Klaus Vedfelt

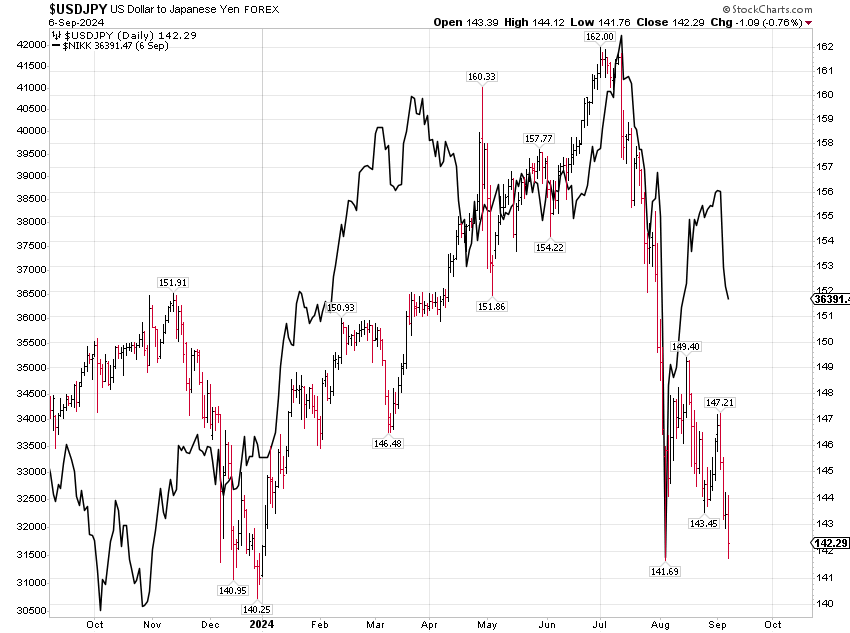

Those pundits that pronounced on TV that the yen carry trade was 50% to 75% unwound last month better be right, as the Japanese currency is just one session away from taking out the high for last month, a high which caused the Nikkei 225 Index (dark line below) to more or less crash.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

When I heard those prognostications, I expressed skepticism (right here in this column), since unless those pundits are high up in the Bank of Japan or involved intimately with the Japanese interbank lending market, they had no good way of knowing the state of the yen carry trade.

The high for the yen this year is a few ticks above 141, while the high for the past 12 months is 140.25, registered in late December (when the yen goes down, that means the yen is appreciating, as it takes fewer yen to buy a dollar). Clearly, we can make a new high without the BOJ hiking rates, as it originally intended, and I sure hope they skip on the rate hike as it would be like throwing kerosene on a fire.

The U.S. market has started a retest of the August low quite expeditiously, as the stock market went down every day last week. There is reason for optimism this week as we have a CPI report on Wednesday which, if very good, would solidify the case for a 50 basis-point rate cut. I still think that by cutting interest rates 50 bps, the Fed is admitting that they are too late to cut, but I suppose that would be better late than never.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

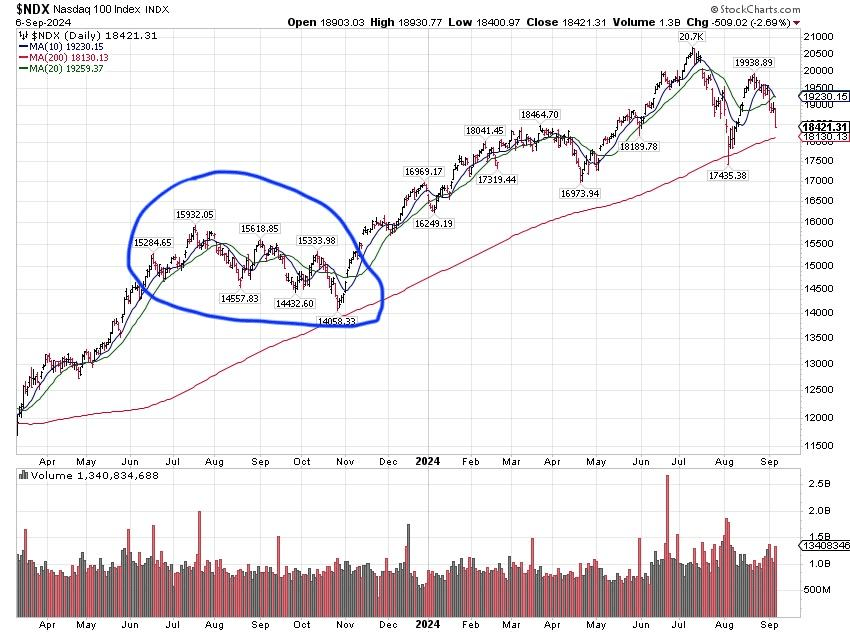

The technology sector led the August rebound to the upside and is now leading the selloff to the downside, as is typically the case. We again have a convergence with the NASDAQ 100’s 200-day moving average, which was a one-day wonder in August. This time it is unknowable if it is a one-day wonder, or if it will be flipping around, as is often the case.

A successful retest of the August low does not mean the market can’t trade below that low point. It means that there should not be an appreciable downside below that level and certainly not below 17,000 on the NASDAQ 100, which is right around the April low. The market appears to be doing exactly what it did last year in the August-October period (annotated above).

There is again a rotation out of the technology sector, as the S&P 500 Equal Weight Index and Dow Industrials made fresh all-time highs on the rebound in August, while the NASDAQ 100 and the S&P 500 didn’t.

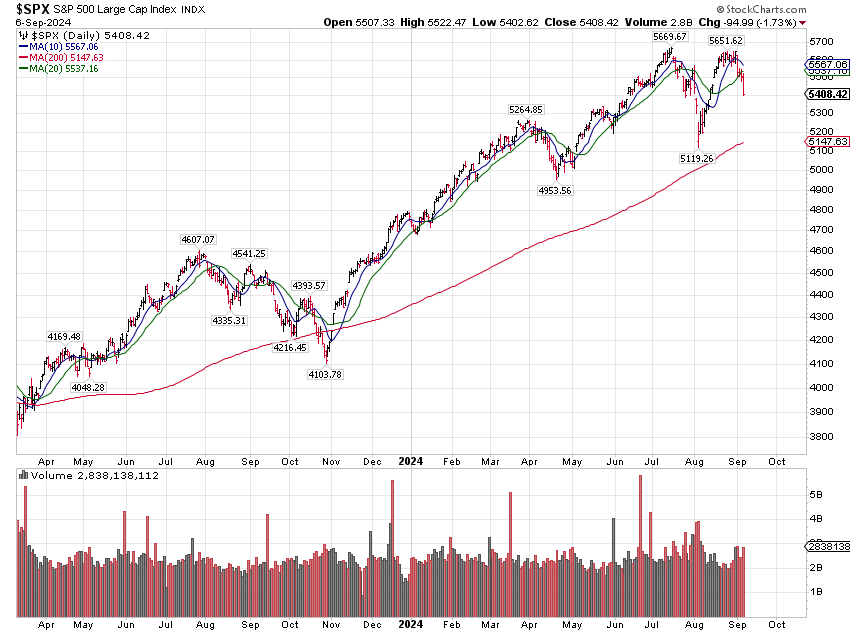

I would not be surprised if we kiss the 200-day moving average on the S&P 500 before Election Day, which is 250 S&P points below where we closed last week and rising.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

A rising 200-day moving average tends to provide good support for corrections. Last year we undercut it mildly and still rallied. Undercutting a rising 200-day moving average is generally not a big deal. It is a much bigger deal if the index declines below a declining 200-day moving average, which takes a while to turn lower. As things stand now, we are in the middle of a correction/consolidation that began in late July.

If we get more aggressive rate cutting by the Fed for the rest of this year, it would be likely that the broad market and the small-cap Russell 2000 Index outperform the tech sector, which they had been lagging, until July. Those are the types of companies with higher debt loads that will see the biggest benefit from Fed rate cuts. The cash-rich technology giants are great businesses but don’t benefit as much from falling rates.

Many have asked me if the sharp selloff in stocks indicates a coming recession. I do not believe that there is a big difference between a soft landing and a mild recession. As things stand right now, the stock market is up a lot for the year and is now flipping, in classic pre-election style.

There is a famous quote, which, according to ChatGPT, is attributed to Paul Samuelson: “The stock market has forecasted nine out of the last five recessions.” ChatGPT says he made this witty remark in 1966 in Newsweek to highlight the stock market’s tendency to predict recessions more often than they actually occur, emphasizing its unreliability as a sole indicator of economic downturns.

When it comes to recessions, my experience is that the bond market is a bit better in forecasting them, and I am not referring to yield curve inversions, which have so far failed to predict anything on the latest inversion.

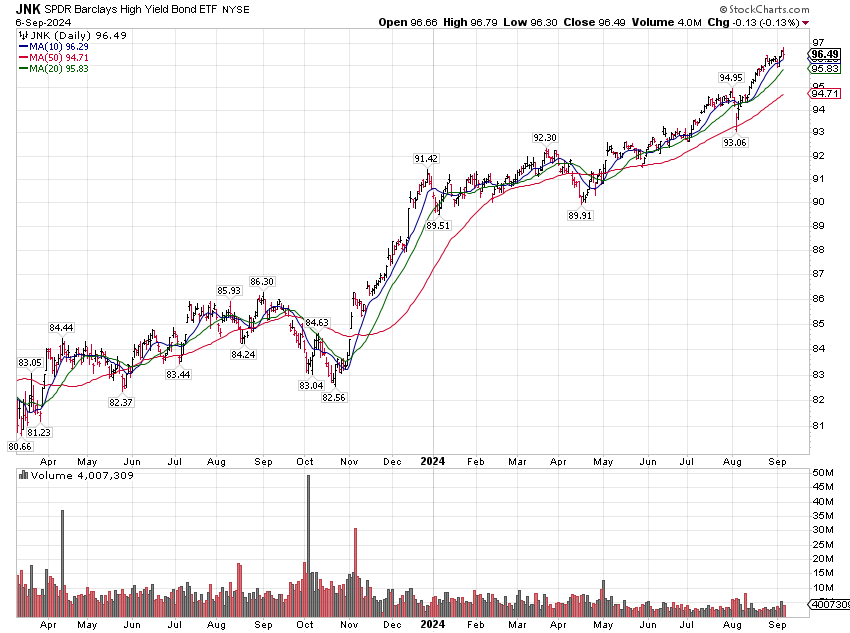

I mean junk bond prices and credit spreads. Single B-rated bonds have credit spreads that are well below 400 basis points when it comes to treasuries, 312 at last count. At the low last October, when the most recent stock market rally started, this same spread was at 470 bps.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Junk bond prices and their famous correlation to stock prices do not show a recession coming soon. The above is a total return chart that includes the substantial yield coming from junk bonds. The sell-off in junk bonds so far is not evident. The sell-off in junk bonds in August of this year was quite a bit smaller than the sell-off they had in April. So far, the junk bond market does not see any recession on the horizon.

All content above represents the opinion of Ivan Martchev of Navellier & Associates, Inc.

Disclaimer: Please click here for important disclosures located in the “About” section of the Navellier & Associates profile that accompany this article.

Disclosure: *Navellier may hold securities in one or more investment strategies offered to its clients.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

{kind=link}