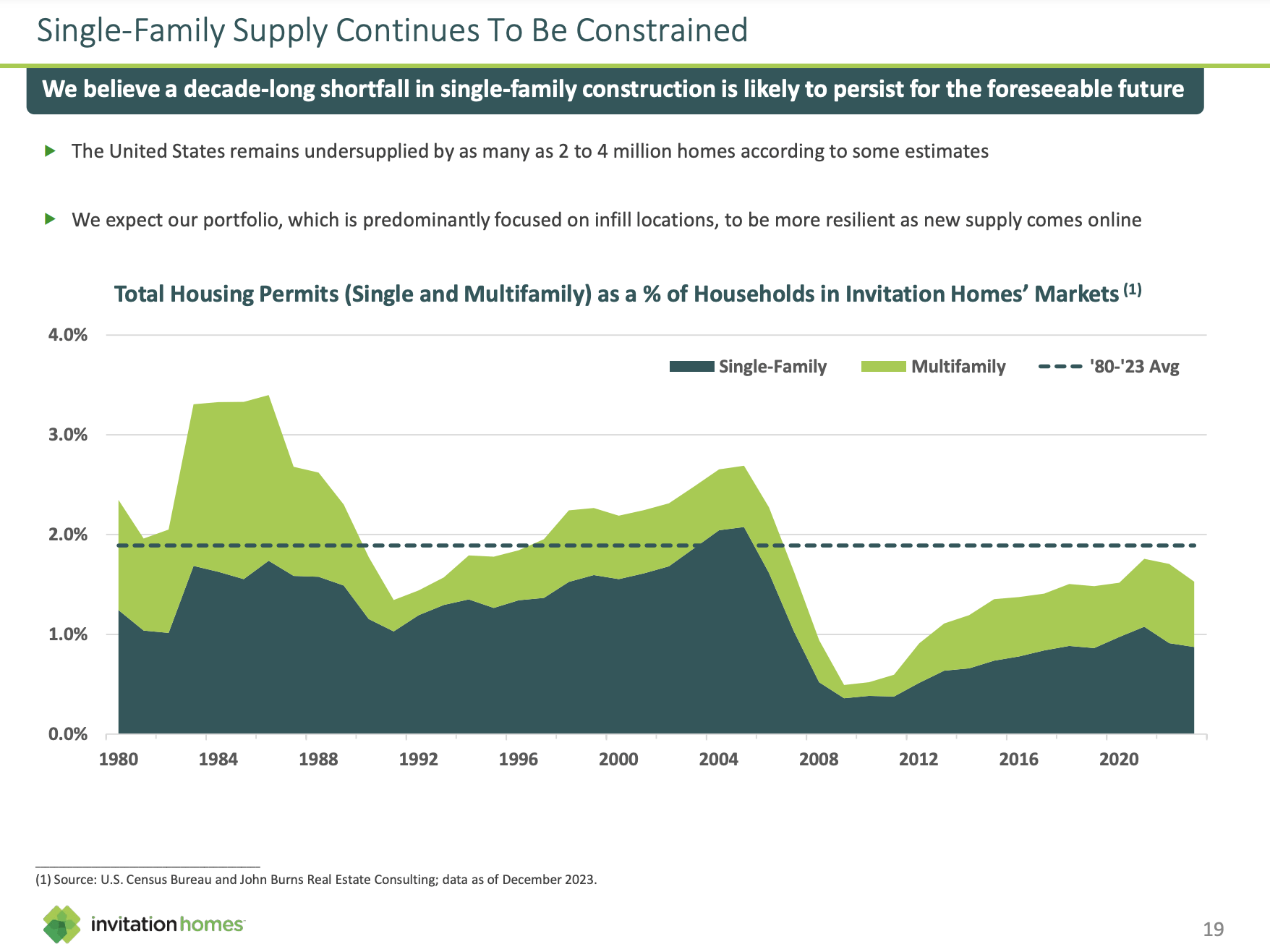

Invitation Homes makes the case that the United States has a shortage of between 2 and 4 million homes. Even better, while this supports pricing power, the company also believes that its focus on infill markets protects it in the event of rising supply, potentially caused by government initiatives.

Invitation Homes

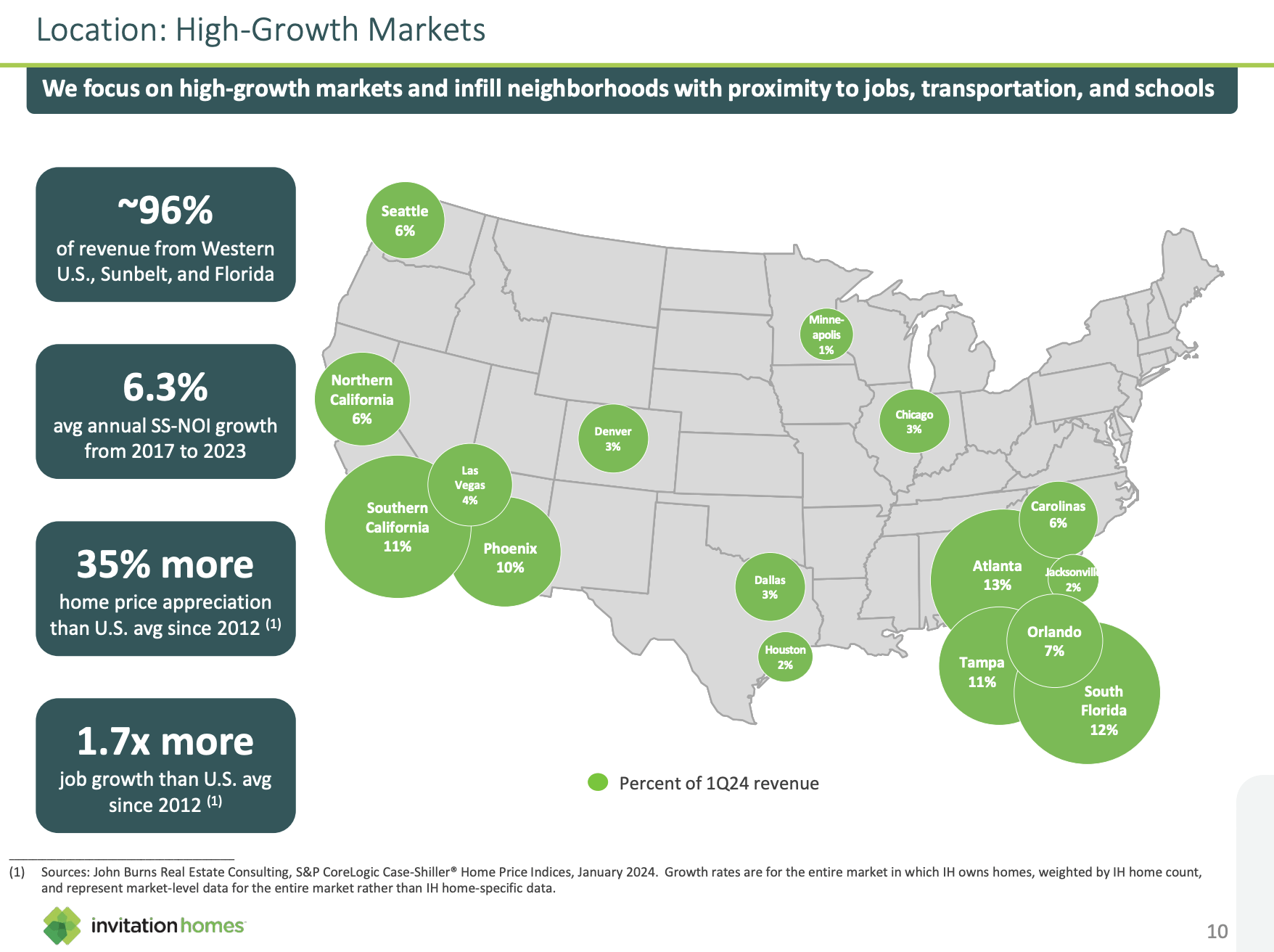

Invitation Homes is a major landlord, owning high-quality homes in attractive neighborhoods. Going into this year, it owned roughly 85 thousand homes in 16 core markets.

Almost 100% of its revenue comes from the Western U.S., Sunbelt, and Florida, with SoCal, Atlanta, and Southern Florida being its largest markets. The company focuses on attractive markets close to employment hubs and good schools.

Invitation Homes

On average, the homes cover 1,880 square feet (1.75 a), including three bedrooms and two bathrooms. This appeals to families and sets the company apart from major REITs focused on apartments and/or manufactured housing communities.

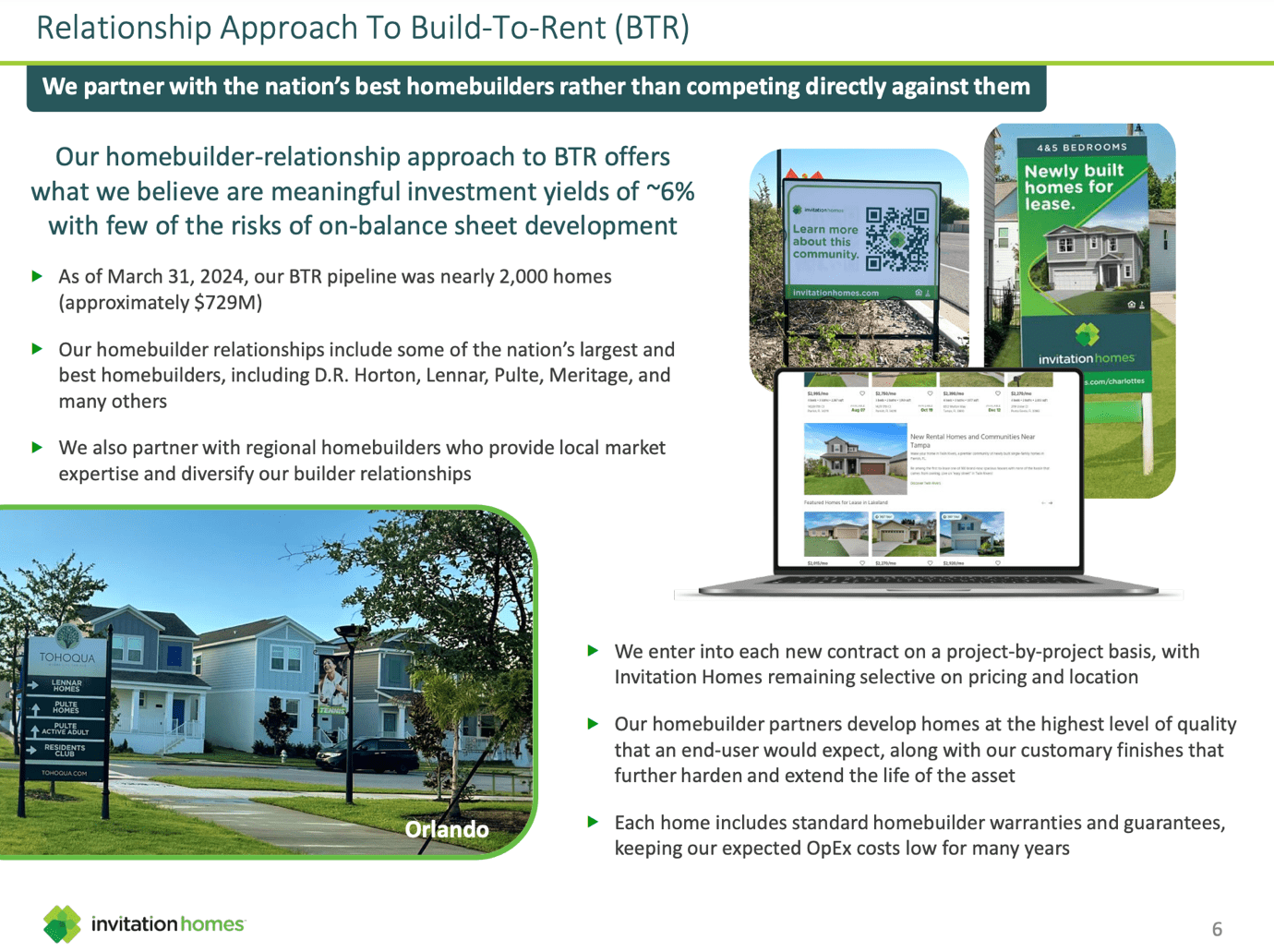

It also has relationships with builders, who build entire neighborhoods for INVH. This yields high returns and is a win-win for both the home builder and INVH.

Invitation Homes

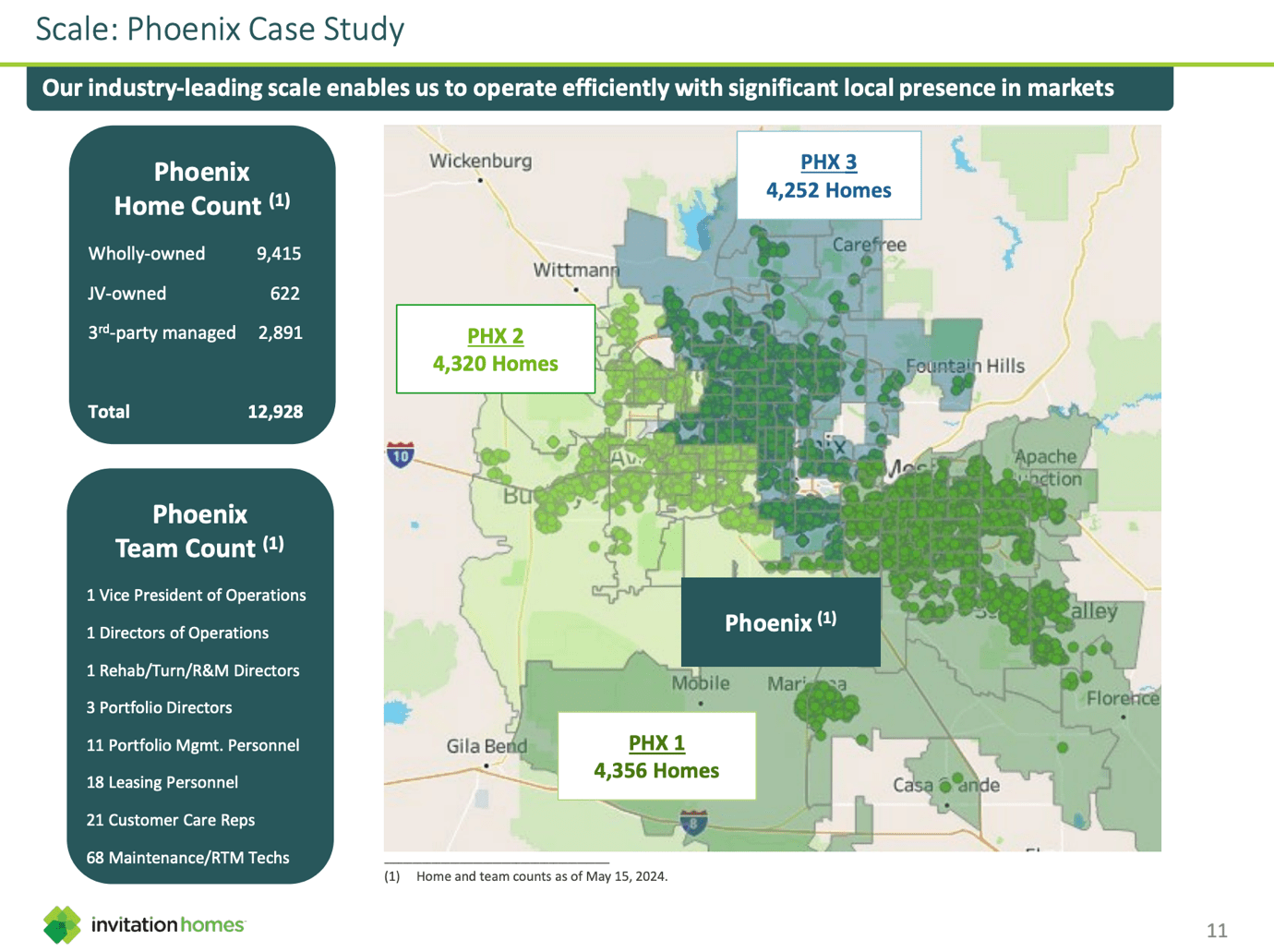

With that said, whenever companies become this large, there’s always the risk of building the Tower of Babylon, where it becomes too hard to manage. To avoid this, INVH has a smart strategy for local management. For example, in Phoenix, the company has divided the market into three areas.

These areas are managed by one Vice President of Operations, 3 Portfolio Directors, 18 Leasing personnel, and many others, including maintenance professionals.

Invitation Homes

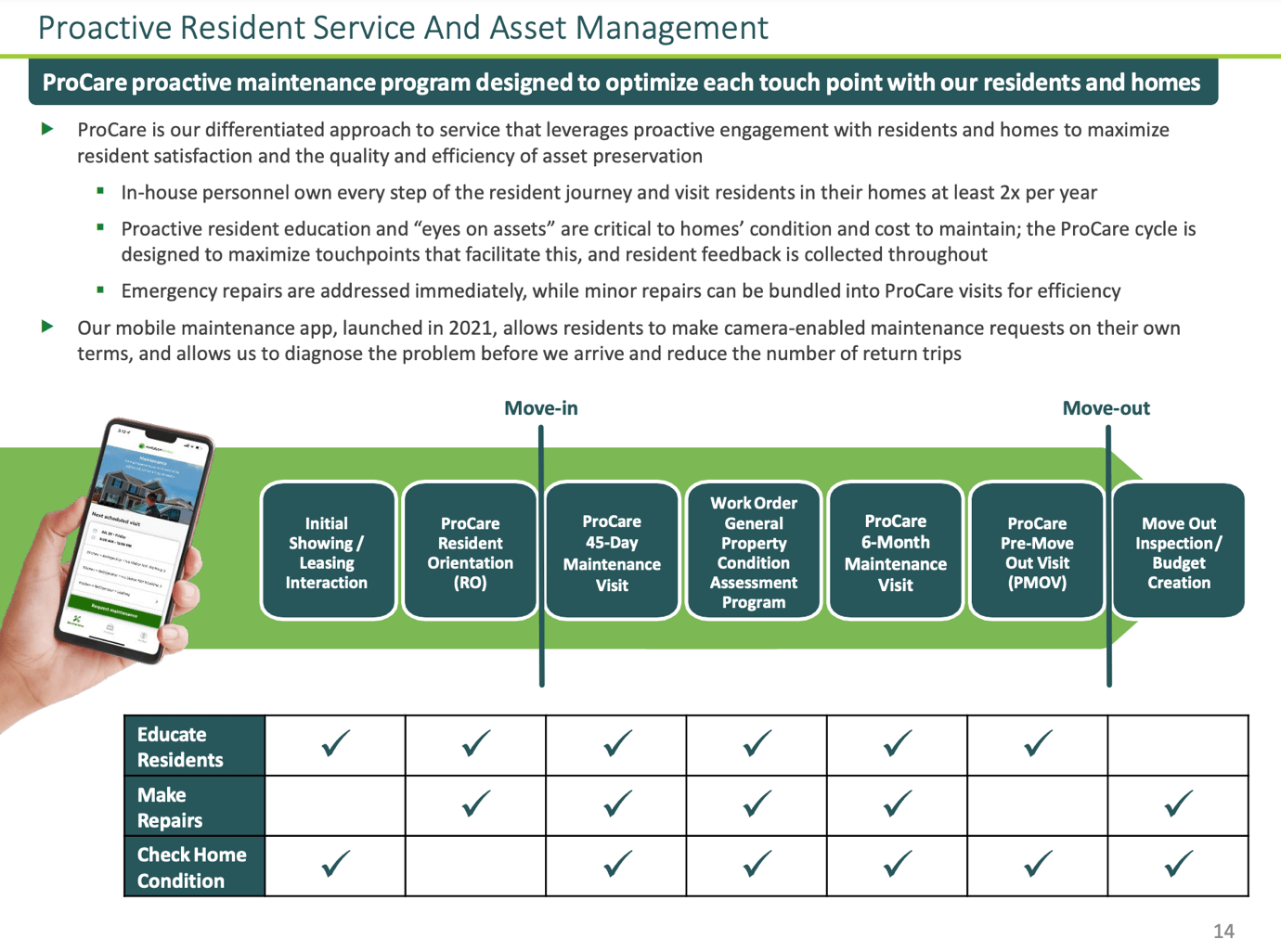

It also has something called ProCare, which helps the company to streamline operations. This includes helping tenants with questions and maintenance issues. In fact, it supports the entire process before the move-in and after the move-out.

Invitation Homes

Moreover, while other landlords are being pressured by new supply growth and inflation, INVH expects to grow its same-store NOI by at least 3.75% this year, supported by at least 4.5% growth in same-store revenues.

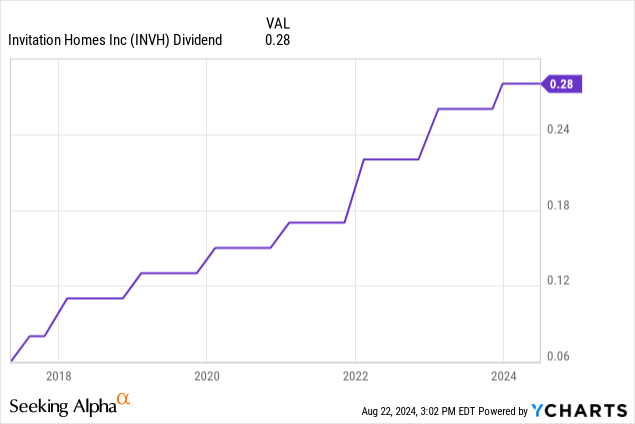

Currently yielding 3.1%, the dividend has a 61% payout ratio and a five-year CAGR of 23%.

Seeking Alpha

Regarding its financial health, the giant has a 5.3x leverage ratio, no debt maturities until 2026, 99.5% fixed-rate debt, and an investment-grade credit rating of Baa2 from Moody’s.

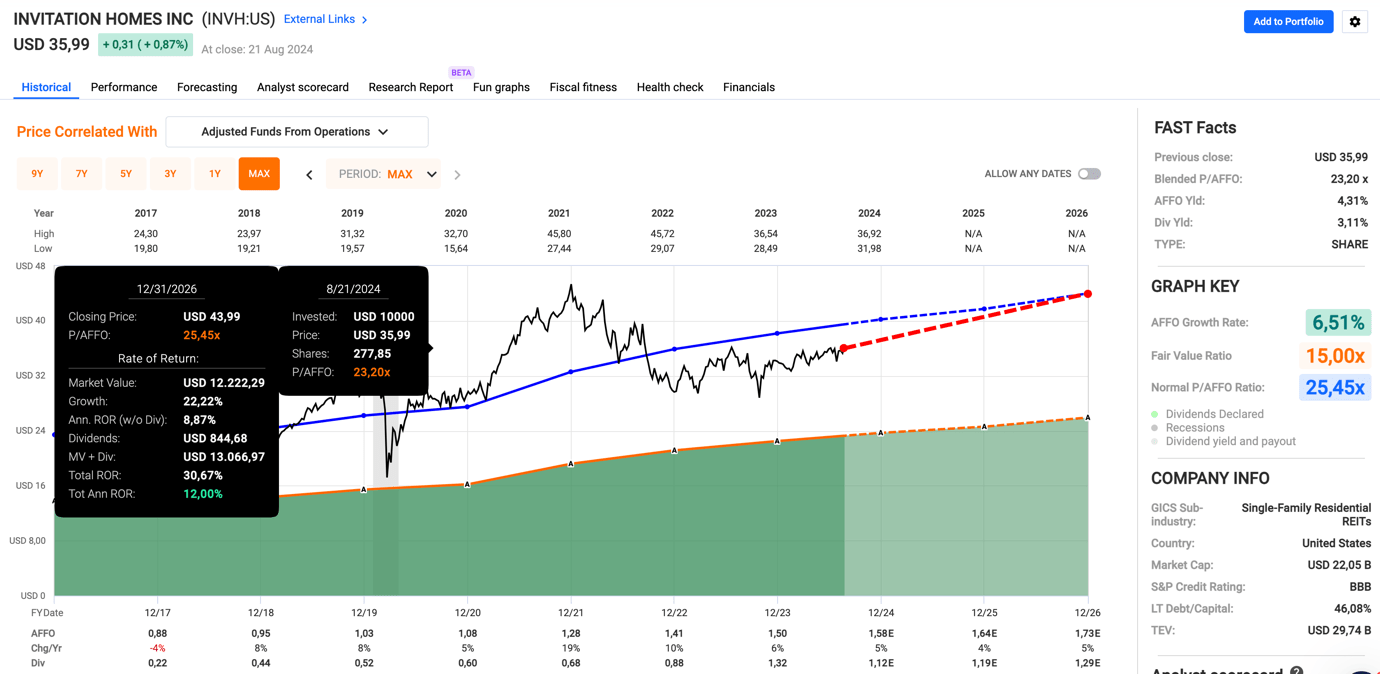

Valuation-wise, the company trades at a blended P/AFFO (adjusted funds from operations) ratio of 23.2x, roughly two points below its longer-term average. Including its 3.1% dividend yield and 4-5% expected annual per-share AFFO growth, we get a total return outlook of roughly 12% per year.

FAST Graphs

Especially if housing inflation accelerates again, INVH should be in a great spot to improve its AFFO growth.

Sun Communities, Inc. (SUI) – MH Communities Are the Place to Be

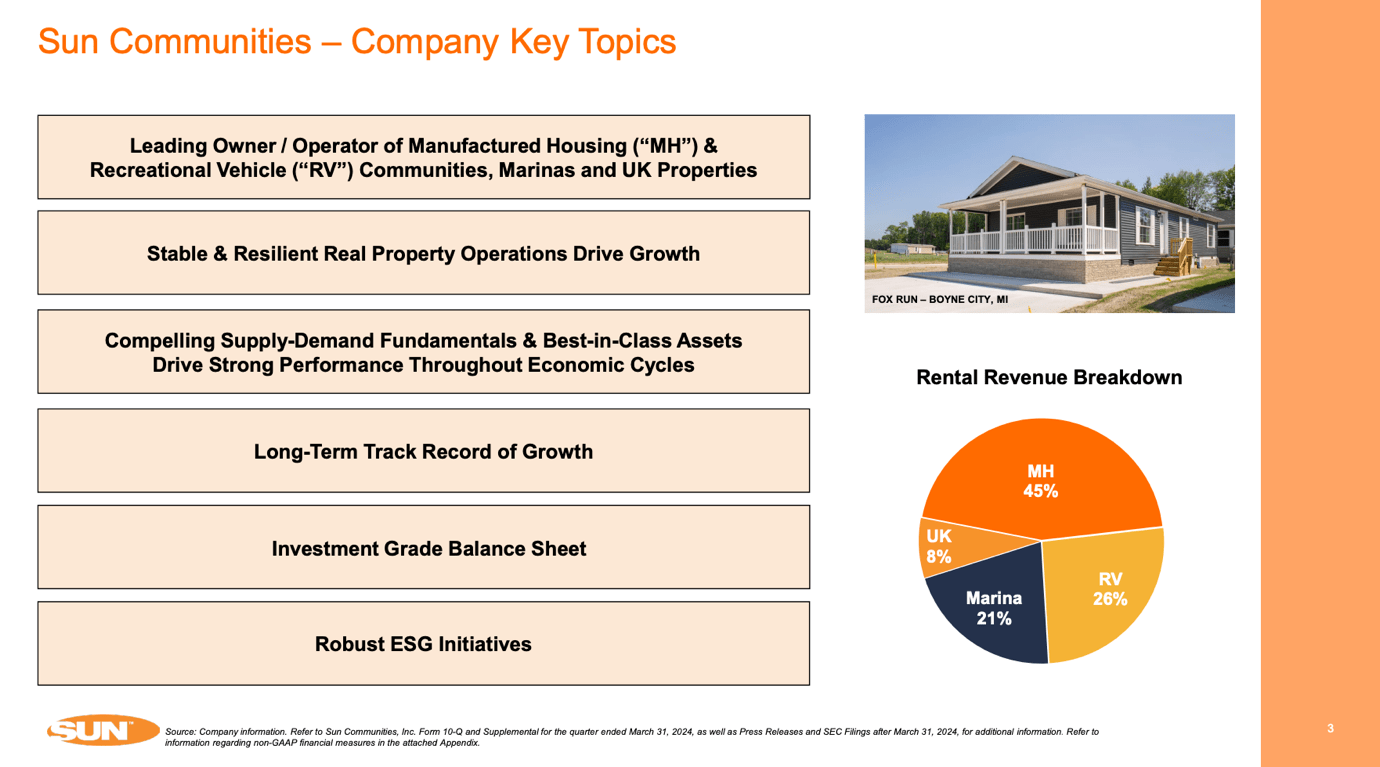

INVH has done a great job growing in the single-family segment. Sun Communities is different. Sun Communities owns and operates manufactured housing (“MH”) communities.

Moreover, it owns RV communities, marinas in attractive locations, and holiday parks in the United Kingdom.

Sun Communities

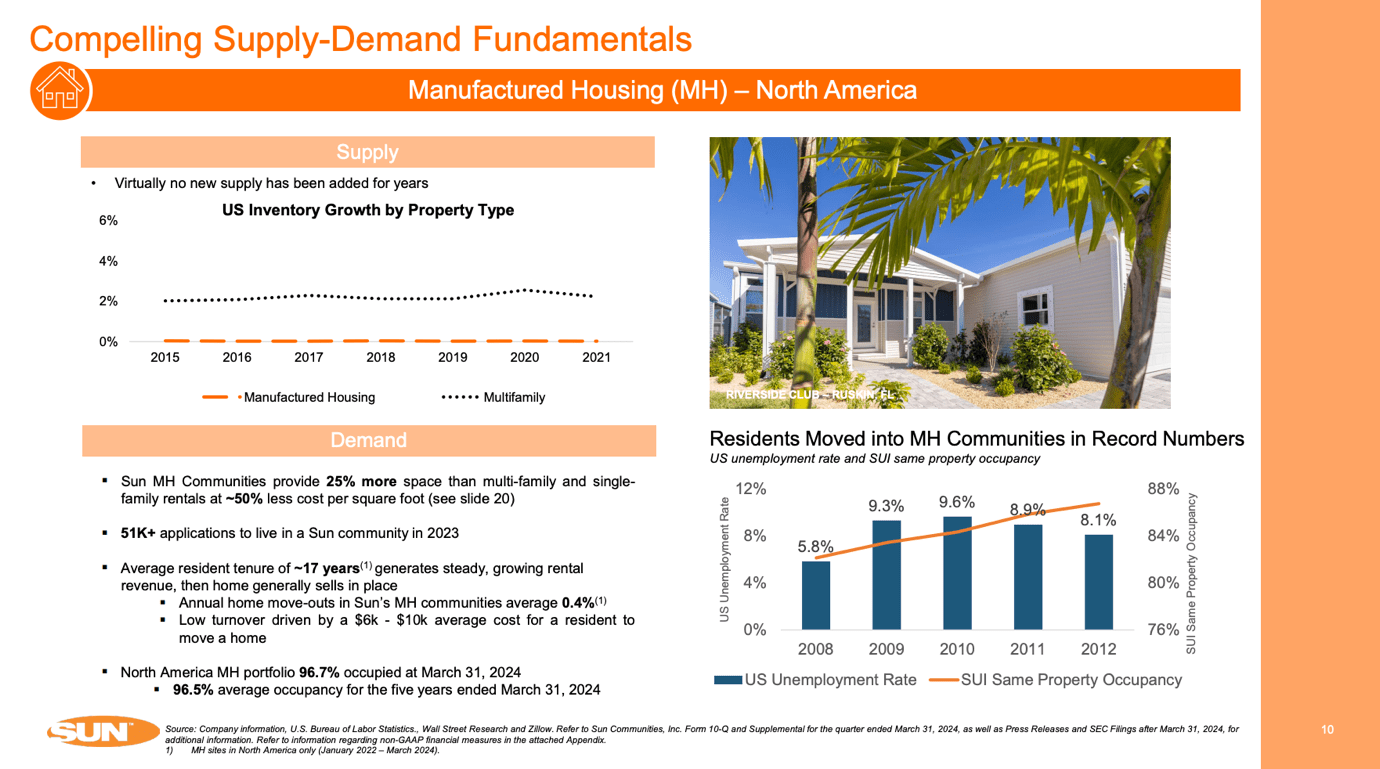

The company’s MH communities are 97% occupied and cover approximately 100 thousand sites, making Sun Communities the largest MH operator in North America.

Especially in light of affordability issues, MH communities are increasingly attractive. As we can see below, the typical MH assets provide 25% more space at a 50% lower cost. Last year alone, the company got over 50 thousand applications from people looking to live in its communities.

Not only are MH communities affordable, but they also come with the benefits of attractive amenities and efficient management, as SUI only needs to make sure the communities are clean. This can be done in a very effective and efficient manner.

Related to that, SUI also benefits from the fact that most of its tenants own their own MH assets, which reduces move-out rates and creates stable cash flow.

Sun Communities

It also benefits from secular growth in the RV space, a market that has seen 8% annual growth between 2014 and 2022.

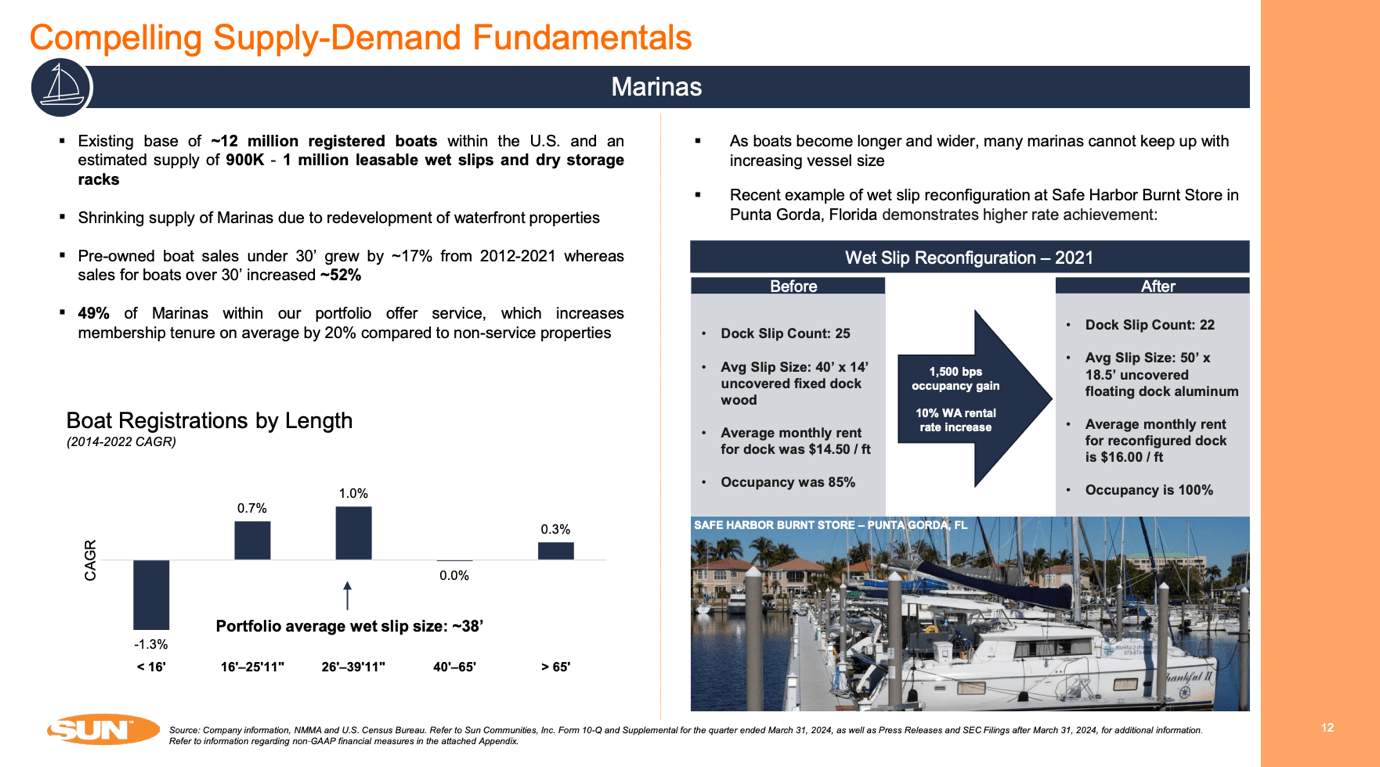

Meanwhile, in its marinas segment, the biggest growth driver is declining supply, as water-front housing reduces the number of marinas in attractive areas.

Sun Communities

Moreover, SUI enjoys an investment-grade balance sheet with no significant maturities until 2026, a net leverage ratio of 6.1x, and close to 80% unencumbered assets.

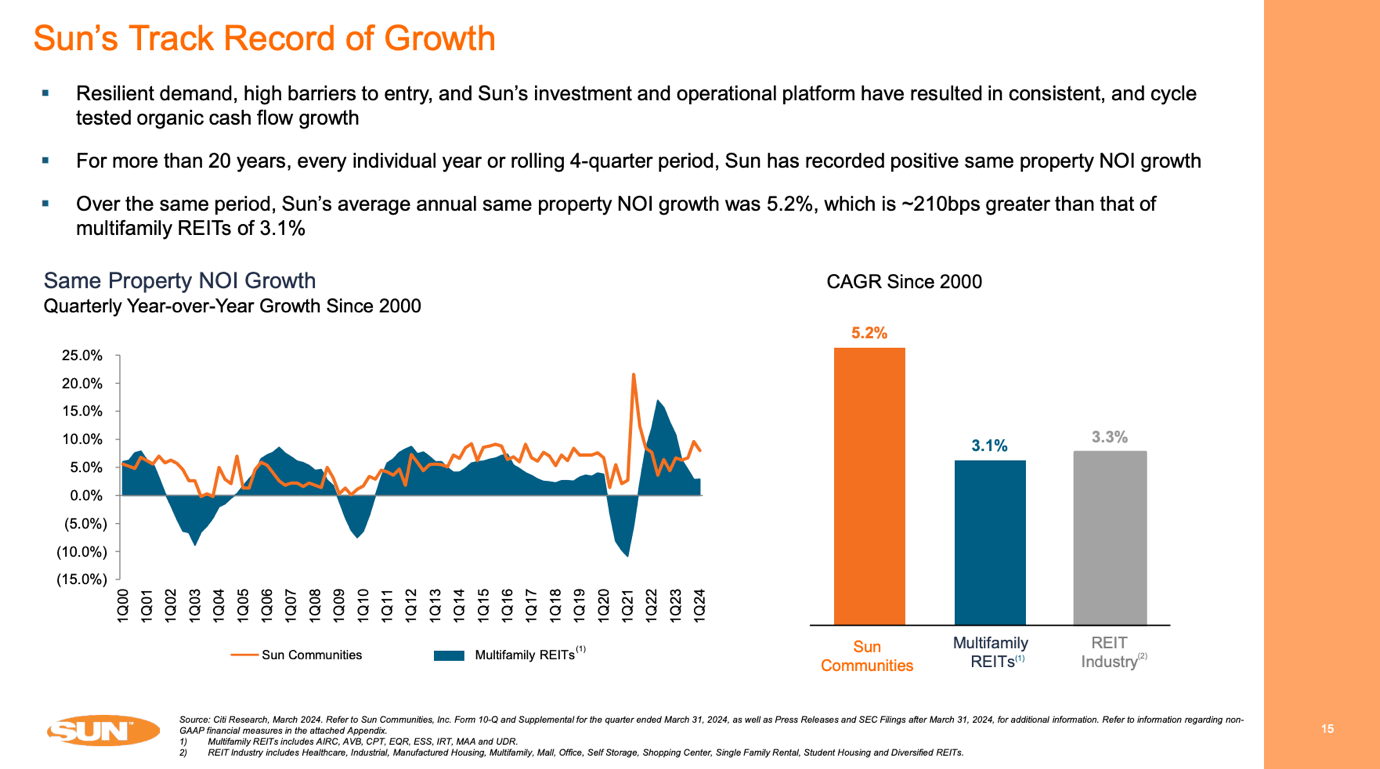

All of this has provided the company with consistent growth. As we can see below, even in the early 2000s, during the Great Financial Crisis, and the pandemic, the company generated positive net operating income (“NOI”) growth. Since 2000, NOI has grown by 5.2% per year, significantly higher than the REIT sector average.

Sun Communities

Regarding its dividend, we’re dealing with a 2.8% yield, protected by a very healthy payout ratio of 53% and a five-year CAGR of 5.1%.

Although SUI isn’t a company with elevated dividend growth, it has beaten the market by focusing on owning attractive assets with strong secular growth. Especially in the current market, this makes SUI a great pick.

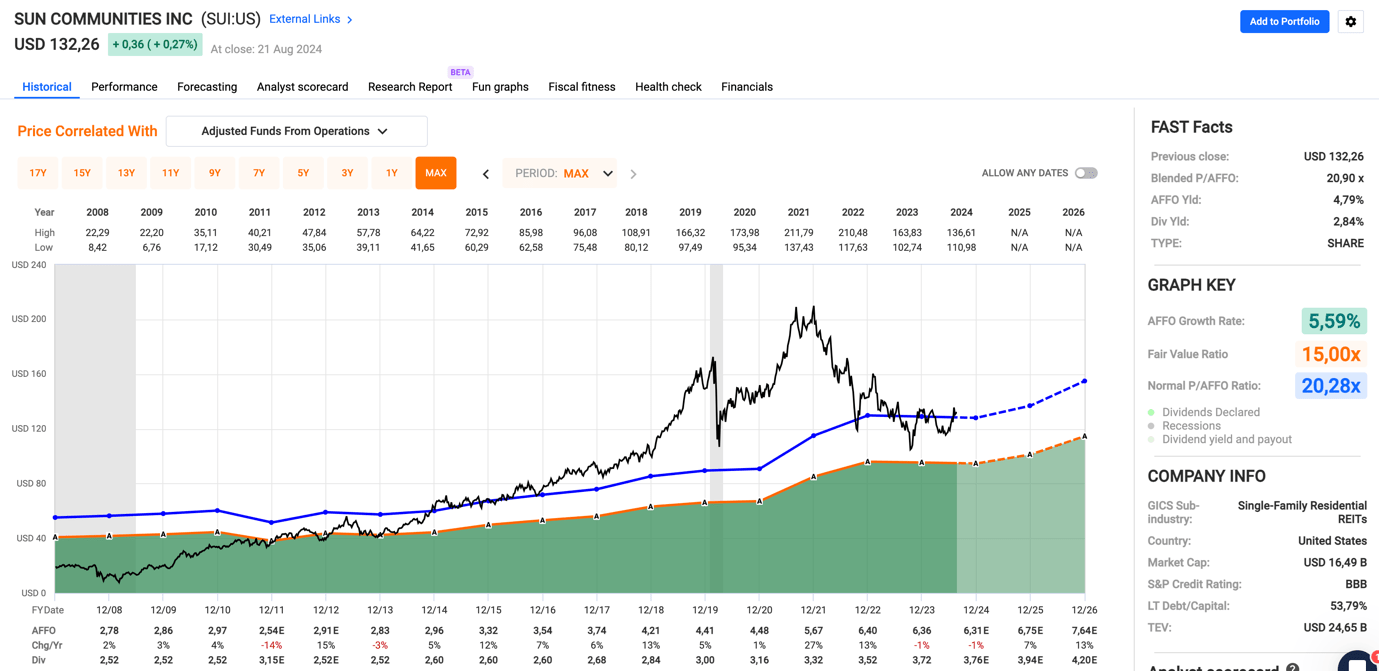

Valuation-wise, the company is trading at a blended P/AFFO ratio of 20.9x, slightly above its long-term average of 20.3x. Looking ahead, analysts see a path to 13% per-share AFFO growth in 2026, indicating a path to 10-11% annual returns.

FAST Graphs

Especially if the “affordability crisis” lasts, Sun Communities will become relatively more attractive, making it a top REIT play for the years ahead – regardless of who wins the election.

In Closing

In today’s housing market, affordability has become a major concern, with soaring home prices and higher mortgage rates putting tremendous pressure on potential buyers.

Although it needs to be seen how the government will intervene, it’s clear that something will happen. It’s also apparent that this could be a measure that increases housing inflation as a side effect (making things worse).

Meanwhile, the best opportunities lie with companies like Invitation Homes and Sun Communities, which are well-positioned to benefit from these affordability challenges.

All things considered, these REITs offer solid growth opportunities and attractive dividends, making them compelling options for investors seeking both capital appreciation and income.

{kind=link}