Just_Super

Rubrik (NYSE:RBRK), one of the notable tech IPOs this year, saw its stock sink slightly after reporting earnings after the bell on Monday. The company comfortably beat on quarterly guidance and raised its outlook for the full-year. I suspect that the stock price weakness has more to do with the IPO lock-up expiring on Tuesday, which may put pressure on the stock price as insiders sell their shares. RBRK is not a perfect story, as it remains unprofitable even on a non-GAAP basis. That said, the cash position looks sufficient to fund many years of losses, if needed, and the stock valuation looks as attractive as ever. I am reiterating my buy rating for the stock.

RBRK Stock Price

I last covered RBRK in April, where I gave the recent IPO a “buy rating” on account of the potential catch-up trade to cybersecurity peers. The stock has not performed well since then, underperforming the broader market by well over 20%. Ironically, close competitor Commvault (CVLT) appears to be the biggest winner from the IPO, as the stock is now up over 100% over the past year.

The stock’s weakness might be due to the expiry of its IPO lockup period – as specified in the company’s S-1 filing, the lock-up agreement expires on the first trading day following the release of the second quarter earnings report, which is Tuesday.

S-1 Filing

Investors might do well to look for attractive entry points amidst this volatile transition.

RBRK Stock Key Metrics

RBRK is a cybersecurity company focused on data recovery. The company offers products to help back-up customer data, which is an invaluable service in the event of a cyberattack.

FY25 Q2 Presentation

RBRK competes in a crowded space but appears to be a market leader as validated by both Gartner as well as its fast growth rates.

Rubrik

In the latest quarter, RBRK saw revenues grow 35% YoY to $205 million, surpassing guidance of $195 million to $197 million. The company prefers investors to focus on subscription annual recurring revenue (‘ARR’), which grew 40% YoY to $919 million.

FY25 Q2 Presentation

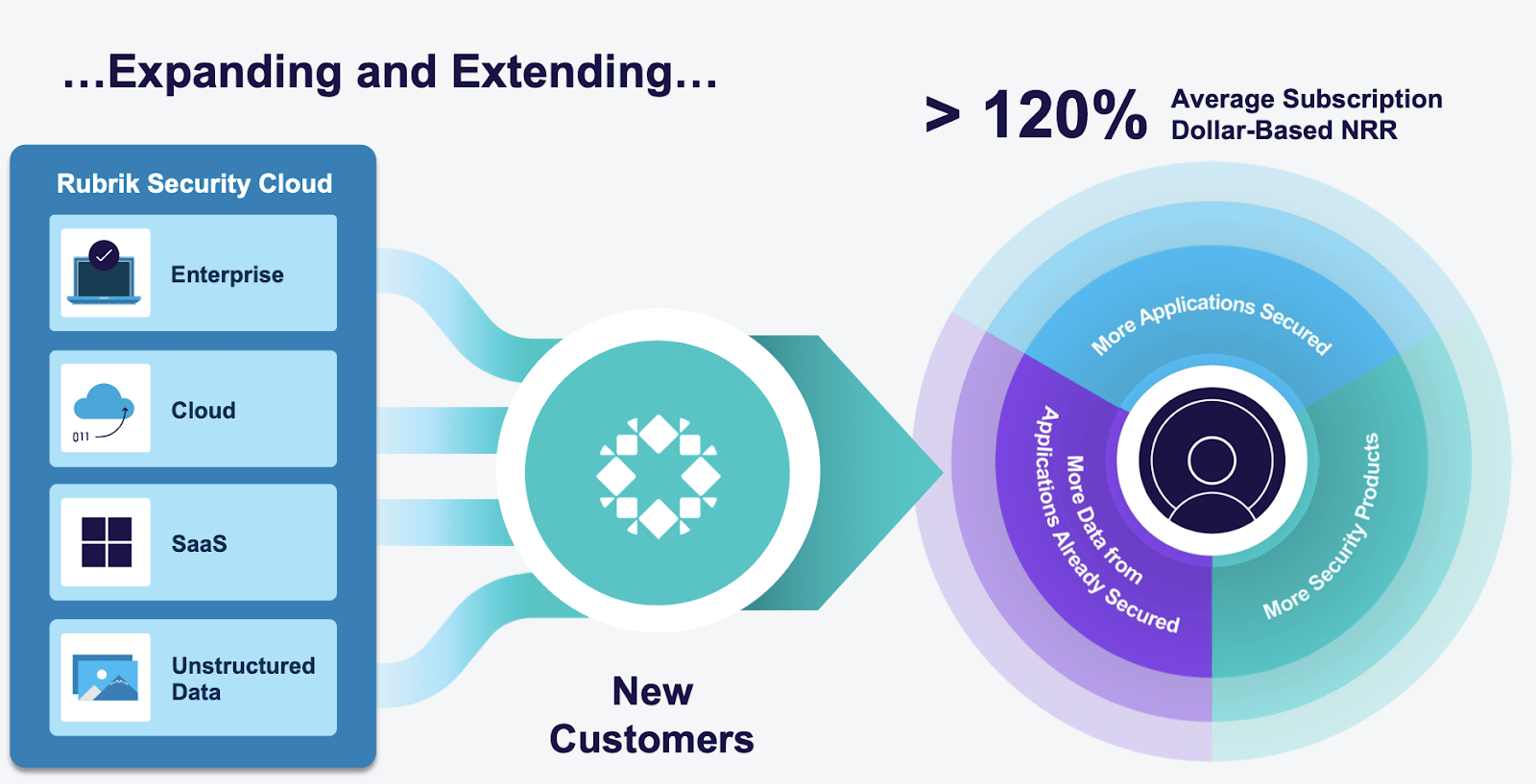

Management notes that the company’s ongoing transition from a perpetual to subscription pricing model drove 2.5 points of that growth. As noted in the first quarter conference call, management expects this benefit to moderate over the coming quarters. The company saw growth come primarily from new customer growth and growth from existing customers. The large customer count grew 35% YoY and the company reported a 120% average subscription dollar-based net retention rate. I note that this rate was in-line with the first quarter and continues to represent some deceleration from the 133% rate disclosed at the time of the IPO.

FY25 Q2 Presentation

Unlike many cybersecurity names, RBRK remains far from profitable, as the company was unprofitable even on a non-GAAP basis. The company did see its non-GAAP operating margin loss improve substantially to 30%, but this still represents one of the lower profitability profiles in the cybersecurity sector and tech market overall.

FY25 Q2 Presentation

RBRK ended the quarter with $601.3 million in cash versus $306.8 million in debt, representing a solid net cash position, albeit modest relative to many tech peers. While the company remains far from GAAP profitability, its free cash flow burn is quite modest, with management projecting up to $67 million in negative FCF this year. That cash balance looks adequate to support the financial needs of this business, especially given the highly recurring nature of the software industry.

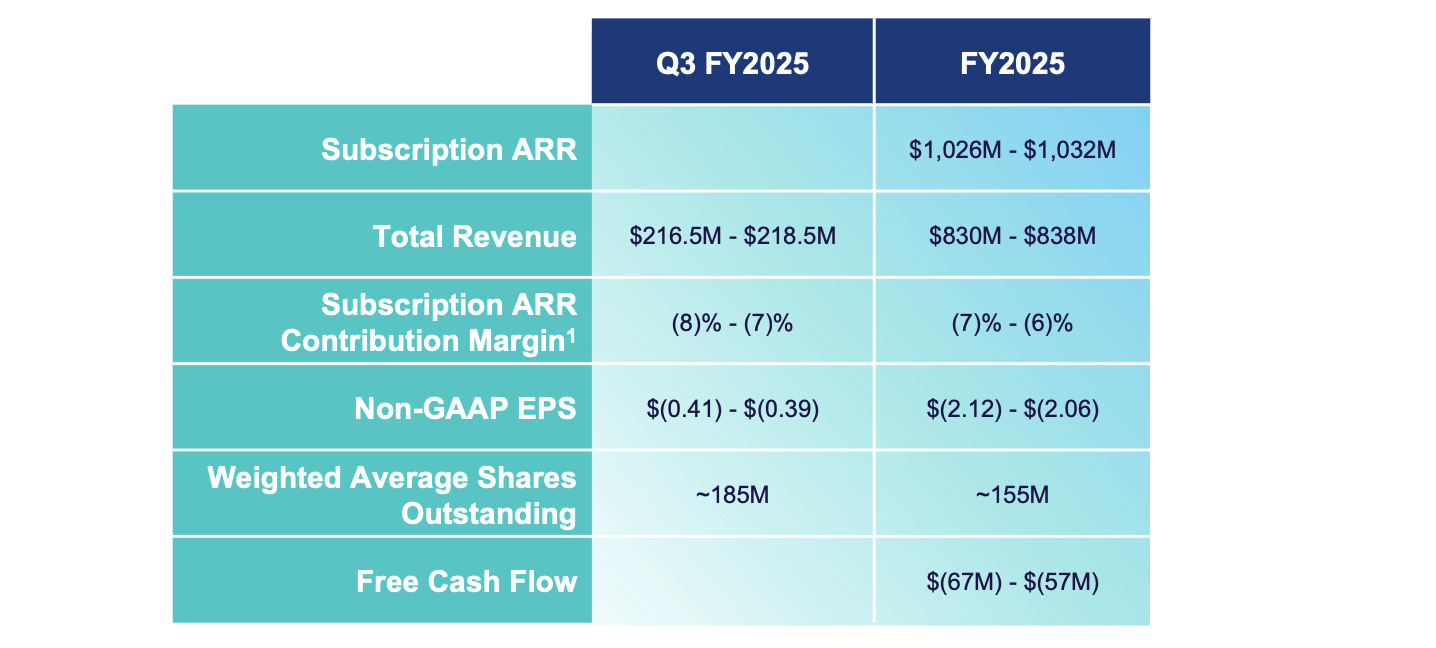

Looking ahead, management expects the third quarter to see up to $218.5 million in revenue, representing up to 31.9% YoY growth. Management raised the full-year targets to see up to $1.032 billion in subscription ARR (up from the prior target of $997 million) and $838 million in total revenue (up from the prior target of $824 million).

FY25 Q2 Presentation

The stock price might not suggest it, but these are arguably strong results from the newly public company, given that the software sector as a whole has seen very few of these “beat and raise” kind of results as of late.

Is RBRK Stock A Buy, Sell, or Hold?

The stock price weakness is quite interesting. As just noted, these results can hardly be blamed given the weakness seen overall from software names this quarter. I also noted previously that close peer CVLT has seen its stock trade sharply higher over the past year. That stock now trades at around 6.6x sales versus a slower 10% projected revenue growth rate, but perhaps the company’s GAAP profitability has helped power the re-rating. Even so, this is a different scenario than when RBRK first came public, when I had previously noted that CVLT’s then-discount at 4.2x sales represented a potential risk. At this point, one could make an argument that RBRK even looks cheap on a relative basis to CVLT, given that it trades at a similar P/S multiple versus a much faster 28% projected forward growth rate.

Seeking Alpha

I am adjusting my valuation framework in light of the weakness seen across many software names. I previously pegged 9x sales as a fair value estimate, leading to a target of $44 per share. I continue to expect 25% net margins over the long term. I now use 7.5x sales as a more appropriate valuation target. This would equate to a 30x long-term earnings multiple, which looks reasonable in light of the 20% to 28% projected forward top-line growth over the coming years. That low price to earnings growth ratio (‘PEG ratio’) is justified due to the GAAP operating losses, which drag against annual returns. This leads to a stock price target of $35 per share over the next 12 months.

RBRK Stock Risks

There are two main risks to consider here. First, as discussed previously, the company remains far from GAAP profitable. This adds to both the financial risk as well as detracting from the annual return potential. Moreover, while the valuation looks cheap relative to cybersecurity peers like CrowdStrike (CRWD), it does not look cheap relative to other software names. It is possible, if not likely, that the stock experiences greater volatility in the event of a market downturn, as investors have historically been quick to flee unprofitable names during such times. There is also the risk of competition and the potential impact on the growth rate. RBRK has posted solid growth results since coming public, but the growth rates have decelerated rapidly (the company saw subscription ARR growth of 47% in 2023). It is possible that top-line growth decelerates far faster than expected – again, the lack of profitability may lead to greater stock volatility under such a scenario.

RBRK Stock Conclusion

RBRK has not enjoyed the same market love experienced by many cybersecurity names, and this is in spite of the company posting a rare beat-and-raise quarter. The stock appears poised for some near term weakness due to the expiration of the IPO lock-up period and the poor profitability metrics, but I still see strong growth ahead relative to the modest valuation. Investors may need to wait for further improvements in cost discipline before enjoying a re-rating, but the company’s strong balance sheet may help weather the storm while we wait. I reiterate my buy rating for the stock.

{kind=link}